Why Regulators and Analysts Are Investigating Home Loan Securitization Fraud

The modern housing finance system relies heavily on securitization—a process that allows lenders to bundle thousands of home loans together and sell them as investment products to institutional investors around the world. While securitization has played a major role in expanding access to mortgage credit and increasing liquidity in the financial markets, it has also raised serious concerns among regulators, legal experts, and financial analysts. Over the past decade, increasing scrutiny has emerged around home loan securitization fraud, a complex issue that sits at the intersection of banking practices, investor transparency, and consumer protection.

At its core, home loan securitization fraud refers to deceptive or improper practices associated with the packaging, documentation, transfer, and representation of mortgage loans within securitized financial instruments. In many cases, the fraud allegations revolve around whether loans were properly transferred into mortgage-backed securities trusts, whether investors were accurately informed about the quality of the underlying loans, and whether borrowers’ legal rights were compromised during the securitization process. These concerns are not just theoretical—they have triggered investigations, litigation, and policy reforms across several jurisdictions.

One of the primary reasons regulators and analysts are paying closer attention to home loan securitization fraud is the potential systemic risk it poses to financial stability. When mortgage loans are bundled into securities and sold globally, even minor irregularities in documentation or loan quality can multiply across thousands of assets. If those irregularities involve misrepresentation or intentional concealment, the impact can ripple through financial markets, undermining investor confidence and potentially destabilizing financial institutions. This risk became painfully evident during the global financial crisis of 2007–2008, when flawed mortgage-backed securities contributed to widespread market disruption.

Regulators are particularly concerned with transparency and compliance in the securitization chain. The securitization process involves multiple participants—originating lenders, servicers, trustees, investment banks, and investors. Each participant plays a specific role, and any breakdown in documentation or oversight can create opportunities for home loan securitization fraud. For example, investigators often examine whether mortgage notes and assignments were properly transferred to the securitization trust as required by trust agreements and securities regulations. If these transfers were incomplete, backdated, or improperly executed, the legal ownership of the loan may be called into question.

Financial analysts also investigate home loan securitization fraud because it directly affects the valuation and credibility of mortgage-backed securities. Investors rely on accurate disclosures regarding loan performance, borrower credit quality, and underwriting standards. When those disclosures are misleading or incomplete, the resulting securities may carry risks that investors were never fully informed about. Analysts therefore examine securitization structures, loan-level data, and servicing practices to determine whether the underlying assets match the representations made to investors.

Another major factor driving investigations into home loan securitization fraud is the growing number of legal disputes between borrowers, lenders, and investors. In many foreclosure cases, borrowers have challenged the legal standing of entities attempting to enforce mortgage loans. These challenges sometimes reveal gaps in the chain of title or inconsistencies in the transfer of mortgage documents during securitization. While not every irregularity constitutes fraud, such findings often prompt deeper reviews by regulators and forensic auditors.

Technology and forensic auditing have further strengthened the ability of regulators and analysts to detect patterns associated with home loan securitization fraud. Advanced data analytics now allow investigators to review thousands of mortgage records, trust filings, and servicing reports to identify inconsistencies. By comparing securitization trust documents with county property records and loan databases, analysts can uncover discrepancies that might otherwise remain hidden. This growing analytical capability has increased both awareness and enforcement activity in the securitization sector.

Importantly, the investigation of home loan securitization fraud is not solely about assigning blame; it is also about strengthening financial accountability and restoring trust in mortgage markets. Regulators seek to ensure that lending institutions adhere to proper documentation standards, disclose accurate information to investors, and respect the legal rights of borrowers. Analysts, meanwhile, play a critical role in evaluating the integrity of securitized assets and helping investors understand potential risks.

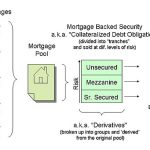

The Mechanics of Mortgage Securitization and Where Risks Begin

To understand why regulators and financial analysts are closely examining home loan securitization fraud, it is important to first understand how mortgage securitization works. In a typical mortgage transaction, a lender provides funds to a borrower to purchase a home, and the borrower agrees to repay the loan over time with interest. However, instead of holding the loan for decades, many lenders sell the mortgage to a secondary market. This is where securitization begins.

In the securitization process, thousands of individual home loans are pooled together and transferred into a trust or special purpose vehicle. That trust then issues securities—commonly known as mortgage-backed securities—to investors. These investors receive payments derived from homeowners’ monthly mortgage payments. The structure is designed to distribute risk and provide liquidity to lenders so they can continue issuing new loans.

While the concept itself is not inherently problematic, the complexity of the process creates opportunities for misrepresentation and documentation errors. The transfer of loans from the original lender to the securitization trust must follow strict legal and procedural requirements. If these steps are not properly followed, it can lead to disputes over ownership, documentation integrity, and investor disclosures. These breakdowns in procedure often form the foundation of allegations related to home loan securitization fraud, especially when financial institutions cannot clearly demonstrate that loans were legally transferred into the trust structure.

Documentation Irregularities and Chain of Title Concerns

One of the most widely investigated aspects of home loan securitization fraud involves documentation irregularities. Mortgage securitization relies on precise recordkeeping because every loan must be transferred through a clear chain of ownership before it becomes part of a securitized pool. This chain typically includes assignments of the mortgage, endorsements of the promissory note, and compliance with trust agreements that govern the securitization vehicle.

Regulators and analysts frequently review whether these transfers were executed according to the governing trust documents. In many investigations, inconsistencies have been discovered in the timing or authenticity of loan assignments. For example, some mortgage documents appear to have been signed or recorded long after the securitization trust had already closed. Such discrepancies raise concerns about whether the loan was ever legally placed into the trust in the first place.

These documentation issues are central to many claims involving home loan securitization fraud because they challenge the legal standing of entities attempting to enforce mortgage loans. If the ownership of the loan cannot be clearly established, the legal authority to collect payments or pursue foreclosure may be questioned. Regulators therefore examine documentation practices closely to determine whether these irregularities represent administrative mistakes or deliberate misrepresentations.

Investor Disclosure and Misrepresentation Issues

Another major area of concern for analysts investigating home loan securitization fraud is investor disclosure. When mortgage-backed securities are offered to institutional investors, detailed prospectuses and offering documents describe the characteristics of the underlying loans. These disclosures include information about borrower credit profiles, loan-to-value ratios, underwriting standards, and expected performance.

Investors rely heavily on the accuracy of this information when deciding whether to purchase mortgage-backed securities. If the loans within the securitized pool fail to meet the standards described in the offering documents, investors may argue that they were misled about the risk profile of the investment. In several high-profile cases, financial institutions have faced allegations that they misrepresented the quality of the mortgages packaged into securities.

Such misrepresentation forms a critical component of investigations into home loan securitization fraud. Analysts carefully review loan data, underwriting records, and performance histories to determine whether the loans matched the descriptions provided to investors. When discrepancies are discovered, they can trigger lawsuits, regulatory enforcement actions, and significant financial penalties for institutions involved in the securitization process.

Foreclosure Litigation and Borrower Challenges

Borrowers have also played a significant role in exposing potential cases of home loan securitization fraud. In foreclosure proceedings, homeowners sometimes challenge the legal authority of the entity attempting to enforce the mortgage. These challenges often require the foreclosing party to demonstrate a clear chain of title proving that it owns the loan and has the right to enforce it.

During these legal disputes, courts occasionally uncover documentation gaps, missing assignments, or inconsistent endorsements. While not every irregularity amounts to fraud, such findings frequently prompt deeper investigations into securitization practices. Borrower litigation has therefore become an unexpected pathway through which analysts and regulators gain insight into potential structural issues within the securitization system.

The growing awareness of these legal challenges has further intensified scrutiny of home loan securitization fraud, as regulators aim to ensure that both borrowers and investors are treated fairly within the mortgage finance system.

The Role of Forensic Audits in Detecting Securitization Issues

Forensic auditing has become an increasingly important tool in identifying potential home loan securitization fraud. These audits involve detailed examinations of loan documentation, securitization trust records, servicing reports, and regulatory filings. By comparing multiple sources of information, forensic analysts can identify discrepancies that may indicate improper transfers or inaccurate disclosures.

For example, auditors may review the pooling and servicing agreement of a securitization trust to determine whether specific loans were included in the trust at the required time. They may also analyze public property records to verify whether mortgage assignments were recorded correctly. When inconsistencies appear between these records, investigators may conclude that the securitization process did not follow the required legal structure.

The increasing availability of digital records and data analytics tools has made forensic audits far more effective. Analysts can now examine large volumes of mortgage data and identify patterns associated with home loan securitization fraud, such as repeated documentation irregularities across multiple securitization trusts or institutions.

Regulatory Oversight and Market Reforms

As investigations into home loan securitization fraud have intensified, regulators around the world have implemented new rules aimed at improving transparency and accountability in mortgage markets. These reforms often focus on strengthening disclosure requirements, enhancing documentation standards, and increasing oversight of mortgage servicers and securitization trustees.

Regulatory agencies now require more detailed reporting about the performance and composition of mortgage-backed securities. This allows analysts and investors to evaluate the risks associated with securitized loans more accurately. In addition, stricter compliance requirements have been introduced to ensure that loans are properly documented before being transferred into securitization trusts.

These regulatory efforts are designed not only to detect home loan securitization fraud but also to prevent it from occurring in the first place. By enforcing clearer documentation standards and improving transparency, regulators aim to restore confidence in mortgage-backed securities and protect both homeowners and investors.

The Growing Importance of Transparency in Mortgage Markets

Ultimately, the investigation of home loan securitization fraud reflects a broader effort to increase transparency in global housing finance systems. Mortgage securitization remains a powerful financial tool that supports lending and investment. However, its complexity requires strong oversight and reliable documentation to function properly.

When transparency is lacking, the risks associated with securitized loans can become difficult to measure, creating uncertainty for investors and borrowers alike. Regulators, analysts, and forensic auditors therefore play a critical role in examining securitization practices and identifying weaknesses that could threaten market stability.

The continued focus on home loan securitization fraud demonstrates the importance of accountability in modern financial systems. As investigative techniques improve and regulatory frameworks evolve, the mortgage industry is gradually moving toward greater transparency, stronger compliance standards, and a more resilient housing finance market.

Conclusion

The growing attention surrounding home loan securitization fraud reflects a broader effort to bring greater transparency, accountability, and integrity to the mortgage finance system. As mortgage loans are bundled into complex financial instruments and distributed across global markets, even small irregularities in documentation, loan transfers, or investor disclosures can have far-reaching consequences. Regulators and analysts therefore continue to investigate home loan securitization fraud to ensure that financial institutions follow proper legal procedures and maintain accurate records throughout the securitization process.

For investors, understanding the risks associated with home loan securitization fraud is essential when evaluating mortgage-backed securities. Accurate disclosures, reliable loan documentation, and proper chain-of-title transfers are critical elements that protect the value and legitimacy of these financial products. When these standards are not met, it can undermine investor confidence and create uncertainty in the broader housing market.

At the same time, scrutiny of home loan securitization fraud also helps protect homeowners by ensuring that the parties enforcing mortgage loans have the legal authority to do so. Through stronger regulatory oversight, improved forensic auditing techniques, and increased transparency, the financial industry can address the challenges associated with home loan securitization fraud and move toward a more trustworthy and stable mortgage lending environment.

Gain the Evidence Advantage: Elevate Your Mortgage Litigation Strategy

In today’s complex mortgage landscape, uncovering accurate financial documentation and securitization data can make the difference between uncertainty and a powerful legal strategy. When attorneys, analysts, and industry professionals need dependable insights, detailed forensic research becomes an essential tool for building stronger, evidence-based cases.

For more than four years, Mortgage Audits Online has supported professionals across the industry by delivering precise securitization and forensic audit reports designed to strengthen litigation and negotiation outcomes. Working exclusively as a business-to-business provider, our services are tailored to help legal teams, consultants, and financial professionals uncover critical information hidden within mortgage loan documentation and securitization structures.

Our experienced team conducts in-depth mortgage and securitization audits that help identify documentation inconsistencies, analyze loan transfers, and clarify the chain of title behind complex financial instruments. These insights can provide attorneys and consultants with the analytical foundation they need to challenge questionable loan documentation, validate claims, and strengthen their clients’ positions in negotiations or litigation.

When you work with us, you gain access to more than just a report—you gain a professional partner committed to delivering accuracy, reliability, and actionable insight. Our audits are prepared with careful attention to detail and structured in a clear, easy-to-understand format that supports legal review, investigation, and strategic decision-making.

If you’re ready to equip your team with powerful mortgage analysis tools and expert forensic insights, take the next step today. Discover how professional securitization audits can bring clarity to complex cases and provide your clients with a stronger path forward.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: Mortgage Audits Online Official Website

Precision. Reliability. Strategic Insight. Your Professional Advantage.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}