How Banks Structure Mortgage Deals and the Risk of Home Loan Securitization Fraud

The modern mortgage market is built on complex financial structures that most borrowers rarely see or fully understand. While a home loan may appear to be a simple agreement between a borrower and a lender, the reality behind the scenes is far more intricate. In today’s global financial system, banks frequently package and sell mortgages to investors through a process known as securitization. This practice helps lenders maintain liquidity, spread risk, and generate capital for issuing new loans. However, the same system that fuels financial growth can also create opportunities for manipulation, misrepresentation, and legal irregularities. At the center of these concerns lies the increasingly discussed issue of home loan securitization fraud.

When a borrower signs a mortgage agreement, they typically believe the lending bank will retain ownership of the loan for the duration of repayment. In many cases, however, the loan is quickly transferred into large investment pools known as mortgage-backed securities (MBS). These securities are then sold to institutional investors such as pension funds, hedge funds, and insurance companies. Through this process, thousands of individual mortgages are bundled together and transformed into tradable financial products. While securitization itself is a legitimate financial mechanism, the lack of transparency in some transactions has raised serious questions regarding home loan securitization fraud and the potential harm it can cause to borrowers.

One of the key issues associated with home loan securitization fraud is the breakdown in clear loan ownership and documentation. As mortgages move through multiple financial entities—including originators, servicers, trustees, and investors—paperwork may become inconsistent or incomplete. In some cases, loan assignments are executed after the fact or recorded inaccurately. This creates a situation where the true holder of the mortgage may not be clearly identifiable, which can become particularly problematic during foreclosure proceedings. Borrowers facing foreclosure have sometimes discovered that the institution attempting to enforce the loan cannot provide a clear chain of ownership, raising significant legal and ethical concerns related to home loan securitization fraud.

Another dimension of home loan securitization fraud involves the misrepresentation of loan quality within mortgage-backed securities. During periods of aggressive lending, particularly in the years leading up to the 2008 financial crisis, some financial institutions packaged risky or poorly underwritten loans into securities that were marketed as stable investments. Investors relied heavily on credit ratings and bank disclosures that did not always reflect the true level of risk embedded in the loan pools. This lack of transparency allowed problematic lending practices to spread throughout the financial system, contributing to widespread market instability and renewed scrutiny of home loan securitization fraud practices.

Borrowers may also be affected by servicing irregularities linked to home loan securitization fraud. Loan servicing companies, which collect payments and manage mortgage accounts, sometimes operate separately from the original lender. When loans are transferred repeatedly between servicing companies, errors in payment records, escrow calculations, or communication can occur. In extreme cases, borrowers have faced wrongful foreclosure actions due to flawed documentation or administrative mistakes tied to securitized mortgage structures. These incidents highlight how the complexity of modern financial systems can expose borrowers to risks they never anticipated when signing their loan agreements.

Legal experts and financial analysts have increasingly turned to forensic mortgage audits to uncover signs of home loan securitization fraud. These audits examine loan documents, securitization filings, assignment records, and trust agreements to determine whether the mortgage was properly transferred and whether the parties involved followed required procedures. By analyzing these records, professionals can identify irregularities that may affect the enforceability of the loan or reveal potential violations of financial regulations.

Understanding home loan securitization fraud is essential not only for borrowers but also for attorneys, financial professionals, and consumer advocates who seek greater transparency within the mortgage industry. As mortgage markets continue to evolve and financial instruments grow more sophisticated, the need for accountability and clear documentation becomes increasingly important. By examining how banks structure mortgage deals and recognizing the risks embedded in securitization practices, individuals can better navigate the complexities of the modern lending landscape and protect themselves from potential financial harm.

The Mechanics of Mortgage Securitization in Modern Banking

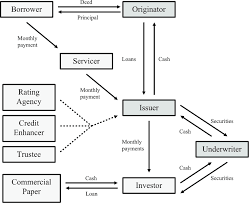

To understand how home loan securitization fraud can occur, it is essential to first examine how mortgage securitization works in the modern financial system. Mortgage securitization is a structured financial process through which banks convert individual home loans into investment products. Instead of holding mortgages on their balance sheets for decades, lenders bundle multiple loans together and sell them to investors through mortgage-backed securities (MBS). This process allows banks to recover capital quickly, enabling them to issue more loans and maintain liquidity in the financial market.

The securitization process typically begins when a borrower obtains a mortgage from a lending institution. Shortly after the loan is issued, the lender may sell it to a larger financial entity or aggregator. These aggregators collect thousands of similar loans and transfer them into a financial trust. Once placed in the trust, the mortgages are structured into securities that are sold to institutional investors. Investors then receive payments generated from the borrowers’ monthly mortgage installments.

While this system provides significant financial efficiency, it also introduces layers of complexity that make tracking ownership difficult. Each transfer—from the lender to the aggregator, from the aggregator to the trust, and eventually to investors—requires precise documentation and compliance with strict legal standards. When these standards are not followed properly, irregularities may emerge, creating conditions where home loan securitization fraud becomes possible.

In many situations, borrowers remain unaware that their loan has been transferred multiple times. Their payments continue through the loan servicer, giving the impression that the original bank still controls the mortgage. However, behind the scenes, ownership may have shifted through several entities, increasing the risk of errors or manipulation within the securitization chain.

Documentation Breakdowns and Chain of Title Problems

One of the most significant issues associated with home loan securitization fraud involves documentation breakdowns and disruptions in the chain of title. The chain of title refers to the documented history of ownership transfers for a mortgage loan. For a foreclosure action or legal enforcement to be valid, the institution seeking repayment must demonstrate a clear and continuous chain of ownership.

In an ideal securitization structure, every transfer of the mortgage is recorded accurately through legally binding assignments. These assignments confirm that the loan has been properly transferred from one party to another. However, during periods of aggressive mortgage lending, documentation standards were sometimes overlooked or handled improperly. As a result, missing assignments, backdated documents, and incomplete records began appearing in mortgage files.

These documentation gaps can create serious legal challenges. If a financial institution attempts to foreclose on a property without demonstrating a clear chain of title, courts may question whether that entity has the legal authority to enforce the loan. Such scenarios have led to increased scrutiny of home loan securitization fraud, particularly when lenders attempt to correct missing paperwork after foreclosure proceedings have already begun.

Another concern arises when multiple entities claim rights to the same loan due to conflicting documentation. When mortgages pass through several financial institutions, inaccurate records can result in overlapping ownership claims. This situation not only creates confusion for borrowers but also highlights the systemic vulnerabilities that can enable home loan securitization fraud to occur within complex mortgage structures.

Investor Misrepresentation and Risk Concealment

Beyond documentation issues, home loan securitization fraud may also involve the misrepresentation of loan quality to investors. Mortgage-backed securities are marketed as investment products that generate income from homeowner payments. Investors rely on detailed disclosures about the loans included in these securities, including information about borrower creditworthiness, loan-to-value ratios, and underwriting standards.

However, during periods of intense market competition, some financial institutions packaged high-risk mortgages into securities that were presented as stable investments. Loans that should have been categorized as high risk were sometimes blended with stronger mortgages, masking their potential for default. Investors purchasing these securities often relied on credit ratings and bank representations that did not accurately reflect the underlying risk.

When these misrepresentations occur, the consequences can ripple throughout the financial system. Investors may suffer substantial losses when loan defaults increase, while borrowers may face aggressive collection practices from servicers seeking to recover investor funds. In such circumstances, investigations frequently reveal structural weaknesses and deceptive practices associated with home loan securitization fraud.

The global financial crisis demonstrated how widespread these issues could become when securitization structures are not properly regulated. As loan defaults increased, the underlying weaknesses within mortgage-backed securities became visible, prompting regulatory agencies and legal professionals to examine how misrepresentations contributed to systemic financial instability.

Loan Servicing Complications and Borrower Impact

Another area where home loan securitization fraud may emerge involves the servicing of securitized mortgages. Loan servicers are responsible for collecting monthly payments, managing escrow accounts, handling borrower inquiries, and overseeing delinquent accounts. In securitized mortgage structures, the servicer operates on behalf of investors who own the loan through the securitization trust.

Because servicers act as intermediaries, borrowers often have limited visibility into who actually owns their mortgage. This separation can create situations where servicers pursue aggressive collection strategies that prioritize investor returns rather than borrower solutions. Additionally, when servicing rights are transferred between companies, errors in payment histories and account records may occur.

Borrowers have occasionally reported unexplained payment discrepancies, inaccurate late fees, or sudden changes in servicing policies after their loan was transferred. In extreme cases, foreclosure proceedings have been initiated even when borrowers believed they were current on their payments. These disputes frequently raise questions about whether the servicer possesses the proper authority to act on behalf of the securitization trust.

Such complications reinforce concerns surrounding home loan securitization fraud, particularly when documentation inconsistencies or servicing irregularities appear during foreclosure proceedings. Legal experts often review servicing records alongside securitization documents to determine whether the loan has been administered in accordance with the trust’s governing agreements.

Forensic Mortgage Audits and Legal Investigations

As awareness of home loan securitization fraud has grown, forensic mortgage audits have become an important investigative tool for attorneys, financial analysts, and consumer advocates. A forensic mortgage audit is a detailed examination of loan documentation, securitization records, and compliance procedures to determine whether a mortgage was transferred and administered according to applicable laws and agreements.

During such an audit, professionals review key documents including the promissory note, mortgage assignments, pooling and servicing agreements, and securitization filings. These records help establish whether the mortgage was legally transferred into the securitization trust and whether the parties involved complied with the trust’s operational guidelines.

If discrepancies are discovered—such as missing assignments, improperly executed transfers, or violations of trust agreements—these findings may become relevant in legal disputes. Attorneys sometimes use audit results to challenge foreclosure actions, negotiate loan modifications, or seek remedies for borrowers who believe their mortgage has been mishandled.

Forensic investigations also play a role in identifying broader patterns of home loan securitization fraud across multiple loans within the same securitization pool. By analyzing documentation across many mortgages, analysts may detect systemic practices that suggest widespread procedural violations rather than isolated administrative errors.

As mortgage markets continue evolving, financial transparency remains essential for maintaining trust between lenders, investors, and borrowers. Increased regulatory oversight, improved documentation standards, and advanced forensic analysis tools are helping uncover irregularities that once remained hidden within complex financial structures. Through careful examination and accountability, the financial industry can work toward minimizing the risks associated with home loan securitization fraud while preserving the benefits that securitization brings to global mortgage markets.

Conclusion

In conclusion, understanding the complexities of mortgage finance is essential for borrowers, investors, and legal professionals navigating today’s lending environment. While securitization has become a standard practice that allows banks to generate liquidity and expand lending opportunities, the intricate structure of mortgage transfers can also create vulnerabilities within the financial system. When documentation errors, misrepresentation of loan quality, or improper servicing practices occur, the risk of home loan securitization fraud increases significantly.

The presence of multiple parties involved in a securitized mortgage—from originators and aggregators to trusts and servicers—makes transparency and accurate recordkeeping absolutely critical. Any break in the chain of title, missing assignment, or irregular documentation can raise serious questions about loan ownership and enforcement rights. For borrowers facing disputes or foreclosure, uncovering potential home loan securitization fraud may reveal critical information about whether the entity attempting to enforce the loan has the legal authority to do so.

As awareness grows, forensic mortgage audits and legal investigations continue to play an important role in identifying possible instances of home loan securitization fraud. By examining loan transfers, securitization records, and servicing activities, professionals can detect irregularities that may otherwise remain hidden. Ultimately, greater transparency, stronger regulatory oversight, and informed borrowers are essential steps toward reducing the risks associated with home loan securitization fraud in the modern mortgage industry.

Gain the Insight That Strengthens Every Mortgage Case

In complex mortgage disputes, clarity can make the difference between uncertainty and a well-prepared legal strategy. With the increasing complexity of loan transfers, securitization structures, and servicing practices, attorneys, consultants, and financial professionals need reliable forensic insight to uncover the truth behind mortgage transactions. That’s where professional securitization analysis and forensic mortgage audits become powerful tools.

For more than four years, our team has helped professional associates strengthen their case preparation through detailed securitization reviews and forensic mortgage audits. Working exclusively as a business-to-business service provider, we focus on supporting attorneys, consultants, and industry professionals with precise documentation analysis, chain-of-title reviews, and securitization tracing designed to reveal critical details within complex loan files. Our goal is simple: deliver accurate information that empowers professionals to build stronger, more confident cases.

At Mortgage Audits Online, our audits are designed to uncover documentation inconsistencies, securitization pathways, and compliance issues that may otherwise remain hidden within extensive loan records. These insights can support litigation strategy, negotiation preparation, and financial investigations. With years of industry expertise and a commitment to dependable analysis, our team provides the clarity and evidence professionals need when navigating complicated mortgage disputes.

If you are ready to strengthen your case preparation with dependable forensic insight, connect with our team today and discover how professional mortgage audits can support your legal and financial strategies.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: Mortgage Audits Online Official Website

Precision. Reliability. Expertise. Your Strategic Edge.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}