Why Home Loan Securitization Fraud Deserves Closer Legal and Forensic Attention

The modern mortgage industry is built on complex financial structures, layered transactions, and highly technical documentation that most borrowers never see. Behind the familiar process of signing loan papers, making monthly payments, and dealing with lenders or servicers, there is often a far more intricate system at work—one driven by securitization, loan transfers, pooled trusts, servicing agreements, and investor-backed instruments. While securitization itself is a lawful and widely used financial process, serious problems can arise when transparency breaks down, records become inconsistent, and parties involved in the loan chain fail to maintain proper compliance. This is where home loan securitization fraud becomes a matter of significant legal and forensic concern.

At its core, home loan securitization fraud refers to deceptive, misleading, manipulated, or improperly documented practices connected to the packaging, transfer, ownership, servicing, or enforcement of mortgage loans within the securitization framework. In many disputed cases, the issue is not simply whether a loan was securitized, but whether the transfers were completed lawfully, whether the documents reflect true ownership, whether servicing conduct aligns with governing agreements, and whether the entities seeking to collect or foreclose actually possess the legal authority to do so. These questions are not minor technicalities. They go directly to the integrity of the mortgage process and the rights of borrowers, investors, attorneys, and courts.

Over time, growing scrutiny has revealed that home loan securitization fraud can involve missing assignments, questionable endorsements, document fabrication, conflicting loan ownership claims, inaccurate payment histories, servicing irregularities, and inconsistencies between public land records and securitization data. In some situations, borrowers are told one party owns the loan while another party services it, and yet another entity appears in foreclosure proceedings. For legal professionals and forensic analysts, these discrepancies raise red flags that demand deeper investigation. The financial damage can be substantial, but the procedural consequences may be even more severe when courts rely on incomplete or inaccurate documentation.

The reason home loan securitization fraud deserves closer attention is that it often hides behind complexity. Many borrowers do not have the technical background to examine trust documents, pooling and servicing agreements, SEC filings, assignment records, or mortgage loan schedules. Even when irregularities exist, they may remain unnoticed unless a detailed forensic review is conducted. That is why legal and forensic attention is essential. Attorneys, auditors, and investigators must often examine whether the loan followed the required chain of transfer, whether note endorsements were valid, whether timelines were respected, and whether foreclosure actions were initiated by parties with standing. A careful review may uncover document defects, compliance failures, or procedural irregularities that materially affect the case.

Another reason home loan securitization fraud requires serious examination is that its impact extends beyond individual homeowners. Investors in mortgage-backed securities rely on accurate reporting and proper asset transfers. Courts rely on truthful evidence and lawful standing. Regulatory systems depend on clean recordkeeping and compliant servicing practices. When mortgage-related documentation is manipulated or misrepresented, the effects can ripple through multiple layers of the financial and legal system. What appears to be a simple servicing dispute may actually involve broader concerns about chain of title, trust compliance, evidence reliability, and enforcement authority.

In today’s environment, home loan securitization fraud should not be dismissed as a niche or overly technical issue. It is a legitimate field of inquiry that intersects with foreclosure defense, mortgage litigation, consumer rights, evidentiary review, and forensic auditing. When the paper trail surrounding a mortgage loan becomes inconsistent or suspicious, deeper legal and forensic analysis is not optional—it is necessary. Closer attention to home loan securitization fraud can help identify hidden irregularities, support stronger case strategy, protect due process, and bring much-needed clarity to highly contested mortgage matters.

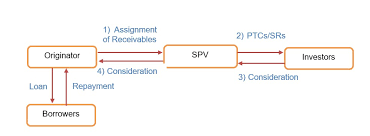

The Hidden Complexity Behind Mortgage Loan Transfers

One of the main reasons home loan securitization fraud deserves serious legal and forensic attention is the extraordinary complexity of mortgage loan transfers. In theory, the process appears straightforward: a lender originates a loan, the loan is sold, pooled with other loans, transferred into a trust, and then administered according to governing agreements. In practice, however, the actual path of a loan can become clouded by multiple entities, inconsistent records, and missing documentation. What begins as a standard real estate transaction may later involve originators, warehouse lenders, sponsors, depositors, trustees, servicers, sub-servicers, document custodians, and foreclosure firms. Each layer creates another opportunity for error, misstatement, or intentional concealment.

This complexity matters because legal enforcement depends on proof. If an entity claims the right to collect, assign, or foreclose, that claim must be supported by reliable evidence. When transfers are poorly documented or recorded after the fact, serious concerns arise about standing, ownership, and chain of title. In many contested matters, home loan securitization fraud is not merely about whether a loan entered a trust, but whether every required step was lawfully completed and properly evidenced. Even a single break in the transfer chain can trigger broader questions about whether the current claimant has enforceable rights.

Why Document Irregularities Matter in Litigation

Documentation sits at the center of every mortgage dispute. Notes, mortgages, assignments, allonges, servicing records, payment histories, default notices, and trust-related documents all carry legal significance. When these materials contain contradictions, unexplained gaps, or suspicious timing, they can dramatically affect the credibility of a case. Home loan securitization fraud often comes into sharper focus when recorded assignments appear years after a trust closing date, when signatures raise authenticity concerns, or when endorsements appear inconsistent with the transaction history being presented in court.

Courts generally expect documents to reflect an orderly and truthful sequence of events. When they do not, legal professionals must ask whether the records were created contemporaneously, whether they were altered to support litigation, or whether they were generated to repair a broken chain after the fact. In this sense, home loan securitization fraud is deeply tied to evidentiary integrity. A defective or misleading document can influence court decisions, affect a borrower’s defense strategy, and alter the course of foreclosure proceedings. Forensic review becomes indispensable because small discrepancies on paper may point to much larger structural problems beneath the surface.

The Role of Forensic Analysis in Uncovering Patterns

A proper forensic examination can reveal patterns that are not visible in a routine file review. This is why home loan securitization fraud deserves specialized analysis rather than casual observation. A forensic auditor or litigation support professional does more than read documents at face value. The work often involves comparing county land records, loan boarding data, servicing histories, investor reports, trust agreements, endorsement sequences, and signatures across multiple filings. The goal is to determine whether the documents and timelines are internally consistent and legally coherent.

This type of review is especially valuable because many securitization disputes hinge on details that are easy to overlook. A late assignment, a mismatch in loan numbers, a discrepancy in dates, or a conflict between recorded instruments and trust requirements may appear minor in isolation. Yet when examined together, those details can suggest fabrication, procedural failure, or unlawful enforcement. Home loan securitization fraud often reveals itself through cumulative inconsistencies rather than one dramatic error. That is why forensic attention can strengthen legal arguments, identify evidentiary weaknesses, and help professionals distinguish between clerical problems and potentially actionable misconduct.

Borrower Harm Is Often Greater Than It First Appears

The consequences of home loan securitization fraud are not confined to abstract financial disputes. Borrowers can face very real harm when inaccurate or deceptive securitization-related practices affect servicing, default calculations, or foreclosure actions. A homeowner may struggle to identify the true owner of the loan, receive conflicting communications from different entities, or be unable to verify whether the party demanding payment has lawful authority. In more severe situations, legal proceedings may move forward on the strength of documents the borrower has no practical ability to test without expert help.

This imbalance is one reason the issue deserves closer legal attention. Mortgage cases are often presented as routine collection matters, yet the borrower may be confronting a highly institutional system supported by vast documentation and procedural momentum. If home loan securitization fraud is present, the borrower may suffer through wrongful fees, improper default declarations, inflated reinstatement amounts, or even foreclosure actions based on questionable standing. Legal and forensic scrutiny can bring needed balance by forcing the record to be examined rather than presumed accurate.

Why Standing and Authority Remain Critical Questions

One of the most important issues in any mortgage enforcement action is whether the claimant has standing. This is where home loan securitization fraud frequently becomes central. A party cannot simply assert authority because it services the loan or appears in correspondence. It must show that it has the right to enforce the note or act on behalf of the lawful holder within the governing legal framework. When assignments are defective, endorsements are incomplete, or trust transfer requirements were not followed, that authority may be disputed.

Standing is not a procedural technicality; it is a foundational legal requirement. Without it, the legitimacy of enforcement is compromised. Yet in securitized mortgage cases, standing issues can be obscured by the sheer volume of paperwork and the assumption that institutional actors have already verified their rights. Home loan securitization fraud demands closer legal and forensic attention because those assumptions are not always justified. When lawyers and auditors examine authority carefully, they may uncover defects that substantially change the legal posture of the case.

Greater Scrutiny Can Lead to Stronger Case Strategy

The value of examining home loan securitization fraud is not limited to identifying problems. It also supports more strategic legal decision-making. When attorneys understand the transfer history, trust structure, servicing conduct, and documentary weaknesses in a mortgage file, they are better positioned to frame defenses, challenge evidence, and evaluate settlement posture. A strong forensic review may reveal issues that support discovery requests, motions practice, negotiation leverage, or trial preparation.

In high-stakes mortgage litigation, clarity is power. Cases involving home loan securitization fraud often turn on whether the factual record can withstand close examination. By investing attention in the forensic and legal details, professionals can build stronger arguments and avoid relying on surface-level assumptions. That deeper inquiry serves not only borrowers and defense counsel, but also the broader justice system, which depends on accurate documentation and lawful enforcement. For that reason, home loan securitization fraud deserves sustained scrutiny wherever mortgage records, transfers, and enforcement claims do not align with the standards required by law.

Conclusion

In conclusion, home loan securitization fraud is not an issue that should be dismissed as overly technical or legally insignificant. It sits at the intersection of mortgage documentation, loan ownership, servicing conduct, foreclosure authority, and evidentiary reliability. When records are inconsistent, assignments appear questionable, endorsements are incomplete, or the chain of title cannot be clearly established, the risk of wrongful enforcement becomes far more serious. That is why home loan securitization fraud deserves careful review from both legal and forensic perspectives.

A deeper examination of home loan securitization fraud can reveal hidden irregularities that may otherwise remain buried under complex financial language and institutional paperwork. For borrowers, attorneys, and litigation professionals, this scrutiny can help clarify whether the party seeking to collect or foreclose actually has the lawful right to do so. It can also expose procedural defects, documentation gaps, and potential compliance failures that may materially affect the outcome of a case.

Ultimately, home loan securitization fraud is about more than mortgage paperwork. It is about accountability, transparency, and due process. When legal and forensic professionals give home loan securitization fraud the attention it deserves, they help protect case integrity, strengthen legal strategy, and support a more accurate and just review of contested mortgage claims.

Turn Complex Mortgage Questions Into Stronger Legal Strategies

Unlock Clarity. Strengthen Your Case. Transform Your Client Outcomes.

When high-stakes mortgage matters demand precision, documentation, and credible forensic insight, the right audit partner can make all the difference. For over 4 years, Mortgage Audits Online has helped associates build stronger, better-supported cases through detailed securitization and forensic audits designed exclusively for the business-to-business market.

Our work is built to help professionals uncover critical details, identify document irregularities, and bring greater clarity to complex mortgage case files. When the facts need to be organized, analyzed, and presented with confidence, our professional audit support can help transform uncertainty into a more strategic path forward.

Partner with a team that understands the value of accuracy, case strength, and dependable forensic review. Give your clients the advantage of deeper analysis and equip your legal strategy with the insight it deserves.

Connect with https://www.mortgageauditsonline.com/ today and move your cases forward with greater confidence.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

Visit: https://www.mortgageauditsonline.com/

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}