Why Foreclosure Fraud Cases Are Increasing and What You Can Do

In recent years, foreclosure fraud has become a growing concern for homeowners, legal professionals, and housing advocates across the country. As financial pressures continue to affect borrowers and mortgage servicing practices become more complex, many property owners find themselves facing not only the threat of losing their homes but also the possibility that improper, misleading, or even deceptive actions may be involved in the foreclosure process. This rising pattern has made foreclosure fraud an increasingly important issue in the real estate and lending landscape, especially for those who are already under stress and uncertainty.

At its core, foreclosure fraud refers to unlawful, deceptive, or questionable practices connected to the initiation, processing, or execution of a foreclosure. These practices may involve inaccurate loan documentation, forged signatures, improper assignments, missing endorsements, robo-signing, false representations, or procedural violations committed by lenders, servicers, trustees, or third-party entities. While not every foreclosure includes misconduct, the increase in disputed filings and borrower complaints has drawn more attention to the serious legal and financial consequences that can arise when due process is ignored. As a result, foreclosure fraud is no longer viewed as an isolated issue but as a widespread risk that demands closer scrutiny.

One major reason these cases are increasing is the continued complexity of modern mortgage ownership and servicing. Loans are often transferred, bundled, sold, and managed by multiple parties over time, making it difficult to verify who truly owns the debt and who has the legal authority to enforce it. In such an environment, documentation errors can multiply, and opportunities for abuse can grow. When paperwork is incomplete, contradictory, or improperly executed, borrowers may face foreclosure actions that are based on flawed records. This is where foreclosure fraud frequently enters the picture, raising critical questions about standing, chain of title, and compliance with legal requirements.

Another contributing factor is the financial vulnerability of struggling homeowners. When borrowers fall behind on payments due to job loss, rising living costs, medical expenses, divorce, or economic instability, they often become prime targets for bad actors offering false promises of relief. Some fraud schemes involve fake foreclosure rescue services, unauthorized modification offers, or misleading legal assistance designed to exploit desperate homeowners. At the same time, institutional errors within the lending and servicing system can push already distressed borrowers deeper into crisis. The growing number of such incidents has made foreclosure fraud a key area of concern for attorneys, auditors, and housing professionals seeking to protect borrower rights.

The digitalization of records and high-volume servicing operations have also played a role in the rise of foreclosure fraud cases. While technology can improve efficiency, it can also create a system where large numbers of files are processed quickly without proper human review. When speed is prioritized over accuracy, mistakes involving notices, default calculations, ownership transfers, and affidavit execution can go unnoticed until significant damage has already occurred. In foreclosure litigation, even a small documentation defect may have major implications, which is why detailed file examination has become essential.

Understanding what you can do starts with recognizing the warning signs early. Borrowers and legal teams should carefully review mortgage documents, payment histories, notices of default, assignments, endorsements, and court filings for inconsistencies. Any unexplained discrepancy, suspicious signature, missing date, or conflicting ownership claim may warrant further investigation. Professional forensic audits and securitization reviews can help uncover evidence related to foreclosure fraud, giving attorneys and their clients stronger insight into the validity of the foreclosure action. Taking proactive steps can make the difference between reacting too late and building a well-supported defense.

As foreclosure fraud cases continue to rise, awareness, documentation, and timely investigation remain essential. Whether you are a homeowner facing uncertainty or a professional working to support a client, understanding the patterns behind these cases is the first step toward protecting legal rights and challenging questionable foreclosure activity effectively.

The Growing Role of Documentation Errors in Foreclosure Fraud Cases

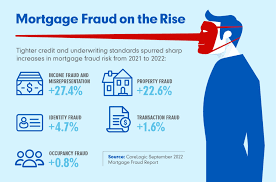

One of the most significant reasons foreclosure fraud cases continue to increase is the growing number of documentation irregularities found in mortgage and foreclosure files. In many cases, homeowners assume that if a foreclosure has been filed, the lender or servicer must have every legal right and every necessary document in place. However, closer examination often reveals missing assignments, conflicting dates, unsigned endorsements, inaccurate payment histories, and affidavits executed without proper verification. These issues are not always minor clerical mistakes. In many situations, they can directly affect the validity of a foreclosure action and raise serious concerns about whether legal procedures were properly followed.

Mortgage loans often change hands multiple times after origination. They may be sold to investors, transferred into trusts, or serviced by different entities during the life of the loan. With each transfer, the possibility of error increases. When records are not properly maintained, a foreclosure may be initiated based on incomplete or defective documentation. This is one of the most common foundations of foreclosure fraud, because it creates uncertainty over who actually owns the loan and who has the lawful authority to enforce it. For homeowners and attorneys alike, this makes detailed document review an essential part of any foreclosure-related dispute.

Another major issue is the use of standardized, high-volume processing systems by servicers and foreclosure firms. In these environments, speed often becomes more important than accuracy. Files may be pushed through automated workflows with limited human oversight, increasing the likelihood that notices are issued incorrectly, default amounts are miscalculated, or legal documents are signed without full review. In past foreclosure crises, the term robo-signing became widely known because of the mass execution of affidavits and other records without proper verification. Although public awareness of those practices has grown, concerns about similar conduct still contribute to the rise in foreclosure fraud claims today.

Why Homeowners Are More Vulnerable Than Ever

The increase in foreclosure fraud is also linked to the difficult financial realities facing many homeowners. Rising living expenses, inflationary pressure, medical debt, family emergencies, and unstable employment have left many borrowers financially stretched. When a homeowner falls behind on mortgage payments, they are often overwhelmed, frightened, and unsure where to turn. That vulnerability creates an opening not only for institutional errors in the foreclosure process but also for outside scammers who prey on desperation.

Fraudulent foreclosure rescue operations are one example. These schemes often promise to stop a foreclosure, secure a loan modification, or save a home in exchange for upfront fees. In reality, many of these operations provide little to no legitimate help. Some may instruct borrowers to stop communicating with their lender, transfer title, or make payments to unauthorized third parties. By the time the homeowner realizes something is wrong, the financial and legal situation may have worsened significantly. In this way, foreclosure fraud extends beyond lender misconduct and can also involve deceptive third-party actors who exploit borrowers during one of the most stressful times of their lives.

The emotional toll should not be underestimated either. Fear and urgency can cause people to sign documents they do not fully understand, miss critical deadlines, or fail to question suspicious claims. Many homeowners are not familiar with mortgage servicing rules, foreclosure timelines, or securitization practices, which makes it harder for them to recognize red flags. This knowledge gap is one reason foreclosure fraud can continue unchecked unless the borrower receives timely professional guidance.

How Legal and Procedural Violations Strengthen Foreclosure Fraud Concerns

Foreclosure is not simply a business process. It is a legal action that must comply with strict procedural requirements. Notices must be sent properly, deadlines must be observed, documents must be authentic, and the party bringing the foreclosure must have standing. When any of these requirements are ignored or manipulated, the case may involve elements of foreclosure fraud. Even where fraud is not conclusively proven at first glance, procedural defects can expose deeper issues that deserve investigation.

Standing is one of the most important issues in contested foreclosure matters. The party filing the foreclosure must be able to demonstrate that it has the legal right to enforce the mortgage and note. If assignments are missing, endorsements are undated, or ownership records conflict, that right may be questionable. Likewise, inaccurate default amounts, improper fees, force-placed insurance charges, and misapplied payments can all distort the basis of a foreclosure claim. These issues matter because they can shape the entire legal strategy of a defense.

For attorneys and legal support teams, this is why reviewing the chain of title, loan transfer history, and servicing records is so important. Foreclosure fraud often reveals itself through inconsistency. One document may identify a different owner than another. A signature may appear across multiple files in suspiciously uniform form. An assignment may be executed after litigation begins, raising concerns about whether the foreclosing party had authority at the time the case was filed. Each discrepancy can become a critical piece of the larger picture.

What You Can Do to Respond Effectively

The most effective response to rising foreclosure fraud is early, informed action. Waiting until the process is far advanced can reduce the number of options available. Homeowners should keep detailed records of every mortgage statement, payment confirmation, notice received, and communication with the servicer. They should review foreclosure filings carefully and compare them against their own records. Any mismatch in amounts, dates, ownership claims, or signatures should be treated seriously.

Professional review can be especially valuable in these cases. Forensic mortgage audits, document examinations, and securitization analyses can help uncover irregularities that are not obvious to the untrained eye. These tools may identify violations, defective assignments, servicing discrepancies, or evidentiary weaknesses that support a stronger legal challenge. In complex cases, the difference between assumption and documented proof can be decisive, which is why a careful investigation into foreclosure fraud is often essential.

Awareness is equally important. Homeowners should be cautious of any person or company promising guaranteed foreclosure relief, asking for large upfront fees, or urging secrecy. Verifying credentials, seeking reputable legal advice, and acting quickly can help prevent deeper harm. As foreclosure fraud continues to affect more cases, those who respond with documentation, diligence, and professional support are far better positioned to protect their rights and challenge questionable foreclosure actions.

Conclusion

In conclusion, foreclosure fraud remains a serious and growing concern that can place homeowners in an even more vulnerable position during an already difficult financial crisis. As mortgage servicing becomes more complex and foreclosure processes involve multiple entities, the risk of documentation errors, procedural violations, and deceptive practices continues to rise. This is why understanding the warning signs of foreclosure fraud is so important for borrowers, attorneys, and housing professionals alike.

From questionable loan transfers and missing assignments to misleading foreclosure rescue schemes, foreclosure fraud can take many forms, each with the potential to affect legal rights, property ownership, and financial stability. Ignoring these risks can lead to costly consequences, while early investigation and careful document review can uncover issues that may significantly impact a case.

Taking action against foreclosure fraud begins with awareness, organization, and timely support. Keeping accurate records, reviewing foreclosure documents closely, and seeking professional forensic analysis can help expose irregularities before it is too late. In today’s lending environment, vigilance is no longer optional. By recognizing the dangers of foreclosure fraud and responding strategically, homeowners and legal professionals can better protect their interests, strengthen their cases, and pursue a more informed path through the foreclosure process.

Elevate Every Case With Trusted Forensic Insight

Unlock clarity, strengthen your legal strategy, and deliver more powerful outcomes with the professional support your cases deserve. For over 4 year. Mortgage Audit Online has helped associates build stronger, more informed cases through detailed securitization analysis and forensic mortgage audits tailored for business-to-business professionals. When documentation, accuracy, and case strength matter most, working with an experienced audit partner can make a measurable difference.

Give your clients the advantage of deeper file review, sharper issue identification, and audit support designed to help you move forward with greater confidence. Partner with a team committed exclusively to serving professionals who need reliable, case-focused mortgage analysis.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

Phone: 877-399-2995

Fax: 877-398-5288

Visit: https://www.mortgageauditsonline.com/

“Disclaimer Note: This article is for educational & entertainment purposes

{kind=link}