A Practical Guide to Securitization and Foreclosure Defense for Legal Professionals

In today’s complex financial and legal landscape, Securitization and Foreclosure Defense has become an essential area of knowledge for attorneys, paralegals, and legal professionals who handle mortgage-related disputes. Over the past two decades, the rapid expansion of mortgage-backed securities and the global financial system has transformed the way residential and commercial loans are originated, sold, and enforced. As a result, understanding the legal and financial mechanics behind loan securitization is no longer optional—it is a critical skill for those seeking to effectively challenge questionable foreclosure actions and protect client rights.

At its core, Securitization and Foreclosure Defense involves examining the transfer and ownership of mortgage loans within the securitization process and determining whether the party attempting foreclosure has the legal authority to do so. Mortgage securitization typically involves bundling thousands of individual loans together and selling them to investors through complex trust structures. These loans are often transferred multiple times between originators, aggregators, trustees, and servicers. While this process was designed to create liquidity in the financial markets, it has also created layers of documentation, assignments, and servicing arrangements that can sometimes lead to errors, inconsistencies, or even violations of legal requirements.

For legal professionals, a strong understanding of Securitization and Foreclosure Defense provides the tools necessary to analyze loan documentation, securitization trust records, pooling and servicing agreements, and assignment chains. By carefully reviewing these elements, attorneys may uncover irregularities such as missing endorsements, improperly executed assignments, broken chains of title, or violations of trust closing dates. These findings can become powerful legal arguments when defending homeowners or challenging foreclosure actions in court.

Another critical component of Securitization and Foreclosure Defense is the forensic review of loan files and servicing records. Mortgage servicers often manage thousands of loans simultaneously, and errors in payment histories, escrow calculations, or default notices can occur. A thorough forensic audit may reveal misapplied payments, unauthorized fees, or inaccurate default calculations that could undermine the validity of a foreclosure claim. Legal professionals who understand how to interpret these financial records gain a strategic advantage when presenting evidence or negotiating settlements.

The legal framework surrounding Securitization and Foreclosure Defense is also shaped by evolving case law and regulatory developments. Courts across jurisdictions have increasingly scrutinized foreclosure filings to ensure that lenders and servicers can demonstrate clear ownership of the loan and proper standing to enforce it. Decisions in various courts have emphasized the importance of accurate documentation, proper assignments, and compliance with trust agreements. For attorneys practicing in foreclosure defense, staying informed about these legal precedents is essential for building persuasive arguments and protecting client interests.

Beyond courtroom litigation, Securitization and Foreclosure Defense also plays an important role in negotiation strategies. When legal professionals identify weaknesses in a lender’s documentation or securitization chain, those findings can create leverage in loan modification discussions, settlement negotiations, or mediation proceedings. Borrowers may benefit from improved settlement terms, reduced balances, or alternative resolution options when lenders recognize potential legal vulnerabilities in their foreclosure claims.

Furthermore, education and training in Securitization and Foreclosure Defense empowers legal professionals to approach mortgage litigation with confidence and precision. By combining legal analysis with financial investigation, attorneys can move beyond surface-level foreclosure defenses and develop deeper, evidence-based strategies. This multidisciplinary approach—blending contract law, property law, financial analysis, and litigation tactics—has become increasingly valuable in modern foreclosure cases.

This practical guide to Securitization and Foreclosure Defense is designed to help legal professionals navigate the complexities of mortgage securitization and apply that knowledge effectively in foreclosure-related matters. By understanding how loans are transferred, documented, and enforced within securitized structures, attorneys and legal teams can identify critical issues that may otherwise remain hidden within thousands of pages of loan and trust documentation.

Ultimately, mastering Securitization and Foreclosure Defense equips legal professionals with the analytical tools needed to evaluate foreclosure cases thoroughly, challenge improper claims, and advocate more effectively for their clients. As mortgage finance continues to evolve and securitization structures remain central to the housing market, professionals who develop expertise in this field will be better positioned to deliver informed, strategic, and impactful legal representation.

Understanding the Foundations of Securitization in Mortgage Lending

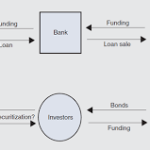

To effectively practice Securitization and Foreclosure Defense, legal professionals must first understand how mortgage securitization works and why it plays such a critical role in modern foreclosure litigation. Mortgage securitization is the financial process through which individual mortgage loans are pooled together and sold to investors as securities. These securities are typically structured as mortgage-backed securities (MBS) and are often placed into specialized trusts that issue investment certificates to investors.

The securitization process typically begins with a lender or originator who creates a mortgage loan with a borrower. Shortly after the loan is originated, it is often sold to an aggregator or sponsor that collects many similar loans into a large pool. These loans are then transferred into a securitization trust, which is administered by a trustee on behalf of investors. The trust issues securities to investors who receive payments derived from the borrowers’ mortgage payments.

For attorneys working in Securitization and Foreclosure Defense, this chain of transfers is critically important. Each step in the process requires documentation, endorsements, and assignments that demonstrate how the loan moved from the original lender into the securitization trust. If any step in this chain is missing or improperly documented, questions may arise regarding whether the party initiating foreclosure actually possesses the legal right to enforce the loan.

Understanding the structure of mortgage securitization allows legal professionals to examine the loan history more effectively. By analyzing trust documents, assignments, and transfer records, attorneys can identify potential inconsistencies or gaps that may become central to a foreclosure defense strategy.

The Role of Documentation in Securitization and Foreclosure Defense

Documentation forms the backbone of any Securitization and Foreclosure Defense strategy. Mortgage loans are governed by a series of critical documents, including the promissory note, mortgage or deed of trust, assignments, endorsements, and servicing agreements. These documents collectively establish ownership of the loan and define the rights of the parties involved.

In many foreclosure cases, the plaintiff must demonstrate that it has proper standing to enforce the loan. This means showing that the party bringing the foreclosure action is the legitimate holder of the note or otherwise authorized to enforce it. When loans have been securitized and transferred multiple times, proving this standing can become complicated.

Legal professionals often focus on reviewing the chain of assignments that document the transfer of the mortgage. If assignments appear to have been executed after the foreclosure filing, improperly notarized, or signed by unauthorized individuals, these issues may raise questions about the validity of the transfer. Within the framework of Securitization and Foreclosure Defense, identifying such documentation problems can be crucial in challenging the legitimacy of a foreclosure action.

Equally important is the review of the promissory note itself. Endorsements on the note indicate how ownership has changed over time. A missing endorsement, incomplete endorsement chain, or questionable allonge attachment may create legal arguments regarding the lender’s ability to enforce the note.

Pooling and Servicing Agreements and Their Legal Significance

Another critical component of Securitization and Foreclosure Defense involves analyzing the Pooling and Servicing Agreement (PSA). The PSA is the governing contract that outlines how loans are transferred into a securitization trust and how those loans must be administered by servicers and trustees.

Pooling and Servicing Agreements establish strict rules for how and when loans must be transferred into the trust. These agreements often include specific closing dates after which no additional loans may be added to the trust. If a mortgage loan appears to have been transferred into the trust after the closing date, it may raise questions regarding whether the transfer complied with the terms of the agreement.

Legal professionals practicing Securitization and Foreclosure Defense frequently examine PSAs to determine whether the transfers associated with a particular loan were executed according to the governing trust documents. Although courts may differ in how they interpret such issues, the PSA remains a critical source of information regarding the intended structure and timeline of securitization transactions.

PSAs also define the roles of servicers, trustees, and other parties responsible for managing the loans. These agreements outline how payments must be processed, how defaults are handled, and what procedures must be followed before initiating foreclosure. When servicers fail to comply with these requirements, it may provide additional arguments within a foreclosure defense strategy.

Forensic Loan Analysis in Foreclosure Litigation

Forensic loan analysis is another essential element of Securitization and Foreclosure Defense. This process involves a detailed examination of the borrower’s payment history, loan servicing records, escrow calculations, and fee assessments. Through forensic analysis, legal professionals can identify discrepancies that may affect the accuracy of the alleged loan balance or default status.

Mortgage servicing errors are not uncommon, particularly in large servicing portfolios that contain thousands of loans. Payments may be misapplied, late fees may be improperly assessed, or escrow accounts may be incorrectly calculated. A comprehensive forensic audit can uncover these issues and provide valuable evidence in foreclosure litigation.

In the context of Securitization and Foreclosure Defense, forensic reviews may also examine whether the servicer followed proper procedures when declaring a default. Many mortgage contracts require lenders or servicers to provide specific notices to borrowers before accelerating the loan or initiating foreclosure. If these notices were not properly issued or documented, it may create a procedural defense.

Legal professionals who understand how to interpret servicing records and financial statements gain a strategic advantage when preparing for litigation. By identifying inconsistencies in the loan records, attorneys can challenge the lender’s claims and strengthen their client’s defense.

Litigation Strategies in Securitization and Foreclosure Defense

Effective litigation strategies are at the heart of Securitization and Foreclosure Defense. Attorneys must combine legal knowledge, financial analysis, and procedural awareness to build persuasive arguments in foreclosure cases. This process often begins with a detailed review of all loan documents and securitization records.

One common strategy involves challenging the plaintiff’s standing to foreclose. If the party initiating foreclosure cannot demonstrate clear ownership of the loan or the authority to enforce it, the court may question the legitimacy of the claim. Establishing standing requires proper documentation of every transfer in the loan’s history.

Another strategy involves identifying violations of consumer protection laws, mortgage servicing regulations, or contractual requirements within the loan agreement. Federal and state laws often impose strict requirements on lenders and servicers regarding disclosures, default notices, and loss mitigation procedures. Violations of these requirements may become important elements of a defense strategy.

Within the broader field of Securitization and Foreclosure Defense, discovery also plays a critical role. Attorneys may request documents related to the securitization trust, servicing records, or internal communications that clarify how the loan was handled. These documents can provide valuable insight into whether the foreclosure process was conducted properly.

The Importance of Expertise in Modern Foreclosure Cases

As mortgage finance has evolved, foreclosure litigation has become increasingly complex. The intersection of securitization structures, servicing practices, and regulatory frameworks requires legal professionals to develop specialized expertise. For this reason, Securitization and Foreclosure Defense has emerged as a distinct and highly specialized area within mortgage litigation.

Attorneys who invest time in understanding securitization structures and forensic loan analysis are better positioned to evaluate foreclosure cases comprehensively. This expertise enables legal professionals to move beyond surface-level defenses and explore deeper issues related to loan ownership, documentation accuracy, and compliance with contractual obligations.

In many cases, the strength of a foreclosure defense strategy depends on the ability to analyze large volumes of financial and legal documents. By applying the principles of Securitization and Foreclosure Defense, attorneys can identify key issues that may significantly impact the outcome of a case.

As foreclosure litigation continues to evolve alongside changes in the mortgage industry, legal professionals who develop strong knowledge in Securitization and Foreclosure Defense will remain well equipped to navigate complex cases, advocate effectively for their clients, and ensure that foreclosure proceedings are conducted in accordance with the law.

Conclusion

In today’s mortgage litigation environment, a clear understanding of Securitization and Foreclosure Defense has become an essential skill for attorneys, paralegals, and legal professionals working with foreclosure-related cases. The securitization of mortgage loans introduced complex financial structures that significantly changed how loans are originated, transferred, and enforced. As a result, foreclosure cases now require deeper legal analysis and careful examination of loan documentation, transfer histories, and servicing practices.

By mastering the principles of Securitization and Foreclosure Defense, legal professionals gain the ability to identify irregularities within the securitization chain, evaluate whether the foreclosing party has proper legal standing, and assess whether mortgage servicers followed the required procedures before initiating foreclosure. Careful review of key documents such as promissory notes, assignments, and pooling and servicing agreements can often reveal inconsistencies that may become central elements in a strong defense strategy.

Furthermore, Securitization and Foreclosure Defense empowers legal teams to approach foreclosure litigation with greater precision and confidence. Through detailed forensic loan analysis and strategic legal arguments, professionals can challenge improper claims and ensure that foreclosure proceedings comply with applicable laws and contractual obligations.

Ultimately, expertise in Securitization and Foreclosure Defense enables legal professionals to better protect their clients’ interests, strengthen case strategies, and navigate the increasingly complex landscape of modern mortgage litigation.

Unlock Clarity. Strengthen Your Case. Transform Your Client Outcomes

When legal strategy depends on documentation, precision, and credible analysis, having the right audit partner can make a measurable difference. For more than four years, Mortgage Audits Online has helped legal professionals and industry associates build stronger, more defensible cases through detailed securitization analysis and forensic mortgage audits.

As an exclusively business-to-business service provider, Mortgage Audits Online works directly with attorneys, law firms, and industry professionals who require audit reports that are structured, documented, and suitable for real-world legal use. Their approach focuses on deep research, accurate documentation, and clear reporting that helps professionals evaluate mortgage transactions, identify inconsistencies, and strengthen case strategies.

Every case presents its own challenges. Mortgage loans often pass through multiple transfers, assignments, and servicing arrangements—creating complex documentation trails that must be carefully examined. Mortgage Audits Online specializes in uncovering these details through forensic mortgage audits and securitization research designed to highlight critical issues such as chain-of-title inconsistencies, documentation gaps, and servicing irregularities. These insights can provide legal teams with the clarity needed to assess risk, challenge questionable claims, and move forward with confidence.

Professional audit reports from Mortgage Audits Online are designed with practical usability in mind. Findings are structured clearly, supported by documentation, and presented in a way that allows legal professionals to quickly understand key issues and integrate them into broader litigation or negotiation strategies. In complex mortgage cases, this level of clarity can turn uncertainty into strategic advantage.

If your firm is seeking reliable analysis, evidence-based reporting, and professional support in mortgage-related matters, Mortgage Audits Online offers the expertise and experience needed to strengthen your case preparation process.

Equip your cases with the depth of analysis they deserve. Connect with Mortgage Audits Online today and gain the clarity that supports stronger legal outcomes.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: : https://www.mortgageauditsonline.com/

“Disclaimer Note: This article is for educational & entertainment purposes

{kind=link}