Home Loan Securitization Fraud and the Mortgage Crisis: Lessons Borrowers Must Learn

The global housing boom of the early 2000s promised prosperity, stability, and the dream of homeownership for millions of families. Easy credit, rising property values, and aggressive lending practices encouraged borrowers to take out mortgages that often seemed manageable at the time. However, beneath this wave of optimism lay a complex financial mechanism that many borrowers did not fully understand. At the heart of this system was home loan securitization fraud, a practice that became increasingly controversial during the financial turmoil that followed the housing market collapse.

To understand why home loan securitization fraud became such a critical issue, it is essential to first look at how modern mortgage finance evolved. Traditionally, banks originated loans and kept them on their books, collecting payments over time. But as the mortgage market expanded, financial institutions began bundling thousands of home loans together and selling them to investors as mortgage-backed securities. This process, known as securitization, allowed lenders to quickly recover capital and issue even more loans. While securitization itself was not inherently illegal, the lack of transparency and oversight created opportunities for manipulation, misrepresentation, and questionable documentation practices.

During the years leading up to the mortgage crisis, lenders, investment banks, and financial intermediaries rushed to produce large volumes of mortgage-backed securities. In this environment, home loan securitization fraud began to emerge in several forms. Some institutions failed to properly transfer mortgage notes into securitized trusts, while others misrepresented the quality of loans being sold to investors. In many cases, paperwork errors, robo-signing practices, and missing documentation created legal uncertainties about who actually owned the loans. These issues later surfaced in foreclosure proceedings, leaving borrowers confused and courts overwhelmed with disputes over loan ownership.

For many homeowners, the discovery of home loan securitization fraud came too late—often when they were already facing foreclosure. Borrowers who attempted to challenge foreclosure actions sometimes found discrepancies in loan documentation, chain-of-title records, or securitization timelines. These irregularities raised serious questions about whether financial institutions had followed proper legal procedures when transferring mortgages into investment trusts. In some cases, courts identified evidence of flawed processes, highlighting systemic weaknesses in the mortgage securitization system.

The mortgage crisis of 2007–2008 exposed how deeply these practices were embedded within the global financial system. As housing prices fell and borrowers began defaulting on loans, the complex network of securitized mortgages started to unravel. Investors discovered that many mortgage-backed securities were backed by risky or poorly documented loans. At the same time, allegations of home loan securitization fraud became a focal point of public debate, regulatory investigations, and legal challenges. Governments and financial regulators were forced to examine how such practices had contributed to the collapse of confidence in the mortgage market.

Another critical lesson from the crisis is the importance of transparency in financial transactions. Borrowers often had little knowledge about what happened to their mortgage after closing. Many were unaware that their loan could be sold, transferred, or securitized multiple times within a short period. This lack of clarity made it difficult for homeowners to understand their rights or identify potential irregularities. As awareness of home loan securitization fraud grew, consumer advocates and legal experts began encouraging borrowers to carefully review loan documents, assignment records, and securitization details.

Today, the legacy of the mortgage crisis continues to shape discussions about financial regulation, consumer protection, and responsible lending practices. While regulatory reforms have been introduced to strengthen oversight of the mortgage industry, concerns about documentation integrity and securitization transparency still exist. The lessons learned from home loan securitization fraud serve as a powerful reminder that borrowers must remain informed, vigilant, and proactive when dealing with mortgage agreements.

Ultimately, understanding the mechanics and risks associated with home loan securitization fraud is not just a legal or financial issue—it is a matter of protecting homeowners from potential abuses within a complex financial system. By learning from the mistakes that contributed to the mortgage crisis, borrowers can better safeguard their interests, demand transparency from lenders, and make more informed decisions about one of the most significant financial commitments of their lives.

Understanding the Structure of Mortgage Securitization

To fully grasp the risks associated with home loan securitization fraud, borrowers must first understand how the securitization process works. Mortgage securitization is a financial mechanism through which lenders bundle large numbers of home loans together and convert them into tradable securities that can be sold to investors. These securities, commonly known as mortgage-backed securities (MBS), allow financial institutions to move mortgage debt off their balance sheets and generate liquidity for further lending.

The process usually begins with the origination of a mortgage loan by a lender. Instead of holding the loan until it is paid off, the lender sells the loan to a financial intermediary, often an investment bank. That intermediary then pools thousands of similar loans and transfers them into a trust. Investors purchase securities backed by the expected payments from those loans. Ideally, each step follows a strict legal framework that ensures the proper transfer of loan ownership and documentation.

However, during the rapid expansion of the housing market in the early 2000s, the demand for mortgage-backed securities surged. Financial institutions were under immense pressure to create and sell these products quickly. In this high-volume environment, oversight weakened and documentation procedures were sometimes bypassed or improperly handled. This environment allowed home loan securitization fraud to take root, as errors and manipulations in the securitization chain became more common.

For borrowers, the complexity of this system often meant that their mortgage could change hands multiple times without their knowledge. The loan they originally signed with one lender could later be owned by a trust, serviced by a different company, and managed by yet another financial institution. This fragmentation made it difficult for homeowners to determine who truly owned their loan or had legal authority to enforce it.

How Documentation Failures Created Opportunities for Fraud

One of the most significant factors behind home loan securitization fraud was the breakdown of documentation practices within the mortgage industry. Mortgage loans require precise documentation to establish legal ownership and enforceability. These documents typically include the promissory note, mortgage or deed of trust, and assignment records that track each transfer of the loan.

During the housing boom, many institutions relied on automated systems and mass-processing techniques to manage loan transfers. While these systems increased efficiency, they also increased the likelihood of errors. In some cases, critical documents were lost, improperly signed, or never transferred to the appropriate trust as required by securitization agreements.

This breakdown in documentation created legal vulnerabilities. If a mortgage note was not properly transferred to the securitized trust within the required timeframe, the trust might not have legal standing to enforce the loan. Yet foreclosures sometimes proceeded regardless of these discrepancies. Such situations became key examples cited by critics when discussing home loan securitization fraud and its impact on homeowners.

Additionally, the widespread use of “robo-signing” practices intensified the problem. Robo-signing involved employees signing thousands of legal documents without verifying the information contained in them. Courts later discovered instances where signatures were fabricated or notarizations were improperly executed. These practices raised serious concerns about the authenticity of foreclosure documents and further highlighted systemic problems associated with home loan securitization fraud.

The Role of Financial Institutions and Rating Agencies

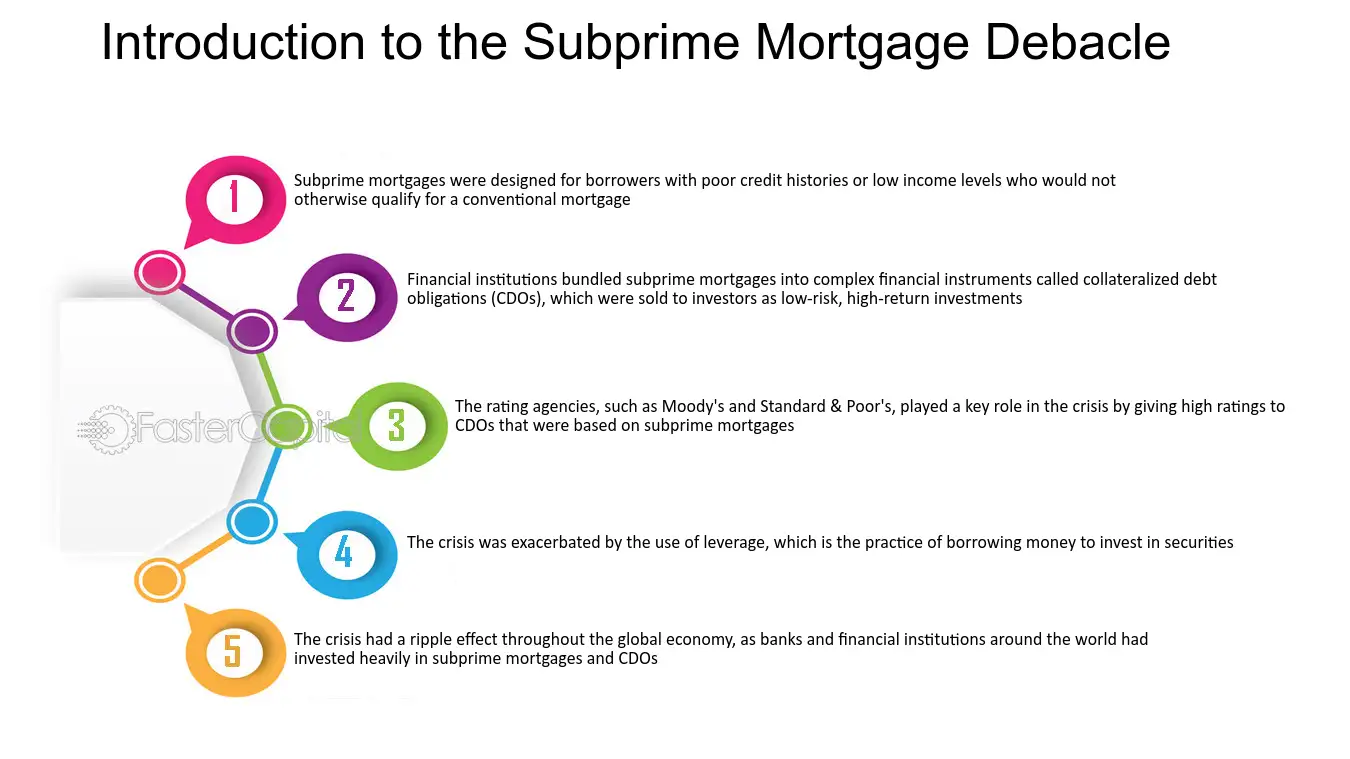

Another dimension of home loan securitization fraud involves the roles played by investment banks, rating agencies, and financial intermediaries. Investment banks structured and sold mortgage-backed securities to investors around the world. To make these securities attractive, they relied heavily on ratings provided by credit rating agencies.

Rating agencies were expected to evaluate the risk associated with mortgage-backed securities. However, during the housing boom, many securities backed by risky or subprime loans received high credit ratings. Investors relied on these ratings when purchasing securities, assuming they represented relatively safe investments.

In hindsight, critics argue that some institutions misrepresented the quality of the underlying mortgage loans. Loans with weak underwriting standards or incomplete documentation were sometimes packaged into securities marketed as low-risk investments. When borrowers began defaulting on their loans, the weaknesses in these securities became apparent.

This misalignment between the actual quality of loans and their representation in financial markets became a central issue during the mortgage crisis. Allegations of home loan securitization fraud often centered on whether financial institutions knowingly sold securities backed by problematic loans while failing to disclose the associated risks.

Legal Battles and Borrower Challenges

As the foreclosure crisis unfolded, many borrowers began questioning the legality of foreclosure actions initiated by banks and loan servicers. Legal challenges emerged across various jurisdictions, with homeowners and attorneys examining whether lenders had the proper documentation to enforce mortgages.

In some cases, borrowers discovered irregularities in the chain of title for their mortgage loans. Missing assignments, incorrect transfer dates, and inconsistent documentation raised doubts about whether the loans had been legally securitized. These findings fueled broader debates about home loan securitization fraud and whether certain foreclosure actions were legally valid.

Courts responded in different ways. Some judges dismissed foreclosure cases when lenders could not demonstrate clear ownership of the mortgage note. Other courts allowed lenders to correct documentation errors and proceed with foreclosure. Regardless of the outcomes, these legal battles brought national attention to the complexities surrounding home loan securitization fraud.

For borrowers, the experience often highlighted the imbalance of power within the mortgage system. Financial institutions possessed extensive legal resources and documentation infrastructure, while homeowners frequently struggled to obtain basic information about their loans. This disparity made it challenging for borrowers to fully investigate potential irregularities in their mortgage transactions.

Lessons Borrowers Must Learn from the Mortgage Crisis

The mortgage crisis revealed profound weaknesses in the financial systems that governed home lending. One of the most important lessons for borrowers is the importance of understanding the legal structure behind their mortgage agreements. Awareness of how loans can be transferred, securitized, and serviced can help homeowners recognize potential irregularities.

Education is also essential in preventing future issues related to home loan securitization fraud. Borrowers should carefully review loan documents before signing and retain copies of all relevant paperwork. Maintaining records of mortgage statements, assignments, and correspondence with lenders can provide valuable evidence if disputes arise later.

Another key lesson involves vigilance. Homeowners should pay close attention to notices regarding loan transfers or servicing changes. If the entity collecting payments suddenly changes, borrowers should request written verification confirming the authority of the new servicer. Such steps can help ensure that payments are being made to the correct party.

The mortgage crisis also demonstrated the need for stronger regulatory oversight within the financial industry. While reforms have been introduced in many countries, the complexity of mortgage securitization continues to present challenges for regulators and consumers alike. Understanding the historical context of home loan securitization fraud can empower borrowers to demand greater transparency and accountability from financial institutions.

Ultimately, the lessons of the mortgage crisis extend far beyond the financial markets. They remind borrowers that homeownership involves not only financial responsibility but also legal awareness. By learning from past mistakes and staying informed about the risks associated with home loan securitization fraud, homeowners can better protect themselves and navigate the complexities of the modern mortgage system with greater confidence.

Conclusion

The mortgage crisis revealed how complex financial systems can affect ordinary homeowners in unexpected ways. At the center of many legal and financial debates was home loan securitization fraud, a problem that exposed serious weaknesses in mortgage documentation, loan transfers, and regulatory oversight. What many borrowers once viewed as a simple home loan often became part of a complicated financial structure involving multiple institutions, investors, and servicing companies. When these systems failed to maintain proper records or follow required legal procedures, the consequences were felt most strongly by homeowners facing confusion and uncertainty.

Understanding home loan securitization fraud is therefore essential for modern borrowers. The lessons from the mortgage crisis highlight the importance of transparency, proper documentation, and borrower awareness. Homeowners must recognize that mortgages may be transferred or securitized several times during the life of the loan, making it critical to maintain accurate records and verify the legitimacy of loan servicing entities.

Moving forward, awareness and education remain the strongest defenses against potential irregularities. By learning about the risks associated with home loan securitization fraud, borrowers can better protect their financial interests, ask informed questions, and demand accountability from lenders and financial institutions. Ultimately, a well-informed borrower is far better equipped to navigate the complexities of today’s mortgage landscape.

Turn Complex Mortgage Evidence Into Powerful Legal Advantage

In complex mortgage litigation and compliance matters, clarity is everything. When documentation, securitization history, and loan transfers become difficult to interpret, professional forensic analysis can make the difference between uncertainty and strategic confidence. That’s where Mortgage Audits Online steps in—providing detailed mortgage securitization and forensic audit services designed specifically for industry professionals.

For over four years, Mortgage Audits Online has supported attorneys, legal teams, and mortgage professionals by delivering structured, evidence-based audit reports that help uncover documentation inconsistencies, securitization chain issues, and compliance concerns. Their forensic mortgage audits carefully examine loan documents, assignments, payment histories, and securitization records to identify discrepancies that could influence litigation strategy or settlement discussions.

Unlike consumer-facing services, Mortgage Audits Online operates exclusively as a business-to-business provider, ensuring their reports are tailored to the analytical and documentation standards required by legal and financial professionals. Their work is structured for real-world use—supporting case evaluation, foreclosure defense strategies, and compliance reviews with clear, organized findings that can withstand professional scrutiny.

When your clients’ cases require precision, credibility, and documented insights, partnering with the right forensic audit provider becomes a strategic decision. Mortgage Audits Online helps professionals transform complex mortgage records into clear, actionable intelligence that strengthens case preparation and supports informed decision-making.

When clarity, documentation, and professional insight matter most, working with the right forensic mortgage audit partner can transform uncertainty into strategic advantage.

Connect with Mortgage Audits Online

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

Equip your cases with deeper mortgage intelligence, stronger documentation, and the professional analysis they deserve. Partner with Mortgage Audits Online today and elevate the strength, clarity, and credibility of every case you build.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}