Understanding Mortgage-Backed Securities and the Debate around Home Loan Securitization Fraud

The modern housing finance system is deeply intertwined with complex financial instruments that move far beyond the traditional lender–borrower relationship. Among these instruments, mortgage-backed securities (MBS) have played a significant role in reshaping how home loans are issued, funded, and traded in global financial markets. Through the process known as securitization, individual mortgages are pooled together and converted into investment products that can be bought and sold by institutional investors. This system has dramatically increased the availability of mortgage credit, enabling banks and lenders to issue more home loans while transferring financial risk to investors in capital markets. However, alongside these benefits, securitization has also sparked intense debate and controversy—particularly regarding allegations of home loan securitization fraud.

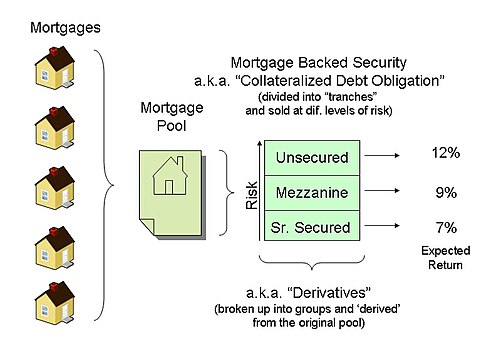

To understand the discussion around home loan securitization fraud, it is important to first grasp how mortgage securitization works. In a typical scenario, a bank or mortgage lender originates a home loan for a borrower purchasing a property. Instead of keeping the loan on its own balance sheet for the life of the mortgage, the lender sells the loan to a financial institution or a trust that bundles thousands of similar mortgages together. These bundled loans are then structured into mortgage-backed securities and sold to investors such as pension funds, insurance companies, and asset managers. This process allows lenders to recover capital quickly and issue new loans, effectively expanding the housing market.

The securitization model gained tremendous momentum in the United States through government-sponsored enterprises such as Fannie Mae and Freddie Mac, which helped standardize mortgage-backed securities and increase investor confidence in these products. Large financial institutions also entered the market aggressively, creating private-label mortgage securities that were often more complex and riskier. While securitization fueled housing growth for decades, it also introduced layers of intermediaries, documentation requirements, and financial engineering that made the system increasingly opaque.

The debate surrounding home loan securitization fraud intensified during the global financial turmoil triggered by the Global Financial Crisis. As mortgage defaults surged, many homeowners and legal analysts began questioning whether the securitization process had been executed correctly. Concerns emerged about missing paperwork, improper loan transfers, and inconsistencies in ownership records within mortgage-backed securities trusts. Critics argued that these irregularities could undermine the legal standing of lenders attempting to foreclose on properties. Supporters of this perspective claim that systemic failures in documentation and compliance may constitute home loan securitization fraud, while others argue that these issues were largely administrative errors rather than deliberate deception.

Another aspect of the controversy centers on the complexity of securitized mortgage structures. In many securitization arrangements, loans pass through multiple entities—from originators to sponsors, depositors, trustees, and servicers—before reaching investors. Each step requires strict adherence to contractual agreements known as pooling and servicing agreements (PSAs). Critics assert that when these agreements are violated or when mortgage notes are not transferred properly, the integrity of the entire securitization chain may be compromised. In such cases, allegations of home loan securitization fraud often arise, particularly when borrowers challenge foreclosure proceedings in court.

Legal scholars, regulators, and financial experts remain divided on the scope and severity of these allegations. Some argue that while documentation errors occurred, the overall framework of mortgage securitization remains legally valid and essential to the functioning of modern housing finance. Others maintain that the widespread use of electronic systems, such as those developed by Mortgage Electronic Registration Systems, created loopholes that obscured the true ownership of mortgage loans and contributed to the perception of systemic misconduct.

Today, the concept of home loan securitization fraud continues to be debated in financial, legal, and consumer advocacy circles. For homeowners facing foreclosure, the issue often centers on whether the party enforcing the mortgage can demonstrate a clear chain of ownership. For investors, it raises questions about transparency, risk management, and compliance within securitized products. Meanwhile, regulators and policymakers continue to evaluate reforms designed to strengthen documentation standards and ensure greater accountability in mortgage markets.

Ultimately, understanding home loan securitization fraud requires examining both the technical mechanics of securitization and the broader financial system that supports it. Mortgage-backed securities remain a cornerstone of global housing finance, but the controversies surrounding their implementation highlight the importance of transparency, proper documentation, and strong regulatory oversight in maintaining trust in the financial system.

.

The Evolution of Mortgage Securitization in Modern Finance

Mortgage securitization did not emerge overnight; rather, it evolved over several decades as financial institutions sought new ways to manage lending risk and increase liquidity in housing markets. Before the development of securitization, banks typically followed a traditional lending model known as “originate and hold.” Under this system, a bank would issue a mortgage loan and keep it on its balance sheet for the entire life of the loan, collecting monthly payments from borrowers until the mortgage was fully repaid. While this approach allowed lenders to maintain control over their loan portfolios, it also limited the number of mortgages they could issue because their lending capacity was tied to the amount of capital they possessed.

The emergence of mortgage-backed securities transformed this model into what became known as the “originate and distribute” system. Instead of holding loans for decades, lenders began selling them to financial institutions that pooled thousands of mortgages together and converted them into investment products. These mortgage-backed securities were then sold to investors across global financial markets. This innovation allowed lenders to free up capital quickly, enabling them to issue more loans and expand homeownership opportunities for millions of borrowers.

However, the complexity introduced by this system also laid the groundwork for concerns surrounding home loan securitization fraud. As mortgages passed through multiple financial entities before reaching investors, the documentation required to prove proper ownership and transfer of the loans became increasingly complicated. When errors or irregularities occurred in this process, critics argued that the resulting gaps in documentation could open the door to potential home loan securitization fraud.

In many cases, the securitization process involves several key participants: the loan originator, the sponsor, the depositor, the trustee, and the loan servicer. Each entity plays a distinct role in transferring the mortgage from the borrower to the investment trust that ultimately holds the loan. Because these transactions must comply with strict legal agreements, any deviation from the prescribed procedures can create disputes regarding whether the mortgage was properly transferred into the securitized trust. These disputes often become central to claims of home loan securitization fraud, particularly when homeowners challenge foreclosure actions.

The expansion of securitization also coincided with rapid innovation in financial engineering. Financial institutions created increasingly sophisticated securities, dividing mortgage pools into different risk categories known as tranches. Investors could choose tranches based on their desired level of risk and expected return. While this structure helped attract a wide range of investors, it also made the underlying mortgage assets more difficult to track and analyze. As a result, transparency in mortgage ownership became a major concern in debates surrounding home loan securitization fraud.

Documentation, Ownership, and Legal Controversies

One of the most contentious issues in discussions about home loan securitization fraud involves the documentation and legal ownership of mortgage loans. In traditional lending, the chain of ownership was relatively straightforward: the bank that issued the loan maintained possession of the mortgage note and related documentation. However, in the securitized system, mortgages are often transferred multiple times within a short period. Each transfer requires precise documentation to ensure that the ownership of the loan is legally recognized.

If the mortgage note or assignment records are missing, improperly executed, or transferred outside the timeline required by the securitization agreement, questions may arise about the legitimacy of the foreclosure process. Borrowers and legal advocates sometimes argue that these procedural deficiencies may indicate home loan securitization fraud, particularly if financial institutions attempt to enforce a mortgage without demonstrating clear ownership of the loan.

The widespread use of electronic systems to track mortgage ownership has also contributed to these controversies. These systems were designed to simplify the recording and transfer of mortgage interests without requiring repeated filings in local land records. While this approach improved efficiency for lenders, critics contend that it sometimes created confusion regarding who actually owns a mortgage at any given time. When homeowners challenge foreclosure actions, disputes over ownership records often become a focal point in arguments related to home loan securitization fraud.

Court cases across various jurisdictions have examined these issues, producing mixed outcomes. Some courts have ruled that lenders must demonstrate a complete and verifiable chain of assignments before initiating foreclosure proceedings. Other courts have concluded that minor documentation errors do not invalidate the overall securitization structure. These differing interpretations have fueled ongoing debate about the extent to which documentation irregularities constitute genuine home loan securitization fraud or simply reflect administrative shortcomings within a complex financial system.

Impact on Borrowers, Investors, and the Housing Market

The controversy surrounding home loan securitization fraud has significant implications not only for borrowers but also for investors and the broader housing market. For homeowners facing foreclosure, the question of who legally owns their mortgage can become a critical legal defense. Borrowers may seek to challenge foreclosure actions by requiring lenders to produce original loan documents and demonstrate that the mortgage was transferred properly through each stage of the securitization process.

For investors, allegations of home loan securitization fraud raise concerns about the reliability of the securities they purchase. Investors rely on accurate documentation and proper loan transfers to ensure that mortgage-backed securities are legally valid and capable of generating expected cash flows. If the underlying mortgages were not transferred correctly, investors may face financial losses or legal disputes over ownership rights.

The housing market as a whole can also be affected by these controversies. When questions arise about the legality of securitized mortgages, foreclosure proceedings may become delayed or challenged in court. These delays can create uncertainty in real estate markets and complicate efforts to resolve distressed properties. In extreme cases, widespread concerns about home loan securitization fraud could undermine confidence in mortgage-backed securities and reduce investor participation in housing finance markets.

Regulatory agencies and policymakers have attempted to address these concerns by introducing stronger documentation standards and oversight mechanisms. Financial institutions are now subject to stricter reporting requirements and compliance rules designed to ensure that mortgage transfers are properly recorded and verified. These reforms aim to reduce the likelihood of disputes related to home loan securitization fraud while preserving the benefits of securitization as a tool for expanding mortgage credit.

Transparency and the Future of Mortgage Securitization

As the financial system continues to evolve, transparency and accountability have become central themes in discussions about mortgage securitization. The lessons learned from past controversies have prompted regulators, lenders, and investors to examine how securitization practices can be improved to prevent future disputes. Greater emphasis is now placed on accurate documentation, digital recordkeeping, and clear chains of ownership for mortgage assets.

Technological advancements are also playing a role in reshaping the securitization landscape. Digital registries, blockchain-based recordkeeping systems, and enhanced data transparency tools are being explored as ways to track mortgage ownership more effectively. These innovations could help reduce errors and disputes that often contribute to allegations of home loan securitization fraud.

At the same time, consumer advocates continue to call for stronger protections for borrowers. They argue that homeowners should have access to clear information about who owns their mortgage and who has the legal authority to enforce it. Improved transparency can help prevent misunderstandings and ensure that foreclosure actions are conducted fairly and lawfully.

Despite the controversies, mortgage securitization remains a critical component of global housing finance. By allowing lenders to access capital markets, securitization provides the liquidity needed to sustain large-scale mortgage lending. However, maintaining trust in this system requires consistent oversight, accurate documentation, and ethical practices throughout the securitization process.

The ongoing debate about home loan securitization fraud reflects broader questions about accountability and transparency within modern financial systems. As regulators refine legal frameworks and financial institutions adopt more rigorous compliance standards, the goal is to ensure that mortgage securitization operates in a manner that protects borrowers, investors, and the stability of housing markets worldwide.

Conclusion

The discussion surrounding home loan securitization fraud highlights the complexities that arise when traditional mortgage lending intersects with modern financial engineering. Mortgage securitization has undeniably expanded access to housing finance by allowing lenders to convert individual home loans into investment products traded in global markets. This process has increased liquidity, encouraged investment, and supported the growth of housing markets in many countries. However, the same mechanisms that make securitization efficient also introduce layers of legal, administrative, and financial complexity.

Concerns about home loan securitization fraud typically emerge when documentation errors, unclear loan transfers, or gaps in the chain of ownership create uncertainty about who legally holds the mortgage. These issues can become especially significant during foreclosure proceedings, where borrowers may challenge the authority of institutions seeking to enforce loan agreements. For investors and regulators, allegations of home loan securitization fraud raise broader questions about transparency, compliance, and risk management within mortgage-backed securities.

Ultimately, maintaining trust in the housing finance system requires strict documentation standards, regulatory oversight, and responsible lending practices. While securitization remains an essential financial tool, addressing concerns related to home loan securitization fraud is critical for protecting borrowers, safeguarding investors, and ensuring long-term stability in the global mortgage market.

Empower Your Cases with Deeper Financial Insight

Gain clarity. Build stronger arguments. Deliver better results for your clients.

In today’s complex lending environment, accurate financial analysis can make the difference between uncertainty and a well-supported case. Our specialized securitization and forensic mortgage audits are designed to help professionals uncover critical details within loan documentation, securitization structures, and servicing practices. By providing clear, data-driven insights, we assist our associates in strengthening case strategies and presenting more compelling evidence.

For more than four years, we have worked exclusively with industry professionals—attorneys, legal teams, and financial consultants—who require reliable mortgage analysis. Our team focuses on delivering comprehensive audit reports that identify inconsistencies, verify documentation chains, and clarify complex securitization structures. This focused approach allows our partners to move forward with greater confidence when evaluating mortgage files and preparing their cases.

Because we operate strictly as a business-to-business provider, our services are tailored to meet the needs of professionals who require dependable research, detailed reporting, and consistent analytical support. Each audit is prepared with accuracy, clarity, and professional integrity in mind, ensuring that our associates receive information they can rely on when building or strengthening their legal and financial arguments.

If you are seeking deeper insight into mortgage documentation and securitization processes, our team is ready to support your work with dependable forensic analysis.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

Precision. Reliability. Insight. Your Strategic Advantage.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}