What Happens When Your Mortgage Is Sold? Home Loan Selling & Securitizationg Insights

Homeownership is often seen as a long-term relationship between the borrower and the lender, but many homeowners are surprised to learn that their loan may be sold or transferred to another financial institution. This process, known as home loan selling & securitizationg, is a common practice in the modern mortgage industry and plays a critical role in maintaining liquidity and stability within financial markets. When a lender sells a mortgage, they transfer the rights to collect payments to another entity, which may be a bank, investor, or financial trust. While the ownership of the loan changes, the borrower’s original loan terms—including interest rate, repayment schedule, and balance—remain the same.

Understanding home loan selling & securitizationg is essential because it helps homeowners recognize why their loan may be transferred and how it impacts their financial journey. Securitization involves bundling multiple mortgages into investment products that are sold to investors, allowing lenders to free up capital and issue new loans to other borrowers. This process supports the broader housing market and ensures continued access to mortgage financing. For borrowers, it is important to know that although the loan owner may change, their legal rights and obligations remain protected. By gaining clarity on how mortgage transfers work, homeowners can feel more confident, informed, and prepared to manage their loan effectively throughout its lifetime.

Why Lenders Sell Mortgages After Closing

Many homeowners assume that the bank or lender who approved their mortgage will continue to manage the loan until it is fully repaid. However, in reality, lenders often sell mortgages shortly after closing. This is a fundamental part of the home loan selling & securitizationg process, which allows lenders to recover their funds quickly and continue offering new loans to other borrowers. Instead of waiting 15 to 30 years to receive the full repayment, lenders sell the loan to investors or financial institutions and receive immediate capital.

This practice helps maintain a continuous flow of money within the housing finance system. Without home loan selling & securitizationg, lenders would have limited resources, making it harder for new borrowers to obtain home loans. By selling mortgages, lenders reduce their financial risk, improve liquidity, and strengthen their ability to support more homeowners. This system ultimately benefits the broader economy by encouraging property ownership and financial growth.

Understanding How Mortgage Securitization Works

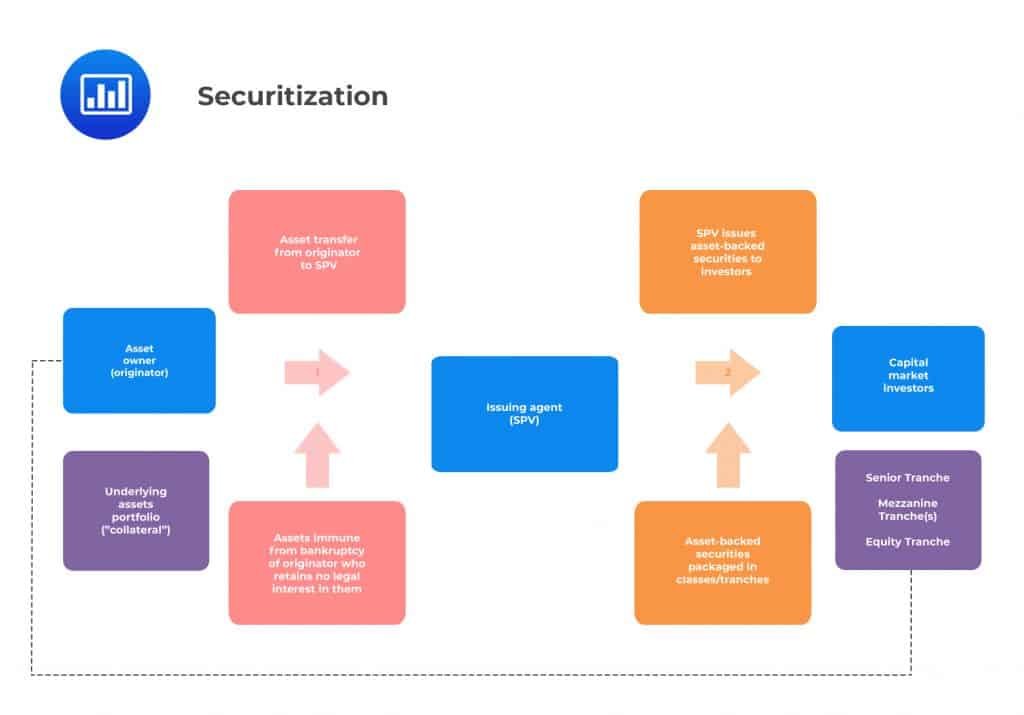

Mortgage securitization is the next stage in the home loan selling & securitizationg process. After mortgages are sold, they are often grouped together with similar loans and converted into investment products known as mortgage-backed securities (MBS). These securities are then sold to investors such as pension funds, insurance companies, and investment firms. Investors earn returns based on the mortgage payments made by borrowers.

This structured system spreads financial risk across multiple investors rather than concentrating it in one lender. It also ensures stability and efficiency in the lending market. Through home loan selling & securitizationg, lenders can continue issuing mortgages while investors gain access to relatively stable, long-term investment opportunities. This interconnected process supports both financial institutions and the housing market.

What Changes for Borrowers When a Loan Is Sold

One of the most important facts borrowers should understand about home loan selling & securitizationg is that the loan terms do not change when the mortgage is sold. The interest rate, monthly payment, repayment period, and loan balance remain exactly the same. The only difference is the entity that owns or services the loan.

Borrowers may receive a notice informing them that their loan has been transferred to a new servicer. The servicer is responsible for collecting payments, managing escrow accounts, and providing customer support. While this may seem concerning at first, it is a routine part of home loan selling & securitizationg and does not negatively affect the borrower’s agreement.

Why This Process Strengthens the Housing Finance System

The home loan selling & securitizationg system plays a crucial role in strengthening the housing finance infrastructure. It creates liquidity, reduces lender risk, and ensures that mortgage funds remain available for future borrowers. This process also supports economic growth by encouraging lending activity and housing development.

For borrowers, understanding home loan selling & securitizationg provides clarity and confidence. It explains why loan ownership changes and reassures homeowners that their rights remain protected. By recognizing how this system works, borrowers can better navigate their mortgage journey and maintain financial stability while benefiting from a well-functioning housing finance system.

Conclusion: Understanding the Bigger Picture of Mortgage Transfers

For many homeowners, learning that their mortgage has been sold can feel unexpected, but it is a normal and essential part of the modern lending system. The process of home loan selling & securitizationg ensures that lenders maintain the financial strength needed to continue offering loans to new borrowers while managing their own risk effectively. By selling mortgages and converting them into investment instruments, lenders create a continuous cycle of funding that supports both individual homeowners and the broader housing market.

It is important for borrowers to remember that home loan selling & securitizationg does not change their original loan terms, interest rate, or repayment obligations. Their agreement remains legally protected, and their responsibility continues as outlined in the original contract. The only change may be the loan owner or servicer, who will handle payment collection and account management.

Ultimately, understanding home loan selling & securitizationg empowers homeowners with knowledge and confidence. It removes uncertainty and helps borrowers recognize that this process is designed to strengthen the financial system. With the right awareness, homeowners can manage their mortgage responsibly while benefiting from a stable, efficient, and sustainable housing finance structure.

Take Command of Every Mortgage Case with Proven Securitization Intelligence

In today’s complex mortgage landscape, understanding securitization and loan transfers is no longer optional—it is essential. Mortgage Audits Online empowers legal professionals, auditors, and industry associates with precise, reliable securitization and forensic audit services designed to uncover critical loan details and strengthen case strategies. With over four years of dedicated experience, we have consistently helped our associates identify hidden securitization paths, uncover documentation gaps, and build stronger, evidence-backed cases.

As a trusted business-to-business provider, Mortgage Audits Online delivers detailed, professional audit reports that provide clarity, accuracy, and actionable insights. Our expertise enables you to confidently evaluate mortgage ownership, identify irregularities, and enhance your client advocacy with credible findings that support your objectives.

Whether you are preparing for litigation, case review, or due diligence, our team is committed to helping you achieve stronger outcomes with dependable forensic analysis and securitization research.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📞 Phone: 877-399-2995

📠 Fax: (877) 398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

{kind=link}