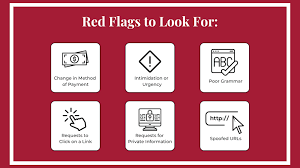

Common Red Flags That May Indicate Foreclosure Fraud

Foreclosure fraud is a serious issue that can place already vulnerable homeowners in even greater financial and legal jeopardy. During the foreclosure process, borrowers are often under intense pressure, facing missed payments, lender notices, legal confusion, and the fear of losing their homes. Unfortunately, this stressful environment can attract deceptive individuals, fraudulent service providers, and dishonest schemes that take advantage of people who are desperately searching for relief. Recognizing the warning signs early is essential because a single misleading promise or suspicious document can result in even deeper financial losses, delayed legal action, or the permanent loss of critical rights.

In many cases, foreclosure fraud does not appear obvious at first. It may come in the form of a company guaranteeing a loan modification, a so-called foreclosure rescue specialist asking for upfront fees, or a third party pressuring a homeowner to sign documents without proper review. Some fraudsters present themselves as legal experts, housing counselors, investigators, or consultants, using polished language and urgent claims to appear credible. They often target distressed homeowners by promising immediate solutions, fast approvals, or guaranteed outcomes that legitimate professionals simply cannot assure. These tactics are designed to build false trust while concealing the true purpose behind the transaction.

Understanding the nature of foreclosure fraud is especially important because homeowners in distress are often focused on immediate survival rather than long-term consequences. When someone is worried about keeping a roof over their head, they may be more likely to believe unrealistic promises, overlook suspicious contract terms, or pay fees to anyone who claims they can stop the foreclosure quickly. Fraudulent actors rely on emotional pressure, confusion, and lack of documentation to move their schemes forward. That is why awareness is not just helpful but necessary. Knowing what to question, what to verify, and when to seek trusted guidance can make a meaningful difference.

Another challenge with foreclosure fraud is that it can involve forged signatures, hidden transfer agreements, misleading foreclosure rescue offers, fake government affiliations, or requests to redirect mortgage payments. In some situations, homeowners may not even realize they have been deceived until title documents are altered, deadlines are missed, or promised services never materialize. By then, the damage can be difficult and expensive to reverse. That is why identifying red flags early in the process can help borrowers protect both their homes and their legal interests.

The topic of foreclosure fraud also matters to attorneys, auditors, paralegals, and legal support professionals who work with foreclosure-related matters. Suspicious timelines, inconsistent loan records, questionable assignments, unexplained fees, and aggressive third-party involvement may all signal the need for closer review. A careful examination of the paperwork and transaction history may reveal irregularities that deserve further attention. In many foreclosure-related disputes, strong documentation and timely investigation play an important role in uncovering potential misconduct.

As foreclosure activity continues to affect homeowners across different markets, staying informed about the common red flags linked to foreclosure fraud becomes increasingly important. Awareness can help individuals avoid manipulation, preserve essential records, and respond more strategically when facing foreclosure threats. From unrealistic guarantees to secretive paperwork and pressure-based tactics, the signs of fraud are often present before the full scheme becomes clear. Learning to identify these warning signs is a vital first step toward protecting homeowners from further harm and ensuring that any foreclosure-related assistance comes from legitimate, transparent, and accountable sources.

Unrealistic Guarantees Are Often the First Warning Sign

One of the clearest indicators of foreclosure fraud is the promise of a guaranteed outcome. Any individual or company claiming they can stop a foreclosure no matter the circumstances should immediately raise concern. The foreclosure process is shaped by loan terms, payment history, court filings, lender actions, state laws, and procedural deadlines. Because every case is different, no legitimate professional can honestly guarantee a loan modification, foreclosure dismissal, mortgage reversal, or complete cancellation of debt without first reviewing the facts. Fraudsters often use absolute language because distressed homeowners are more likely to respond when they hear words such as “guaranteed approval,” “instant relief,” or “we will save your home.” These promises are designed to create emotional dependence before the homeowner has the chance to verify credentials or review the actual terms of service.

In many foreclosure fraud schemes, the guarantee is paired with urgency. A homeowner may be told that immediate action is required and that delay will automatically result in losing the property. While foreclosure deadlines are indeed serious, pressure tactics are often used to stop people from asking questions, consulting an attorney, or reading documents carefully. A trustworthy professional explains the situation clearly, discusses possible outcomes honestly, and never relies on fear-based promises to secure payment or signatures.

Upfront Fees Can Signal Serious Trouble

Another major red flag associated with foreclosure fraud is the demand for large upfront fees before any real service is performed. Homeowners in distress are often asked to pay for forensic audits, negotiation services, modification support, document review, or foreclosure rescue plans. While some legitimate services may involve structured fees, fraudulent operators often insist on payment first and provide little or nothing afterward. Once the money is collected, communication may become inconsistent, vague, or disappear altogether.

The danger grows when the homeowner believes that paying the fee means the problem is being handled. During that period, court dates may approach, lender notices may go unanswered, and valuable time may be lost. In this way, foreclosure fraud causes damage not only through financial loss but also through delay. A borrower may spend crucial weeks trusting the wrong party instead of pursuing valid legal or procedural options. Any company demanding high fees while avoiding clear written explanations of services, timelines, and limitations should be examined with caution.

Requests to Sign Documents without Review Should Never Be Ignored

A frequent tactic in foreclosure fraud involves pressuring homeowners to sign documents quickly, often without allowing enough time to read or understand what is being signed. Fraudsters may claim the paperwork is routine, say it is only for negotiation purposes, or insist that legal language is too complicated to explain. In reality, those documents may contain transfer clauses, power of attorney provisions, rental conversion terms, or waivers that significantly weaken the homeowner’s position.

This is especially dangerous because people facing foreclosure are often overwhelmed and may assume that signing paperwork is simply part of getting help. Yet in many foreclosure fraud cases, the documents are the mechanism through which control over the property changes hands. A homeowner might believe they are authorizing assistance while actually transferring an interest in the home or consenting to terms that are difficult to reverse. Legitimate professionals encourage review, provide explanations, and allow time for independent legal advice. Pressure to sign immediately is not a small concern; it is often a central sign that something is wrong.

False Claims of Government or Legal Affiliation Create Misplaced Trust

Many foreclosure fraud operations rely on appearance and language to seem official. They may use names that sound connected to federal housing programs, legal enforcement agencies, banks, or court-approved relief services. Some may include seals, logos, or formal-looking documents that create the impression of government authority or lender endorsement. Homeowners who are already frightened may assume the communication is authentic simply because it appears professional.

This type of deception is effective because it targets trust. People tend to respond differently when they believe the contact is tied to a government office, attorney, housing authority, or mortgage institution. In the context of foreclosure fraud, that false credibility can persuade borrowers to disclose personal information, pay fees, or follow instructions that put them at greater risk. Any unexpected communication claiming official authority should be independently verified through known contact channels rather than accepted at face value.

Instructions to Stop Communicating With the Lender Are Highly Suspicious

One of the most harmful patterns in foreclosure fraud is when a third party tells the homeowner to stop speaking directly with the lender, servicer, or attorney. Fraudsters often want to control all communication because it prevents the borrower from hearing accurate information about deadlines, loss mitigation options, reinstatement amounts, or case status. Once contact is cut off, the homeowner becomes dependent on whatever updates the third party chooses to provide, whether true or false.

This isolation benefits the scheme. By limiting direct communication, foreclosure fraud operators reduce the chance that the homeowner will discover missed filings, false promises, or nonexistent negotiations. A borrower may believe a modification is underway when in fact no paperwork was ever submitted. Keeping open communication with the lender does not solve every foreclosure problem, but being told to completely disconnect from the actual mortgage holder or servicer is a serious warning sign that should not be dismissed.

Title Transfer and Sale-Leaseback Offers Require Extreme Caution

Some of the most damaging forms of foreclosure fraud involve offers that appear creative or helpful on the surface. A fraudster may suggest transferring the title temporarily so the foreclosure can be avoided, or propose that the homeowner sell the property and remain in it as a renter until they can buy it back later. These arrangements are often presented as rescue strategies, but they can conceal a plan to strip equity and permanently remove ownership from the borrower.

In many cases, the promised buyback never becomes realistic. Rent terms may rise, repurchase conditions may be impossible to meet, and the former homeowner may find that their legal rights have weakened dramatically. This is why title-related proposals deserve close scrutiny. Within the broader pattern of foreclosure fraud, any strategy requiring immediate transfer of ownership should be reviewed very carefully with trusted legal guidance before a signature is ever provided.

Missing Documentation and Vague Explanations Often Reveal Deception

Fraud rarely thrives in transparency. Many foreclosure fraud schemes are marked by poor documentation, incomplete contracts, verbal promises, inconsistent timelines, and vague explanations about what services will actually be delivered. The fraudster may speak confidently but avoid specific answers when asked for proof, credentials, written commitments, or detailed scope of work. They may also resist providing copies of signed papers or fail to explain how fees are calculated.

This lack of clarity is not accidental. Ambiguity gives fraudulent actors room to change their story, deny earlier statements, and escape accountability. In foreclosure-related matters, where timing and documentation are critical, unclear records can create lasting harm. One of the strongest protections against foreclosure fraud is careful attention to paperwork, written communication, and verified details. When documents are missing, explanations are evasive, and promises remain unsupported, the warning signs are already present.

Conclusion

In conclusion, foreclosure fraud is a serious threat that can deepen the financial and emotional strain already faced by homeowners in distress. From unrealistic guarantees and upfront fee demands to rushed signatures, false affiliations, and suspicious title transfer offers, the warning signs of foreclosure fraud should never be ignored. These schemes are often designed to exploit urgency, confusion, and fear, making it essential for borrowers to slow down, verify every claim, and review every document with care before making decisions.

Understanding the common indicators of foreclosure fraud is one of the strongest ways to protect both property rights and legal options. When homeowners, attorneys, and support professionals recognize inconsistencies early, they are better positioned to prevent further damage, preserve important records, and respond strategically. Even small irregularities can point to much larger issues when examined closely.

Ultimately, awareness is the first line of defense against foreclosure fraud. Careful documentation, independent verification, and timely professional review can help uncover deceptive practices before they lead to irreversible consequences. By staying informed and alert, those facing foreclosure can reduce their risk, protect their interests, and make more confident decisions during one of the most challenging periods of the homeownership journey.

Turn Complex Mortgage Questions Into Stronger Legal Strategies

Unlock clarity, strengthen your case, and deliver greater value to your clients with the trusted support of Mortgage Audits Online. For over 4 years, we have helped our associates build stronger cases through detailed securitization reviews and professional forensic mortgage audits designed to uncover critical loan documentation issues, identify inconsistencies, and support case preparation with meaningful insight.

When clarity, documentation, and professional analysis matter most, the right forensic mortgage audit partner can help transform uncertainty into strategic advantage. Mortgage Audits Online works exclusively as a business-to-business provider, giving legal and industry professionals the focused support they need to approach complex mortgage matters with greater confidence, precision, and credibility.

Equip your cases with the depth of analysis they deserve. Partner with a team committed to helping you strengthen your files, support your arguments, and pursue better client outcomes through reliable mortgage audit services.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

Phone: 877-399-2995

Fax: 877-398-5288

“Disclaimer Note: This article is for educational & entertainment purposes

{kind=link}