Home Loan Securitization Fraud and the Critical Documents That Demand Review

In today’s complex mortgage environment, borrowers, attorneys, forensic auditors, and housing advocates are increasingly examining the hidden layers behind loan origination, transfer, servicing, and foreclosure activity. One of the most important issues drawing attention is home loan securitization fraud, a subject that often remains poorly understood until a dispute, default, servicing conflict, or foreclosure action forces a closer look. What appears on the surface to be a simple mortgage transaction may actually involve multiple parties, repeated transfers, questionable endorsements, inconsistent assignments, servicing changes, and documentation that does not always align with the legal history of the loan. This is why a careful review of the mortgage file is no longer optional in many contested cases. It is essential.

At its core, home loan securitization fraud refers to irregularities, misrepresentations, or document defects connected to the bundling of mortgage loans into trusts or mortgage-backed securities. When a loan is securitized, it may pass through several entities, including originators, sponsors, depositors, trustees, custodians, and servicers. In a properly documented process, every transfer should be supported by clear, timely, and legally consistent records. However, in many disputed cases, the paper trail contains gaps, contradictions, late assignments, missing endorsements, fabricated allonges, or signatures that raise serious questions about authenticity and authority. These issues are not merely technical concerns. They can affect ownership claims, enforcement rights, payment application, loss mitigation decisions, and the legal standing of parties attempting to collect or foreclose.

The growing concern surrounding home loan securitization fraud is tied directly to the importance of documentary evidence. Mortgage cases often turn on what can be proven through records, not what is casually asserted by a servicer or plaintiff. A borrower may be told that the current claimant owns the loan, yet the chain of title may be incomplete. A foreclosure complaint may rely on documents executed years after trust closing dates. An assignment may appear valid at first glance but conflict with pooling and servicing provisions, recorded timelines, or the authority of the signatory. In many situations, the truth lies buried in the details of the note, mortgage, assignments, allonges, payment history, servicing records, SEC filings, trust documents, and correspondence. Without reviewing these records together, it is easy to miss the inconsistencies that could significantly change the direction of a case.

This is where the document review process becomes critical. Identifying home loan securitization fraud requires more than scanning a few pages for errors. It demands a structured, evidence-based examination of the key mortgage and securitization records that define the loan’s legal and financial journey. Every date, endorsement, signature block, recording entry, transfer history, and trust reference matters. Even a minor discrepancy can signal deeper problems in ownership, compliance, or enforcement. For attorneys and legal professionals, these records can support motions, defenses, discovery strategies, and challenges to standing. For borrowers, they can reveal whether representations made about the loan are accurate. For forensic specialists, they provide the basis for identifying patterns of document manipulation, securitization defects, and servicing misconduct.

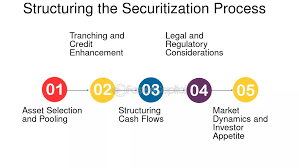

Understanding home loan securitization fraud also means recognizing that the issue is not limited to one document or one event. It often emerges through a pattern of irregularities spread across the entire file. That is why the most effective reviews focus on the critical documents that demand scrutiny from origination through securitization and, if applicable, through foreclosure. A disciplined investigation can uncover whether the records support a lawful transfer and enforceable claim, or whether they expose defects that deserve immediate legal and forensic attention.

Why Document Review Is Central to Uncovering Home Loan Securitization Fraud

A mortgage dispute cannot be evaluated properly without examining the documents that support the life of the loan. In cases involving home loan securitization fraud, the most damaging issues are often hidden behind paperwork that appears routine until it is carefully compared line by line. A loan may have been originated by one entity, sold to another, pooled into a trust, serviced by multiple companies, and later enforced by a party claiming rights through assignments and endorsements that deserve close scrutiny. When the documents do not align with that timeline, serious questions arise about ownership, authority, and legal standing. This is why document review is not simply an administrative exercise. It is one of the strongest ways to detect whether the records tell a coherent and lawful story or reveal indicators of home loan securitization fraud.

The Promissory Note Must Be Examined With Precision

The promissory note is one of the most important documents in any mortgage file because it represents the borrower’s promise to repay the debt and often becomes central in enforcement actions. In matters involving home loan securitization fraud, the note should be reviewed for endorsements, undated stamps, missing signatures, suspicious allonges, and alterations that appear inconsistent with the rest of the record. A note that is presented as properly transferred may still raise concerns if endorsements appear out of sequence or if an allonge is introduced only after litigation begins. These details matter because they can affect whether the party seeking enforcement actually possesses the rights it claims.

Reviewing the note also helps determine whether the transfer history matches the loan’s alleged securitization path. If the note reflects a pattern that conflicts with assignments, trust documentation, or servicing claims, it may signal deeper defects in the securitization chain. In many investigations, the note becomes a key piece of evidence because it often exposes whether documentation was maintained in the ordinary course of business or reconstructed later to support a contested claim.

The Mortgage or Deed of Trust Can Reveal Transfer Problems

The mortgage or deed of trust secures the loan with the property and must be reviewed together with the note, not in isolation. In cases of home loan securitization fraud, this document may contain clues about the original lender, nominee relationships, recording history, legal descriptions, and the scope of authority granted to entities involved in later transfers. A disconnect between the mortgage and the note can become highly significant, especially when recorded assignments appear years after the loan was allegedly placed into a securitized trust.

The language in the mortgage document may also help reveal whether later claims of ownership are consistent with the original transaction. If a foreclosing party relies on an assignment that conflicts with earlier records or if the transfer history appears incomplete, the mortgage file may expose the gap. These inconsistencies are often important because home loan securitization fraud can involve attempts to repair or recreate a chain of title after defects have already occurred.

Assignments of Mortgage Often Carry the Most Visible Red Flags

Assignments of mortgage are frequently among the most scrutinized records in any securitization dispute. They can provide a timeline of supposed transfers, but they can also reveal serious concerns when examined carefully. In allegations of home loan securitization fraud, assignments may be executed long after the trust closing date, signed by individuals whose authority is unclear, notarized under questionable circumstances, or recorded in a sequence that does not make commercial or legal sense. A late assignment may not automatically prove wrongdoing, but it can raise legitimate questions that deserve further investigation.

One of the most common problems is the appearance of assignments created only when foreclosure becomes imminent. When a document suddenly emerges to bridge a missing link in ownership, investigators often ask whether the record reflects a true historical transfer or a later attempt to correct an evidentiary problem. In many cases, the assignment history becomes the place where home loan securitization fraud is most visible because it provides a concrete record that can be matched against trust rules, servicing claims, and court filings.

Allonges and Endorsements Demand Close Authentication Review

Allonges are often presented as attachments to the note containing endorsements that supposedly transferred enforcement rights. Because of their importance, they deserve an especially careful review. In matters involving home loan securitization fraud, allonges may raise concerns when they are undated, unattached, inconsistently formatted, or introduced without a clear custodial history. A valid endorsement process should be logical, consistent, and supported by the surrounding records. When an allonge appears out of nowhere or contains irregularities in placement, sequencing, or execution, it may suggest that the transfer record is less reliable than claimed.

The authenticity of endorsements also matters because a party may rely on them to argue possession and standing. If the endorsements are incomplete, questionable, or inconsistent with securitization timelines, the strength of that claim may weaken considerably. That is why home loan securitization fraud investigations often focus intensely on whether allonges and endorsements were created in the ordinary course of transfer or produced later to fill documentary gaps.

Pooling and Servicing Agreements Can Expose Conflicts in the Transfer Timeline

The pooling and servicing agreement, often called the PSA, is one of the most important securitization records because it defines how loans are supposed to move into the trust and how the trust is administered. In many home loan securitization fraud reviews, the PSA becomes essential because it can reveal whether the alleged transfer of the mortgage loan actually complied with the trust’s governing terms. If the trust required delivery of endorsed notes and assignments by a specific closing date, but the loan documents show transfers occurring much later, that inconsistency may carry major significance.

The PSA can also identify the parties expected to participate in the securitization chain, including the depositor, trustee, master servicer, and document custodian. When the loan file reflects a transfer path that does not match those roles, the discrepancy may support concerns about home loan securitization fraud. A careful comparison between the PSA and the recorded mortgage documents can therefore reveal whether the securitization story is supported by evidence or undermined by contradictions.

Payment Histories and Servicing Records Often Tell a Different Story

While transfer documents receive significant attention, payment histories and servicing records are equally important. In cases involving home loan securitization fraud, these records may reveal unexplained fees, inconsistent balances, misapplied payments, sudden servicing changes, or account histories that conflict with representations made in litigation or collection efforts. Servicing records can show whether the entity demanding payment actually maintained the account with accuracy and authority.

These documents can also expose whether the loan was treated as part of a securitized pool while other records fail to establish a lawful chain of transfer. In some situations, payment ledgers and servicing notes reveal activity inconsistent with the official ownership narrative. That is why the investigation of home loan securitization fraud should never stop with recorded land documents alone. The internal servicing file may reveal operational facts that either support or undermine the legal claims being made.

SEC Filings and Trust Documents Add Critical Context

Securitized loans are often tied to trusts that generate filings, prospectuses, schedules, and investor-related disclosures. These documents can provide valuable context when evaluating home loan securitization fraud because they help establish whether the loan was actually listed, transferred, or described as part of a specific trust. If a party claims that a mortgage belongs to a securitized trust, supporting trust records should help confirm that claim. When such confirmation is missing or inconsistent, the absence itself can be meaningful.

Reviewing trust-related documents also helps investigators test the credibility of assertions made by servicers or foreclosure plaintiffs. A case may rely on broad claims of securitized ownership, but the trust records may fail to reflect the loan in a way that matches the litigation narrative. In these circumstances, home loan securitization fraud becomes a document-driven inquiry in which each record must be measured against the others to determine whether the full picture is legally and factually consistent.

Conclusion

In conclusion, home loan securitization fraud is a serious issue that cannot be understood by looking at one document alone. It is often uncovered only through a careful review of the full mortgage file, including the promissory note, mortgage or deed of trust, assignments, allonges, pooling and servicing agreements, payment histories, servicing records, and trust-related disclosures. When these records are compared closely, they may reveal gaps in the chain of title, questionable endorsements, late transfers, conflicting dates, or inconsistencies in ownership claims that deserve immediate attention.

The importance of identifying home loan securitization fraud lies in the fact that documentation errors and irregularities can directly affect enforcement rights, foreclosure standing, and the overall legal strength of a claim. What may first appear to be a routine mortgage transaction can, upon deeper examination, expose a pattern of flawed transfers or unreliable records. That is why borrowers, attorneys, and forensic professionals must approach these cases with precision and diligence.

A thorough document review does more than uncover possible home loan securitization fraud. It creates clarity, strengthens legal strategy, and helps ensure that any claim involving the loan is supported by credible and consistent evidence rather than unsupported assertions.

A through documentation, and professional insight matter most, working with the right forensic mortgage audit partner can transform uncertainty into strategic advantage. Connect with Mortgage Audits Online today and equip your cases with the depth of analysis and credibility they deserve.

Unlock Clarity. Strengthen Your Case. Transform Your Client Outcomes

When mortgage disputes demand precision, documentation, and credible analysis, having the right forensic audit partner can make all the difference. For over four years, Mortgage Audits Online has helped associates build stronger, better-supported cases through detailed securitization and forensic audits designed to uncover critical loan and document issues with confidence.

As an exclusively business-to-business provider, Mortgage Audits Online is committed to supporting professionals who need reliable insight, strategic clarity, and evidence-driven reporting. Our work is designed to help you identify key irregularities, strengthen case preparation, and move forward with greater authority in complex mortgage-related matters.

When clarity, documentation, and professional insight matter most, working with the right forensic mortgage audit partner can transform uncertainty into strategic advantage. Connect with Mortgage Audits Online today and equip your cases with the depth of analysis and credibility they deserve.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

Phone: 877-399-2995

Fax: 877-398-5288

Visit: www.mortgageauditsonline.com

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}