How Securitization and Foreclosure Defense Strategies Can Challenge Mortgage Claims

In recent decades, the structure of the mortgage industry has changed dramatically. Home loans that were once held by the original lender are now commonly bundled, sold, and traded on global financial markets through a process known as securitization. While this financial mechanism has increased liquidity and investment opportunities in the housing market, it has also introduced layers of complexity that often obscure the true ownership and enforceability of mortgage loans. As a result, Securitization and Foreclosure Defense strategies have emerged as powerful tools for examining and challenging mortgage claims, especially in cases where documentation, ownership, or legal standing is questionable.

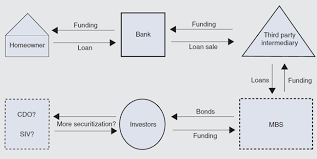

At its core, securitization involves pooling thousands of mortgage loans into financial instruments known as mortgage-backed securities (MBS), which are then sold to investors. These securities generate income based on homeowners’ monthly mortgage payments. However, the process requires multiple transfers of the loan through various entities, including originators, sponsors, depositors, trustees, and servicers. Each transfer must follow strict legal and contractual guidelines to ensure the loan is properly conveyed into the securitized trust. When these transfers are mishandled, improperly documented, or executed outside the required timelines, it can create serious legal issues regarding who actually owns the mortgage and who has the authority to enforce it.

This is where Securitization and Foreclosure Defense becomes critically important. Borrowers and legal professionals increasingly rely on detailed forensic analysis of loan documents, securitization filings, and servicing records to uncover discrepancies in the mortgage chain of title. If a lender or servicer cannot demonstrate clear ownership or lawful assignment of the mortgage, the foundation of the foreclosure claim may be challenged. Courts in many jurisdictions require that the party seeking foreclosure prove that it has proper standing, meaning it must show that it is the legitimate holder of the note and mortgage.

One of the most common issues uncovered through Securitization and Foreclosure Defense is the improper assignment of mortgage documents. In many securitized loans, assignments were created years after the trust closing date, which may violate the terms of the trust agreements governing mortgage-backed securities. When these assignments appear to be backdated or executed by entities without proper authority, they raise legitimate legal questions about whether the loan was ever validly transferred into the trust. If the transfer did not occur as required, the entity attempting foreclosure may lack the legal standing to enforce the debt.

Another significant area of scrutiny involves the role of mortgage servicers. Servicers are responsible for collecting payments, managing accounts, and initiating foreclosure actions when borrowers default. However, servicers do not necessarily own the mortgage loan. In some cases, foreclosure proceedings are initiated by servicers acting on behalf of investors without sufficient documentation proving the investors’ rights. Through Securitization and Foreclosure Defense, attorneys and analysts can examine servicing agreements, payment histories, and investor reports to determine whether the servicer has the authority to bring a foreclosure action.

In addition to ownership disputes, securitization analysis can reveal broader procedural violations. Missing endorsements on promissory notes, inconsistent loan records, robo-signed documents, and gaps in the chain of title are all issues that can undermine the legitimacy of a foreclosure claim. By conducting a thorough investigation of these records, Securitization and Foreclosure Defense strategies help identify weaknesses in the lender’s case and provide borrowers with opportunities to challenge improper foreclosure actions.

The growing reliance on forensic loan audits and securitization analysis reflects a broader shift in foreclosure litigation. Rather than focusing solely on payment default, legal defenses increasingly examine whether the party enforcing the mortgage has complied with the complex financial and legal structures underlying securitized loans. When inconsistencies or violations are uncovered, they can become powerful arguments in court, negotiations, or loan modification discussions.

Ultimately, Securitization and Foreclosure Defense is not simply about delaying foreclosure proceedings; it is about ensuring that mortgage claims are supported by accurate documentation, lawful transfers, and proper legal standing. By shining a light on the intricate processes behind mortgage securitization, these strategies promote accountability and transparency in an industry where the true ownership of loans is often difficult to trace.

The Structure of Mortgage Securitization and Its Legal Implications

Mortgage securitization fundamentally changed the way residential loans are originated, transferred, and enforced. Instead of a lender holding a mortgage for the life of the loan, financial institutions began packaging thousands of mortgages together and selling them as investment securities. While this structure created a massive secondary mortgage market, it also introduced complex chains of ownership that often complicate foreclosure proceedings. Because of this complexity, Securitization and Foreclosure Defense has become an essential strategy for examining whether a foreclosure action is legally valid.

The securitization process usually begins with a lender originating a mortgage loan to a borrower. The loan is then sold to a sponsor or aggregator, which pools large numbers of loans together. These loans are subsequently transferred into a securitized trust that issues mortgage-backed securities to investors. Each transfer is supposed to be documented through assignments and endorsements that establish a clear chain of ownership. However, in many cases, these transfers were rushed, poorly documented, or executed outside the time frames required by the governing trust agreements.

When foreclosure actions occur years later, the entity attempting to enforce the loan must prove it has legal standing. This means it must demonstrate that the mortgage and promissory note were properly transferred into its control. Securitization and Foreclosure Defense focuses on reviewing the documentation behind these transfers to determine whether the chain of title is legally intact. If the chain of transfers contains gaps, inconsistencies, or unauthorized assignments, the foreclosure claim may be subject to serious legal challenges.

Chain of Title Issues and Their Impact on Foreclosure Cases

A central component of Securitization and Foreclosure Defense involves analyzing the chain of title associated with a mortgage loan. The chain of title represents the chronological record of ownership and assignments from the original lender to the current party attempting to enforce the debt. In a properly documented loan, every transfer should be clearly recorded, dated, and authorized.

However, during the height of mortgage securitization, many institutions relied on automated systems and bulk transfers rather than individually recorded assignments. This often resulted in incomplete or delayed documentation. In foreclosure proceedings, these documentation gaps can raise questions about whether the foreclosing party actually possesses the legal authority to enforce the loan.

For example, if an assignment of mortgage appears years after the securitized trust’s closing date, it may violate the trust’s governing agreements. Many securitized trusts operate under strict rules that require all loans to be transferred into the trust within a specified time frame. If a loan was not transferred according to these requirements, it may legally remain outside the trust. Through Securitization and Foreclosure Defense, attorneys and forensic analysts review trust documents, assignments, and securitization filings to determine whether such violations occurred.

When these irregularities are identified, they can undermine the foreclosure claim by challenging the standing of the foreclosing entity. Courts in many jurisdictions require clear proof of ownership before granting foreclosure relief. If the party bringing the foreclosure cannot demonstrate a valid chain of title, the case may be dismissed or significantly delayed.

The Role of Forensic Loan Audits in Mortgage Litigation

Forensic loan audits have become a critical investigative tool in Securitization and Foreclosure Defense. These audits involve a detailed review of mortgage documents, payment histories, securitization records, and servicing agreements. The goal is to identify inconsistencies, procedural violations, and documentation defects that may weaken the lender’s case.

During a forensic audit, analysts examine whether the promissory note contains proper endorsements and whether the mortgage assignments align with the securitization timeline. They also review payment records to ensure that loan balances, fees, and interest charges were calculated correctly. In some cases, auditors discover discrepancies in loan servicing practices, such as unexplained fees or accounting errors that affect the borrower’s payment history.

Another key aspect of these audits is the analysis of securitization databases and investor reports. These records may reveal whether the loan was sold into a mortgage-backed security and whether the transfer complied with the trust’s governing documents. When discrepancies are discovered, they can form the basis of legal arguments used in Securitization and Foreclosure Defense strategies.

For attorneys representing homeowners, forensic audit reports can provide valuable evidence that supports motions to dismiss, discovery requests, or settlement negotiations. Even when a foreclosure ultimately proceeds, identifying documentation defects can sometimes lead to more favorable outcomes for borrowers, such as loan modifications or negotiated resolutions.

Legal Standing and the Burden of Proof in Foreclosure Litigation

Legal standing is one of the most critical issues examined in Securitization and Foreclosure Defense cases. Standing refers to the legal right of a party to bring a lawsuit or enforce a financial obligation. In foreclosure proceedings, the plaintiff must demonstrate that it is either the holder of the promissory note or an authorized agent acting on behalf of the holder.

Because securitized loans often pass through multiple entities before reaching investors, establishing standing can be challenging. Servicers frequently initiate foreclosure actions on behalf of investors, but they must still demonstrate that the investors possess the legal rights associated with the loan. Without proper documentation, this authority may be questioned.

Through Securitization and Foreclosure Defense, legal professionals analyze whether the foreclosing party has provided sufficient evidence of its standing. This includes examining the endorsements on the promissory note, verifying the timing of mortgage assignments, and reviewing servicing agreements that authorize the servicer to act on behalf of investors.

If a foreclosure plaintiff cannot prove that it holds the note or has lawful authority to enforce it, the court may determine that the plaintiff lacks standing. In such cases, the foreclosure action may be dismissed until proper documentation is provided.

Documentation Irregularities and Procedural Violations

Another important area addressed by Securitization and Foreclosure Defense involves the identification of documentation irregularities. During the mortgage crisis, many financial institutions relied on mass document processing to handle large volumes of foreclosures. This practice led to widespread concerns about robo-signed documents, missing endorsements, and improperly executed assignments.

Robo-signing refers to the practice of signing large numbers of legal documents without verifying their accuracy. In foreclosure cases, this can result in affidavits and assignments that contain incorrect information or lack proper authorization. Courts have increasingly scrutinized these practices, and evidence of robo-signing can raise questions about the reliability of the documents submitted in support of foreclosure claims.

Missing endorsements on promissory notes can also create legal complications. A promissory note must typically be endorsed to each successive owner in order to establish a valid chain of possession. If the endorsements are incomplete or inconsistent with the recorded assignments, it may cast doubt on whether the foreclosing party is the legitimate holder of the note.

By investigating these documentation issues, Securitization and Foreclosure Defense strategies help reveal weaknesses in the lender’s case. Identifying such irregularities may support legal defenses that challenge the enforceability of the mortgage claim.

The Growing Importance of Analytical Mortgage Defense Strategies

As mortgage transactions continue to evolve, the importance of thorough loan analysis and legal review has grown significantly. The complexity of securitized loans means that foreclosure actions often involve far more than a simple claim of payment default. Questions about ownership, documentation, and compliance with securitization agreements frequently play a central role in foreclosure litigation.

Because of these complexities, Securitization and Foreclosure Defense has become an increasingly sophisticated field that combines legal analysis, financial investigation, and forensic auditing. Attorneys, analysts, and consultants work together to examine loan histories, securitization structures, and servicing records to determine whether foreclosure claims are supported by valid documentation.

For borrowers and legal professionals alike, understanding these strategies can provide valuable insight into the mechanics of modern mortgage enforcement. By carefully reviewing the documentation and financial structures behind mortgage loans, Securitization and Foreclosure Defense strategies help ensure that foreclosure actions are based on legitimate legal authority and accurate financial records.

Conclusion

The modern mortgage system is far more complex than traditional lending structures, largely due to the widespread use of securitization. While securitization created opportunities for investment and expanded the availability of mortgage credit, it also introduced intricate chains of ownership and documentation that can complicate foreclosure proceedings. As a result, Securitization and Foreclosure Defense has become an important analytical approach for examining whether mortgage claims are supported by valid legal authority and proper documentation.

By carefully reviewing loan transfers, securitization trust agreements, and servicing records, Securitization and Foreclosure Defense strategies help uncover discrepancies that may affect the enforceability of a mortgage. Issues such as incomplete chains of title, questionable assignments, missing endorsements, and procedural violations can raise serious concerns about whether the party seeking foreclosure actually has standing to enforce the loan. Through forensic loan audits and detailed document analysis, legal professionals can identify these weaknesses and use them to challenge improper or unsupported foreclosure actions.

Ultimately, Securitization and Foreclosure Defense promotes accountability within the mortgage servicing and lending system. By ensuring that foreclosure claims are backed by accurate records and lawful ownership, these strategies help uphold the integrity of the legal process while providing borrowers and attorneys with the tools needed to evaluate and challenge complex mortgage enforcement actions.

Strengthen Your Case with Proven Forensic Insight

Unlock Clarity. Strengthen Your Case. Transform Your Client Outcomes

In complex mortgage litigation and foreclosure defense matters, success often depends on the strength of your documentation, the clarity of your analysis, and the credibility of the evidence you present. When attorneys, auditors, and legal professionals require dependable insights into mortgage securitization, partnering with the right forensic audit provider can make a meaningful difference.

For more than four years, Mortgage Audits Online has been supporting legal and financial professionals with detailed securitization and forensic mortgage audits designed to help build stronger, evidence-based cases. As an exclusively business-to-business service provider, our mission is focused on empowering professionals with precise, well-structured reports that reveal critical loan details, identify documentation irregularities, and support informed legal strategies.

Our experienced analysts combine deep industry knowledge with comprehensive research methods to deliver clear and actionable findings. Each report is carefully prepared to help uncover securitization pathways, chain-of-title issues, servicing discrepancies, and other documentation concerns that may influence litigation or negotiation strategies. The result is a professional audit package that provides both clarity and strategic value when preparing foreclosure defense or mortgage litigation cases.

Professionals across the legal and financial sectors rely on Mortgage Audits Online for reports that are structured, credible, and designed to support real-world case preparation. Whether you are evaluating mortgage ownership, examining securitization transfers, or preparing documentation for court proceedings, our audits help transform complex loan histories into understandable, evidence-driven analysis.

When accuracy, professional insight, and timely delivery matter most, working with a trusted forensic audit partner can turn uncertainty into a strategic advantage. Equip your cases with the depth of analysis and credibility they deserve by partnering with a team dedicated to supporting your professional success.

Mortgage Audits Online

📍 100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

“Disclaimer Note: This article is for educational & entertainment purposes

{kind=link}