Home Loan Securitization Fraud: How the Secondary Mortgage Market Really Works

The modern mortgage industry is built on a complex financial ecosystem that extends far beyond the local bank where a borrower signs loan documents. At the center of this system lies the secondary mortgage market—a powerful network where mortgage loans are bought, bundled, and sold as investment products to institutional investors around the world. While this system helps provide liquidity to lenders and keeps credit flowing to homebuyers, it has also become a focal point for concerns about transparency, documentation integrity, and potential home loan securitization fraud.

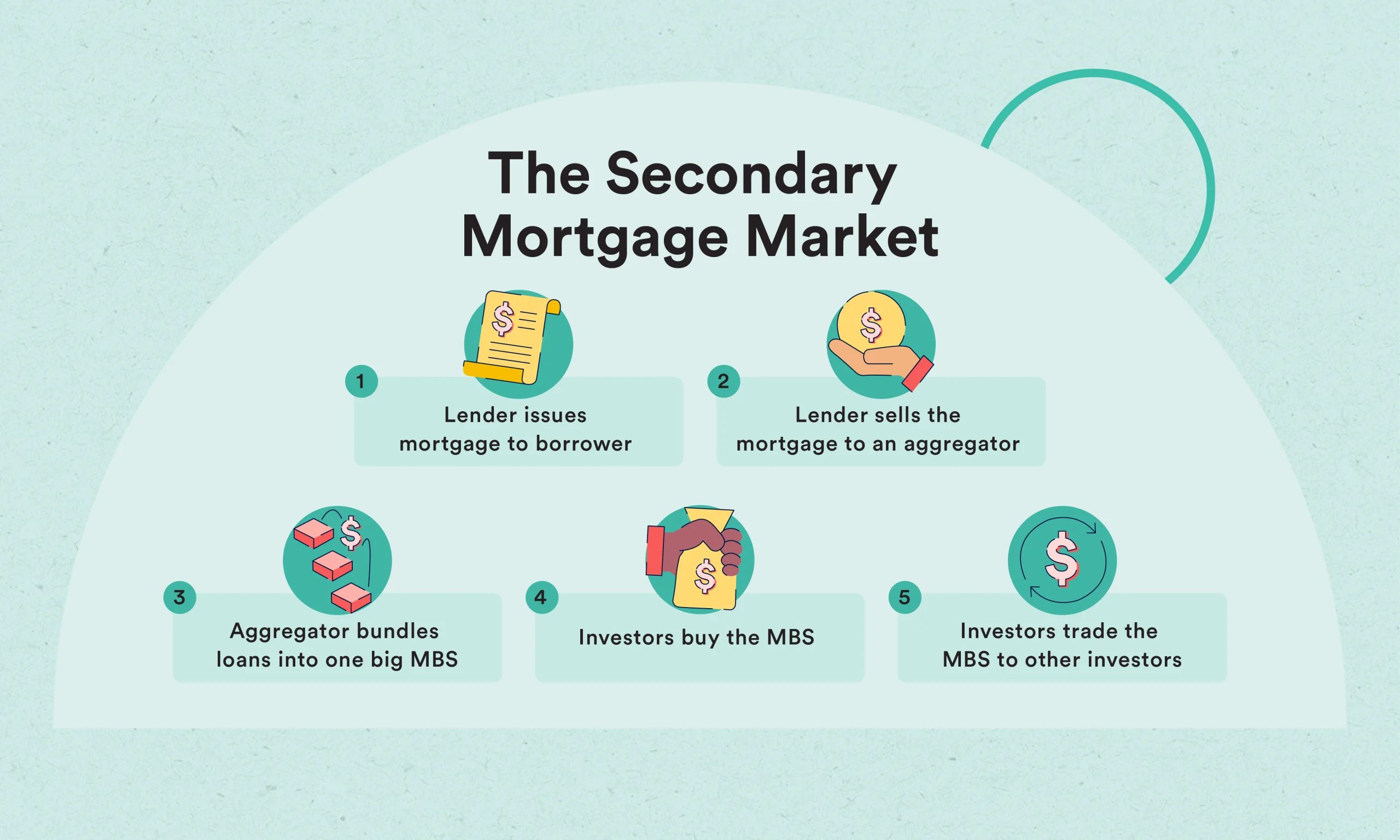

For most homeowners, the mortgage process seems straightforward: a lender provides funds to purchase a home, and the borrower repays the loan over time. However, behind the scenes, that original lender often does not keep the loan. Instead, the loan may be quickly sold to another financial institution, pooled with thousands of other mortgages, and converted into mortgage-backed securities (MBS). These securities are then sold to investors such as pension funds, hedge funds, and insurance companies. This process, known as securitization, has become a cornerstone of the global financial system.

While securitization itself is not illegal, the rapid transfer of loans through multiple entities has created opportunities for irregularities. Questions have emerged regarding missing paperwork, incomplete loan transfers, improper endorsements, and inaccurate representations in securitized mortgage pools. These issues are frequently associated with allegations of home loan securitization fraud, where the documentation or ownership trail of a mortgage may not fully comply with legal or contractual requirements.

Understanding home loan securitization fraud requires a closer look at how mortgages move through the financial system after origination. Typically, a lender originates a mortgage and sells it to a larger aggregator or investment bank. The aggregator then pools similar loans together and transfers them into a trust that issues mortgage-backed securities to investors. Each step in this chain requires precise documentation and strict compliance with trust agreements, pooling and servicing agreements (PSAs), and securities regulations.

Problems can arise when the required transfer procedures are not followed correctly. For example, loans must often be transferred into a trust by a specific deadline and accompanied by properly endorsed promissory notes and assignments of mortgage. If those steps are skipped, delayed, or improperly documented, it can raise legal questions about who actually owns the loan and whether the trust has the authority to enforce it. Such irregularities are frequently cited in investigations related to home loan securitization fraud.

Another layer of complexity comes from the electronic tracking systems used in the mortgage industry. Over the past two decades, digital registries have been used to record mortgage transfers in order to speed up the securitization process. While these systems were designed to simplify record-keeping, critics argue that they sometimes bypass traditional county recording procedures, potentially leading to gaps in the public record. In certain disputes, these documentation gaps have become central to claims of home loan securitization fraud.

The consequences of these issues became widely visible during the global financial crisis. As millions of homeowners faced foreclosure, courts and investigators began scrutinizing mortgage documentation more closely. In many cases, questions arose about whether the party initiating foreclosure could demonstrate a clear chain of ownership for the loan. These cases sparked widespread debate among legal professionals, consumer advocates, and financial experts about the role securitization practices may play in cases involving home loan securitization fraud.

Today, the secondary mortgage market remains essential to the housing economy. It enables lenders to free up capital, extend more loans, and maintain a steady supply of mortgage financing for homebuyers. At the same time, the complexity of securitization structures means that transparency and compliance remain critical. Proper documentation, accurate loan transfers, and adherence to trust agreements are necessary safeguards that help ensure the system functions as intended.

For borrowers, attorneys, and financial professionals, understanding the mechanics of securitization is increasingly important. Allegations of home loan securitization fraud often arise from misunderstandings about how mortgage loans are transferred and managed after origination. By examining the structure of the secondary mortgage market and the legal framework governing mortgage-backed securities, it becomes easier to identify where errors, irregularities, or potential violations may occur.

Ultimately, exploring the realities behind home loan securitization fraud requires a balanced understanding of both the benefits and the risks associated with mortgage securitization. While the system has enabled unprecedented access to home financing, its complexity also demands rigorous oversight and careful legal scrutiny to ensure that borrowers, investors, and financial institutions operate within the boundaries of the law.

Understanding the Foundation of Mortgage Securitization

To fully understand home loan securitization fraud, it is important to first understand how mortgage securitization developed and why it became such a dominant force in the housing finance system. Mortgage securitization emerged as a financial innovation designed to increase liquidity in the housing market. Instead of banks holding mortgage loans for 20 or 30 years, they could sell those loans to investors through structured financial instruments known as mortgage-backed securities.

In this process, a mortgage lender originates a home loan and then sells that loan to a financial institution or aggregator. That institution bundles thousands of similar mortgages into a pool and transfers them into a trust. The trust then issues securities backed by the monthly payments from homeowners. Investors purchase these securities because they generate predictable income streams.

This process helped expand homeownership by allowing lenders to issue more mortgages without keeping them on their balance sheets. However, the complexity of these transactions also created opportunities for errors, misrepresentations, and potential home loan securitization fraud. When loans move rapidly through multiple institutions, maintaining accurate documentation becomes both critical and challenging.

As securitization expanded globally, the industry relied heavily on precise legal frameworks that govern how loans must be transferred into trusts. If those procedures are not followed correctly, it can raise serious questions about the validity of the securitization process and whether the trust truly owns the loans it claims to hold.

The Role of the Secondary Mortgage Market

The secondary mortgage market plays a central role in the securitization system and is often where discussions of home loan securitization fraud originate. The secondary market allows lenders to sell mortgage loans after they are originated, which frees up capital and allows them to issue new loans to other borrowers.

In the United States and many other countries, large financial institutions and government-sponsored entities dominate the secondary mortgage market. These entities purchase mortgages from lenders and package them into investment securities that are sold to institutional investors worldwide.

While this system promotes liquidity and supports housing markets, it also introduces a chain of transactions that can become difficult to trace. Mortgages may be sold several times between different entities before they are finally placed into a securitized trust. Each transfer must comply with strict legal requirements, including proper endorsements and assignments of the mortgage note.

When these steps are overlooked, delayed, or improperly documented, it can lead to disputes about ownership of the loan. These disputes are frequently associated with allegations of home loan securitization fraud, particularly when foreclosure actions rely on documents that appear incomplete or inconsistent with the securitization timeline.

Documentation and Chain of Title Concerns

One of the most common issues discussed in relation to home loan securitization fraud involves the concept of the mortgage “chain of title.” The chain of title refers to the documented history showing how a loan was transferred from the original lender to subsequent holders.

For securitization to be legally valid, each transfer must occur in a specific sequence and must be properly recorded. This typically involves endorsing the promissory note and assigning the mortgage to the next entity in the securitization chain. These transfers must also occur within the timeframe established by the trust’s governing documents.

However, during the housing boom of the early 2000s, the mortgage industry processed enormous volumes of loans at unprecedented speeds. In some cases, documentation procedures were rushed or overlooked entirely. As a result, questions began to emerge about whether certain loans were transferred correctly.

These concerns became particularly significant when foreclosure proceedings began following the financial crisis. Borrowers and attorneys started requesting proof that the entity initiating foreclosure actually owned the loan. In many cases, courts required lenders to produce documentation demonstrating the full chain of title. When such documentation appeared incomplete or inconsistent, allegations of home loan securitization fraud often followed.

Electronic Registration Systems and Record-Keeping Challenges

Another factor that contributed to discussions of home loan securitization fraud was the adoption of electronic mortgage registration systems. These systems were designed to streamline the transfer of mortgage loans between institutions without requiring repeated filings in local county recording offices.

The goal was to make the securitization process faster and more efficient. Instead of recording each transfer publicly, the electronic system tracked changes in loan ownership within a centralized digital database. While this system improved efficiency, it also introduced new challenges.

Critics argue that bypassing traditional recording procedures may create gaps in the public record, making it more difficult to verify who actually owns a mortgage at any given time. When disputes arise, these gaps can complicate legal proceedings and raise questions about whether the loan transfers complied with legal requirements.

These issues have played a role in numerous legal cases involving alleged home loan securitization fraud, particularly when conflicting records exist between electronic databases and traditional land records.

Legal Scrutiny After the Financial Crisis

The global financial crisis brought unprecedented attention to the mortgage securitization industry. As foreclosure rates surged, courts began examining the documentation behind mortgage loans more closely than ever before. This scrutiny revealed instances where lenders struggled to produce complete records of loan ownership.

Some cases involved documents that appeared to have been created after foreclosure proceedings had already begun. Others involved missing endorsements or assignments that were required under the securitization trust agreements. These irregularities fueled public debate about whether widespread home loan securitization fraud had occurred within the mortgage industry.

Government investigations and legal settlements followed, prompting financial institutions to strengthen compliance procedures and improve documentation practices. Regulatory reforms also aimed to increase transparency in the securitization process and reduce systemic risks within the financial system.

Although many improvements have been made since the crisis, legal professionals and financial analysts continue to examine securitization structures carefully. The complexity of these transactions means that even small documentation errors can have significant legal implications.

Why Understanding Securitization Matters for Borrowers and Professionals

For homeowners, attorneys, and financial professionals, understanding how mortgage securitization works can provide valuable insights into the broader housing finance system. While the concept may seem distant from the everyday experience of making mortgage payments, securitization ultimately determines who owns the loan and who has the authority to enforce it.

When questions arise about documentation or loan ownership, the issue may involve the securitization process itself. In such cases, forensic loan audits and detailed reviews of securitization records can help clarify whether the loan was transferred correctly.

The growing awareness of home loan securitization fraud has also led to increased interest in mortgage audits and investigative services that examine the legal and financial structure of mortgage-backed securities. These analyses can uncover discrepancies in loan transfers, trust compliance, and servicing practices.

As the mortgage industry continues to evolve, transparency and accountability remain essential. Understanding the mechanisms behind home loan securitization fraud allows borrowers and professionals to navigate complex financial systems with greater confidence and awareness.

By examining the structure of securitized mortgages, the role of documentation, and the legal standards governing loan transfers, it becomes possible to better understand how the secondary mortgage market truly operates—and why maintaining accurate records is essential to protecting both borrowers and investors.

Conclusion

Understanding the structure of the modern mortgage system is essential for anyone involved in housing finance, legal advocacy, or mortgage servicing. The secondary mortgage market has transformed the way home loans are funded, enabling lenders to provide financing to millions of borrowers while distributing financial risk among global investors. However, the complexity of this system has also created areas where documentation errors, compliance failures, and irregular loan transfers can occur—issues that are often associated with home loan securitization fraud.

Throughout the securitization process, every mortgage must follow a clearly defined chain of transfers from the originating lender to the securitized trust that ultimately holds the loan. When those transfers are incomplete, improperly recorded, or executed outside the required timelines, legal questions can arise regarding the true ownership of the loan. These situations frequently lead to investigations or claims related to home loan securitization fraud, particularly during foreclosure disputes where proof of loan ownership becomes critical.

For borrowers, attorneys, and financial professionals, gaining a deeper understanding of home loan securitization fraud helps reveal how the mortgage industry functions behind the scenes. Transparency, proper documentation, and strict compliance with securitization agreements remain essential safeguards that protect both homeowners and investors while preserving trust in the global housing finance system.

Unlock Clarity. Strengthen Your Case. Transform Your Client Outcomes

When mortgage litigation, foreclosure defense, or securitization analysis becomes complex, having the right insights can make all the difference. That’s where Mortgage Audits Online steps in as a trusted professional partner. For more than four years, the firm has been helping industry associates build stronger, evidence-based cases through detailed securitization and forensic mortgage audits designed specifically for professional use.

Unlike consumer-focused services, Mortgage Audits Online operates exclusively as a business-to-business provider, working with attorneys, law firms, mortgage professionals, and industry specialists who require accurate, well-structured reports that can withstand professional scrutiny. Each audit is built on documented loan data, regulatory benchmarks, and thorough analysis, helping professionals identify inconsistencies, strengthen arguments, and approach complex mortgage cases with confidence.

Their audit process focuses on clarity and precision—reviewing loan documentation, securitization records, assignments, endorsements, and servicing data to uncover discrepancies that may impact legal strategy or compliance evaluation. By translating complicated mortgage data into clear, actionable insights, Mortgage Audits Online equips professionals with the information they need to make informed decisions and move cases forward effectively.

If your work involves foreclosure litigation, mortgage compliance reviews, or securitization analysis, partnering with a team that understands the intricacies of the secondary mortgage market can give you a meaningful advantage. Mortgage Audits Online provides the analytical depth and documentation needed to support stronger professional outcomes.

Connect with Mortgage Audits Online today and empower your cases with data-driven clarity and expert-level mortgage analysis.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}