Securitization and Foreclosure Defense: What Homeowners and Attorneys Need to Know Today

The modern mortgage system has become far more complex than many homeowners realize. Over the past few decades, loans have increasingly been bundled, sold, and transferred across multiple financial institutions. This process, known as securitization, has dramatically reshaped the mortgage industry and introduced new challenges for borrowers facing foreclosure. As a result, Securitization and Foreclosure Defense has emerged as a powerful and increasingly important strategy for homeowners and attorneys seeking to understand and challenge questionable foreclosure actions.

At its core, Securitization and Foreclosure Defense focuses on examining the way mortgage loans are packaged into financial securities and sold to investors. When a homeowner signs a mortgage agreement, the expectation is often that the lender will maintain ownership of the loan. However, in many cases the loan is quickly transferred through a chain of financial transactions, sometimes passing through multiple entities before ultimately becoming part of a mortgage-backed security. While this process can provide liquidity to financial markets and expand lending opportunities, it can also create documentation gaps, ownership disputes, and compliance issues that become critically important when foreclosure proceedings begin.

For homeowners facing the threat of losing their property, understanding Securitization and Foreclosure Defense can provide valuable insight into whether the party attempting to foreclose actually has the legal authority to do so. In many foreclosure cases, the institution initiating the foreclosure may not be the original lender and may struggle to prove proper ownership of the loan. This is where careful investigation into the securitization chain becomes essential. Attorneys and forensic auditors often analyze loan transfers, assignments, pooling and servicing agreements, and trust compliance rules to determine whether the foreclosure claim is legally valid.

The growing interest in Securitization and Foreclosure Defense stems largely from the lessons learned during the global housing crisis. During that period, millions of mortgages had been rapidly securitized and transferred through complex financial structures. In many cases, documentation errors, robo-signing practices, and improper assignments were discovered. These issues revealed that the foreclosure process was not always as straightforward as lenders claimed. Courts began seeing an increasing number of cases where the foreclosing entity could not demonstrate a clear chain of title or proper legal standing.

For attorneys working in foreclosure litigation, Securitization and Foreclosure Defense has become a crucial analytical framework. By investigating how a loan was securitized, legal professionals can identify potential violations of trust agreements, improper transfers, and regulatory failures. Mortgage-backed securities typically operate under strict rules that govern how and when loans can be transferred into a trust. If those rules are not followed precisely, the entity claiming ownership may not legally hold the loan. In such situations, foreclosure actions can become vulnerable to legal challenge.

Homeowners themselves are also becoming more aware of the role Securitization and Foreclosure Defense can play in protecting their rights. Many borrowers assume that foreclosure is inevitable once payments fall behind. However, when the ownership and servicing history of a mortgage is carefully examined, discrepancies may surface that affect the legality of the foreclosure attempt. These issues can include missing assignments, improperly executed documents, or transfers that occurred after securitization deadlines.

Another important aspect of Securitization and Foreclosure Defense is the use of forensic mortgage audits. These audits involve a detailed review of loan documents, securitization records, and servicing activity to uncover irregularities. By identifying inconsistencies in the mortgage transfer process, forensic analysts can provide attorneys with critical information that may strengthen a borrower’s defense strategy. This investigative approach has become an essential tool in modern foreclosure litigation.

As mortgage markets continue to evolve, the relevance of Securitization and Foreclosure Defense continues to grow. The complexity of modern financial structures means that foreclosure cases are no longer simply about missed payments—they are also about documentation, compliance, and legal standing. For homeowners seeking clarity and attorneys building effective defense strategies, understanding the mechanics of securitization can reveal opportunities that might otherwise remain hidden.

Ultimately, Securitization and Foreclosure Defense represents more than just a legal concept; it is a framework for uncovering the truth behind mortgage ownership and ensuring that foreclosure actions follow the rule of law. By examining how loans are transferred, securitized, and enforced, homeowners and legal professionals can better navigate one of the most challenging aspects of modern real estate finance.

Next part in 1000 words following the introduction with headlines, no subheadings Use KW meaningfully.

Understanding the Structure Behind Mortgage Securitization

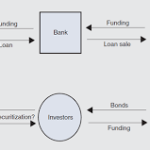

After gaining a foundational understanding of Securitization and Foreclosure Defense, the next step is recognizing how the mortgage securitization system actually works. Mortgage securitization is a financial process where individual home loans are bundled together and converted into investment products known as mortgage-backed securities. These securities are then sold to investors in financial markets. While this process may appear distant from the homeowner’s experience, it directly affects how a mortgage is owned, managed, and enforced.

In a typical securitization structure, a mortgage loan is first originated by a lender and then quickly sold to another entity, often referred to as an aggregator or sponsor. That loan may then pass through additional entities before being transferred into a trust designed to hold thousands of mortgages. Investors purchase certificates representing shares of the income generated by these loans. Servicers are then assigned to collect monthly payments from homeowners and distribute those payments to the trust.

Within the context of Securitization and Foreclosure Defense, understanding this structure is essential because it reveals how many parties may be involved in a single mortgage. When foreclosure occurs, the entity attempting to enforce the loan must demonstrate that it has the legal authority to do so. If the chain of transfers within the securitization process is incomplete or improperly documented, it may raise questions about whether the foreclosing party truly owns the loan.

For attorneys and homeowners alike, examining these transfers forms a core part of Securitization and Foreclosure Defense. Each assignment, endorsement, and transfer document must comply with both contractual requirements and legal standards. When these elements are missing or improperly executed, they can become key points of defense in foreclosure litigation.

The Importance of Chain of Title in Foreclosure Cases

One of the most critical components of Securitization and Foreclosure Defense is the examination of the mortgage chain of title. The chain of title refers to the chronological record showing how ownership of a mortgage loan has been transferred from one entity to another over time. In a properly documented system, every transfer should be recorded and traceable.

However, during periods of rapid mortgage securitization, especially in the years leading up to the housing crisis, documentation was sometimes overlooked or executed improperly. Loans were transferred between multiple institutions at high speed, and in many cases the paperwork did not keep pace with the transactions. As a result, gaps in the chain of title can appear when the loan is later reviewed in a foreclosure proceeding.

This is where Securitization and Foreclosure Defense becomes especially significant. If the entity bringing the foreclosure cannot demonstrate a complete and legally valid chain of title, the court may question whether it has standing to enforce the loan. Standing is a fundamental legal requirement in foreclosure actions, meaning that the party filing the case must prove it has the right to do so.

Attorneys who focus on Securitization and Foreclosure Defense carefully analyze recorded assignments, endorsements on the promissory note, and the timing of transfers into securitization trusts. If inconsistencies appear, they may indicate that the foreclosure process has not followed the required legal procedures.

Pooling and Servicing Agreements and Their Role in Foreclosure Defense

Another important aspect of Securitization and Foreclosure Defense involves reviewing the governing documents of securitized mortgage trusts, particularly the pooling and servicing agreement. This agreement establishes the rules that dictate how loans are transferred into the trust, how payments are handled, and how the trust operates throughout its lifetime.

Pooling and servicing agreements typically contain strict requirements regarding the timing and method of loan transfers. For example, loans may need to be transferred into the trust before a specific closing date, and the documentation for those transfers must follow precise procedures. If a loan is transferred after that deadline or without proper documentation, it may violate the terms of the trust.

When such violations occur, they can become highly relevant in Securitization and Foreclosure Defense. If the loan was never properly transferred into the securitization trust, the trust may not legally own the loan. This raises important questions about whether the trust or its servicer has the authority to initiate foreclosure proceedings.

Legal professionals often review these agreements alongside loan transfer records to determine whether the securitization process complied with the trust’s governing rules. Any deviation from those requirements may create grounds for challenging the foreclosure.

The Role of Mortgage Servicers in the Foreclosure Process

Mortgage servicers play a central role in the administration of securitized loans, and their actions are frequently scrutinized within Securitization and Foreclosure Defense. Servicers are responsible for collecting payments, managing escrow accounts, communicating with borrowers, and initiating foreclosure proceedings when necessary.

Although servicers act on behalf of the loan owner or securitization trust, they do not necessarily own the loan themselves. This distinction can become significant during foreclosure litigation. When a servicer files a foreclosure action, it must demonstrate that it has the authority to act on behalf of the loan owner.

Within Securitization and Foreclosure Defense, attorneys often investigate whether the servicer has properly documented its authority. This may involve reviewing servicing agreements, power-of-attorney documents, or trust authorizations. If the servicer cannot clearly demonstrate its authority to enforce the loan, the foreclosure case may face legal challenges.

Servicers are also responsible for maintaining loan records and payment histories. Errors in these records can sometimes lead to disputes about the borrower’s payment status or the accuracy of the foreclosure claim. Careful review of servicing activity can therefore become another critical component of Securitization and Foreclosure Defense.

How Forensic Mortgage Analysis Supports Legal Defense Strategies

Forensic mortgage analysis has become an increasingly valuable tool in Securitization and Foreclosure Defense. This process involves conducting a detailed examination of the mortgage loan’s documentation, transfer history, securitization records, and servicing activity. The goal is to identify irregularities, inconsistencies, or violations that may affect the legality of the foreclosure.

A forensic audit may review multiple layers of documentation, including the original loan documents, recorded assignments, securitization filings, trust agreements, and servicing records. By analyzing these materials together, forensic analysts can reconstruct the history of the loan and determine whether the securitization process followed the required legal and contractual procedures.

The findings of a forensic analysis can provide attorneys with valuable evidence when preparing a defense strategy. For example, an audit might reveal that a loan was transferred into a securitization trust after the trust’s closing date or that an assignment was executed by an entity that no longer held the loan. These types of discrepancies may become important issues in foreclosure litigation.

In many cases, Securitization and Foreclosure Defense relies on this investigative approach to uncover details that are not immediately visible in standard foreclosure filings. By carefully examining the documentation trail behind a mortgage loan, legal professionals can better assess whether the foreclosure process complies with the law.

The Evolving Importance of Securitization Analysis in Modern Foreclosure Cases

As financial markets continue to evolve, the role of Securitization and Foreclosure Defense remains highly relevant. Mortgage loans are still widely securitized, and the legal complexities associated with these financial structures continue to affect foreclosure litigation. Courts today are often more familiar with securitization issues than they were in the past, but disputes over loan ownership and documentation still arise.

For homeowners, gaining insight into how securitization affects their mortgage can help clarify the foreclosure process and highlight potential areas of legal defense. For attorneys, the careful analysis of securitization structures provides an additional layer of strategy when challenging foreclosure claims.

Ultimately, Securitization and Foreclosure Defense serves as a powerful framework for understanding the intersection between modern finance and property law. By examining the structure, documentation, and compliance requirements behind securitized mortgages, legal professionals can uncover critical details that influence the outcome of foreclosure cases.

In today’s complex mortgage environment, understanding Securitization and Foreclosure Defense has become increasingly important for both homeowners and legal professionals. Mortgage securitization transformed the housing finance system by allowing loans to be bundled, sold, and traded across global markets. While this system increased liquidity and expanded lending opportunities, it also created intricate ownership structures that can complicate foreclosure proceedings. Because mortgages often pass through multiple entities before reaching a securitized trust, verifying the true holder of the loan and the legal right to enforce it can be challenging.

This is where Securitization and Foreclosure Defense plays a crucial role. By carefully examining loan transfers, assignments, servicing records, and securitization documents, attorneys can determine whether foreclosure actions meet the legal standards required by courts. Issues such as incomplete documentation, improper loan transfers, or unclear authority of servicers may significantly impact foreclosure cases. Although these defenses do not eliminate a borrower’s financial obligations, they can ensure that lenders follow proper legal procedures.

Ultimately, Securitization and Foreclosure Defense emphasizes transparency, accountability, and due process within the foreclosure system. For homeowners facing the risk of losing their property, understanding these legal principles may provide important opportunities to challenge improper foreclosure actions, negotiate alternatives, and protect their rights under the law.

Unlock Clarity. Strengthen Your Case. Transform Your Client Outcomes

In today’s complex mortgage litigation environment, success depends on more than assumptions—it requires documented evidence, clear analysis, and professional insight. When questions arise about securitization, loan ownership, or documentation integrity, having a trusted forensic audit partner can make the difference between uncertainty and a strong, well-supported legal strategy.

For more than four years, Mortgage Audits Online has helped legal professionals, investigators, and industry associates build stronger cases through comprehensive securitization and forensic mortgage audits. Working exclusively as a business-to-business service provider, our focus is on empowering attorneys and professional partners with detailed, evidence-driven reports that expose critical loan data, identify documentation inconsistencies, and clarify complex securitization structures. These insights can strengthen litigation preparation, enhance negotiation leverage, and support more confident decision-making for your clients.

Our team combines deep industry expertise with a meticulous analytical approach. Each audit is designed to uncover hidden details within mortgage documentation, track loan transfers through securitization pathways, and highlight discrepancies that could influence case strategy. By transforming complex mortgage data into structured, court-ready insights, we help professionals turn uncertainty into actionable intelligence.

When clarity, documentation, and credibility matter most, partnering with the right forensic mortgage audit provider can elevate your case preparation and professional impact. Instead of navigating the complexities of securitized loans alone, equip your practice with reports built to support high-stakes decisions and strengthen legal arguments.

Connect with Mortgage Audits Online today and give your cases the analytical depth they deserve.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

“Disclaimer Note: This article is for educational & entertainment purposes

{kind=link}