Hidden Risks Behind Home Loan Securitization Fraud in Modern Mortgage Cases

In today’s complex lending environment, home loan securitization fraud has become an increasingly discussed issue in modern mortgage disputes, foreclosure defense strategies, and forensic loan investigations. What appears on the surface to be a standard mortgage transaction may, in some cases, involve a far more complicated chain of ownership, assignment activity, document transfers, and securitization practices that raise serious legal and procedural concerns. For borrowers, attorneys, legal support professionals, and industry observers, understanding the deeper mechanics behind home loan securitization fraud is essential because the consequences can affect standing, enforceability, transparency, and the overall integrity of a mortgage case.

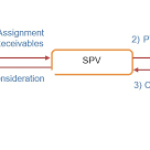

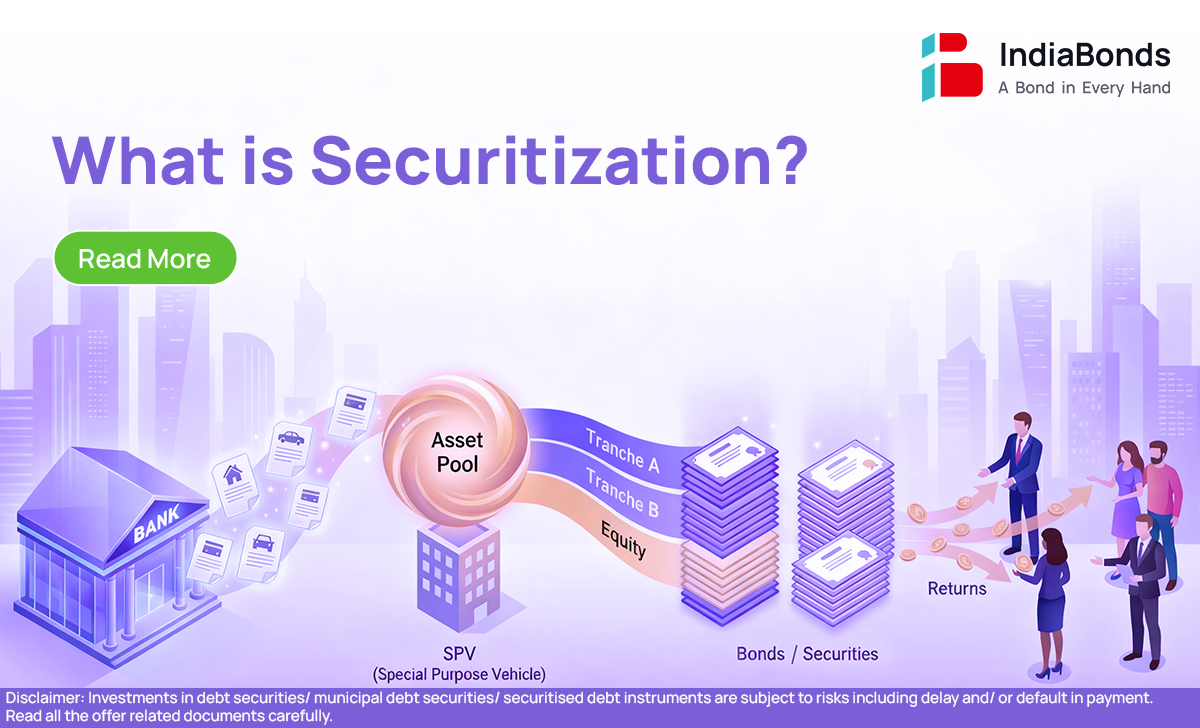

At its core, mortgage securitization was designed to convert individual home loans into tradable financial instruments that could be sold to investors in pooled trusts. In principle, this process created liquidity in the housing market and expanded access to lending. However, the practical execution of securitization has not always followed a clean, well-documented path. In many disputed cases, questions arise over whether the note and mortgage were transferred correctly, whether assignments were executed in a timely and lawful manner, whether the trust actually acquired the loan under its governing rules, and whether the party attempting enforcement has the legal authority to do so. These are the areas where home loan securitization fraud becomes a major point of concern.

One of the hidden risks tied to home loan securitization fraud is the masking of broken title chains behind layers of servicing activity and institutional paperwork. Borrowers are often told that a servicer, trustee, or substituted entity has the right to collect, enforce, or foreclose, yet the underlying documentation may reveal inconsistencies, gaps, robo-signed assignments, conflicting dates, or transfers that appear to fall outside the terms of the securitization trust. These issues are not always immediately visible without a detailed forensic review. That is why this topic has become so important in contested mortgage cases, especially where documentation appears polished on the surface but raises substantive questions upon closer analysis.

Another reason home loan securitization fraud continues to draw attention is because modern mortgage litigation often depends on documentary precision. A single improperly executed assignment, a missing endorsement, or an unexplained gap in possession can create critical legal questions. When such defects are combined with questionable servicing conduct, payment misapplication, or fabricated loss mitigation histories, the borrower may be facing not just administrative confusion but a potentially systemic pattern of irregularities. In this context, home loan securitization fraud is not merely about technical defects. It may point to a broader failure of compliance, disclosure, and lawful transfer practices that can influence the outcome of a case.

The hidden nature of these risks is what makes the issue especially significant. Most borrowers do not have access to securitization documents, trust agreements, servicing records, custodial certifications, or investor reporting data at the beginning of their case. As a result, problems linked to home loan securitization fraud may remain concealed until a detailed audit or legal discovery process uncovers discrepancies. By that stage, the borrower may already be deep into default proceedings, foreclosure litigation, or post-judgment challenges. This delay in discovery can place homeowners at a serious disadvantage, especially when they are confronting institutions with extensive legal and procedural resources.

For legal professionals and investigators, the study of home loan securitization fraud offers an opportunity to move beyond surface-level pleadings and examine the actual history of the loan. It requires close attention to assignment sequences, trust closing dates, note endorsements, SEC filings where applicable, and the relationship between the named plaintiff and the debt being enforced. These details can become central in determining whether a case rests on valid documentation or on a structure weakened by irregular transfers and questionable representations.

As mortgage disputes continue to evolve, home loan securitization fraud remains one of the most critical hidden issues shaping modern mortgage cases. Its risks are often buried beneath technical language, institutional complexity, and delayed document production, but its impact can be profound. A careful, informed review is often the first step toward exposing weaknesses that might otherwise remain hidden in the modern mortgage system.

Why the Chain of Title Matters in Every Mortgage Dispute

One of the most important issues in any contested mortgage matter is the chain of title, because it reveals whether the right party truly holds the legal authority to enforce the debt. In cases involving home loan securitization fraud, the chain of title often becomes the foundation of deeper investigation. A mortgage may be originated by one lender, transferred to another entity, sold into a securitized trust, serviced by a third-party company, and later enforced by yet another institution acting in a trustee or servicing capacity. On paper, that structure may seem routine. In practice, however, every transfer must be supported by valid documentation, proper timing, and legal consistency. When those elements are missing, the entire enforcement narrative can weaken.

In many modern mortgage disputes, borrowers discover that recorded assignments were created years after the alleged trust transfer date or were executed only after default had already occurred. This creates suspicion that documents were generated to repair gaps rather than to reflect actual historical transactions. Such inconsistencies are often central to claims or defenses tied to home loan securitization fraud, because they raise the question of whether the foreclosing party is relying on authentic loan history or on reconstructed paperwork intended to establish standing retroactively. When a case depends on documents prepared after the fact, the reliability of the foreclosure record may come under serious scrutiny.

The Role of Mortgage Servicers in Document and Payment Conflicts

Mortgage servicers play a major role in how borrowers experience the loan after origination, yet servicers are not always the actual owners of the debt. This distinction matters greatly in cases connected to home loan securitization fraud. A servicer may send monthly statements, collect payments, issue default notices, and manage foreclosure proceedings, but its authority comes from contracts and delegations that are often invisible to the borrower. If the servicer cannot clearly demonstrate who owns the loan and how servicing rights were established, confusion grows quickly.

Servicing problems often overlap with securitization-related concerns. Borrowers may encounter unexplained fee increases, misapplied payments, inconsistent account histories, sudden changes in creditor identity, or contradictory notices from multiple entities. These issues may appear administrative at first, but they can become highly significant when combined with flawed assignments or missing note endorsements. In cases involving home loan securitization fraud, the servicer’s records may not align with trust documents, investor data, or public land records. That mismatch can suggest that the servicing platform is operating on assumptions rather than verified legal ownership. Forensic review of payment histories, default calculations, and communication logs often becomes essential in exposing those inconsistencies.

Trust Closing Dates and Transfer Violations

A securitized mortgage trust usually operates under a strict governing framework that outlines when and how loans must be transferred into the trust. These rules are often contained in pooling and servicing agreements or similar trust instruments. In disputes involving home loan securitization fraud, trust closing dates are frequently examined because they may reveal whether the loan was ever transferred into the trust in the manner claimed by the enforcing party.

If a loan is assigned into a trust long after the trust’s closing date, serious questions can arise. The transfer may conflict with the trust’s governing documents, investor representations, or tax-related requirements. While the legal consequences of such violations can vary depending on jurisdiction and case strategy, the factual discrepancy itself is often highly relevant. It may suggest that the trust was named as the holder for litigation convenience rather than because it lawfully acquired the loan at the required time. This is one reason home loan securitization fraud has become such a vital topic in foreclosure defense and mortgage audits. It is not only about whether a document exists, but whether that document reflects a transaction that could legally and contractually occur in the way described.

Questionable Assignments and the Problem of Manufactured Paper Trails

Many contested mortgage files include assignments that appear facially valid but raise troubling questions upon closer review. Signatures may belong to individuals who signed on behalf of multiple institutions, dates may conflict with known business records, notary information may appear irregular, or the same document preparers may appear repeatedly across unrelated files. These patterns have led many investigators to focus on whether the mortgage file reflects genuine transactional history or a manufactured paper trail. This is one of the clearest warning areas in matters involving home loan securitization fraud.

A manufactured paper trail can be especially damaging because courts, servicers, and borrowers often rely heavily on recorded documents. Once an assignment is placed into the public record, it may carry an appearance of legitimacy even if the underlying transfer never happened as stated. That appearance can shape litigation strategy, settlement pressure, and judicial assumptions. Yet a deeper review may reveal that the document was executed by an entity with no real authority, by a signatory lacking corporate capacity, or on a date that contradicts the alleged ownership timeline. In such situations, home loan securitization fraud is not just a theory. It becomes a practical concern tied directly to whether the foreclosure machinery is operating on valid evidence.

Why Forensic Review Has Become So Important

The complexity of modern mortgage transactions means that surface review is rarely enough. A forensic loan analysis can identify discrepancies that ordinary document review might miss, including securitization mismatches, endorsement defects, improper assignments, inconsistent default amounts, and signs of document fabrication. In the context of home loan securitization fraud, forensic review is often the bridge between suspicion and documented evidence.

This process may involve comparing county land records, loan servicing histories, securitization trust data, recorded assignments, note copies, allonges, and court filings. It also means examining the chronology carefully. When was the loan originated, when was it supposedly transferred, who serviced it at each stage, and when did enforcement begin? If the answers do not align, the case may contain material weaknesses. Because home loan securitization fraud can hide behind technical language and institutional complexity, careful document correlation is often the only way to expose the true status of the loan.

The Broader Impact on Borrowers and Legal Strategy

The danger of home loan securitization fraud extends far beyond paperwork defects. For borrowers, it can mean defending against a party that may not have proper standing, facing inflated arrears, or being pressured into negotiations without full disclosure of who actually controls the debt. For legal professionals, it can change the entire direction of a case. Issues once treated as minor technicalities may become central to motions, discovery requests, affirmative defenses, or settlement leverage.

As modern mortgage litigation grows more document-driven, the risks linked to home loan securitization fraud continue to shape both borrower rights and case outcomes. Hidden irregularities in transfers, trust compliance, servicing authority, and document execution can affect every stage of a mortgage dispute. That is why meaningful investigation is no longer optional in many contested cases. It is often the key to identifying whether the mortgage file reflects lawful ownership and enforceable rights, or whether it conceals structural weaknesses that deserve closer legal examination.

Expose the Details. Elevate the Strategy. Empower Every Case.

When mortgage disputes involve complex documentation, securitization concerns, and hidden case weaknesses, the right audit partner can make all the difference. For more than 4 years, we have helped our associates build stronger cases through detailed securitization reviews and forensic mortgage audits designed to uncover critical findings with precision and professionalism.

As an exclusively business-to-business provider, Mortgage Audits Online is committed to supporting professionals who need reliable analysis, well-documented findings, and deeper insight into complex mortgage case files. Our work is designed to help you move forward with greater confidence, sharper strategy, and stronger case positioning.

When clarity, documentation, and professional insight matter most, working with the right forensic mortgage audit partner can transform uncertainty into strategic advantage. Connect with Mortgage Audits Online today and equip your cases with the depth of analysis and credibility they deserve.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

Phone: 877-399-2995

Fax: 877-398-5288

Website: www.mortgageauditsonline.com

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}