Legal Experts Discuss the Impact of Home Loan Securitization Fraud on Homeowners

The modern mortgage system is built on complex financial structures that most homeowners rarely see or fully understand. While borrowers typically focus on interest rates, repayment schedules, and monthly installments, the financial journey of their mortgage often extends far beyond the original lender. In today’s global financial markets, many home loans are bundled together and sold as investment products in a process known as securitization. Although securitization can help banks maintain liquidity and expand lending opportunities, it has also created an environment where transparency is sometimes lost. This lack of clarity has opened the door to serious legal concerns, particularly those related to home loan securitization fraud.

Legal experts across the financial and consumer protection sectors have increasingly raised concerns about how home loan securitization fraud affects homeowners, borrowers, and even the broader housing market. In simple terms, securitization involves converting mortgage loans into tradable securities that investors can purchase. While this financial practice is legal and widely used, problems arise when documentation errors, ownership misrepresentation, or improper loan transfers occur during the process. When these issues are not handled properly, they may lead to disputes about who truly owns the mortgage note and who has the legal authority to enforce foreclosure.

For homeowners, the consequences of home loan securitization fraud can be profound and sometimes devastating. Many borrowers assume their mortgage remains with the lender that issued the loan. However, once a loan enters the securitization pipeline, it may be sold, transferred, or assigned multiple times to different entities, including investment trusts and servicing companies. Legal professionals have observed that in some cases, these transfers are not documented correctly, which can create serious legal gaps. When foreclosure proceedings begin, homeowners may discover that the entity attempting to enforce the mortgage cannot properly demonstrate ownership of the loan.

Attorneys specializing in foreclosure defense frequently highlight that home loan securitization fraud often revolves around incomplete or questionable paperwork. Mortgage assignments may be backdated, signatures may be questionable, or key documents may be missing entirely. In certain cases, the original promissory note—the document that proves the borrower’s obligation—cannot be located. These documentation issues can significantly complicate foreclosure cases and raise legal questions about the validity of the claims made against homeowners.

Another major concern raised by legal experts involves the role of mortgage servicers in cases involving home loan securitization fraud. Mortgage servicers are responsible for collecting payments, managing escrow accounts, and communicating with borrowers. However, they often do not actually own the loan itself. This separation between loan ownership and loan servicing can create confusion for homeowners trying to resolve disputes or negotiate loan modifications. When documentation is unclear or inaccurate, borrowers may find themselves trapped in a system where accountability becomes difficult to establish.

The legal implications of home loan securitization fraud extend beyond individual homeowners and can influence the integrity of the financial system itself. Courts across multiple jurisdictions have seen cases where securitized loans were transferred into trusts after legal deadlines had passed or where the chain of ownership was incomplete. Such irregularities can undermine investor confidence and create legal vulnerabilities for financial institutions. As a result, many legal professionals argue that stronger regulatory oversight and stricter documentation standards are necessary to ensure transparency within the securitization process.

Consumer advocates and legal analysts also emphasize the importance of education and awareness when addressing home loan securitization fraud. Many homeowners are unaware that their mortgage may have been securitized or that irregularities in the securitization process could impact their legal rights. By understanding how securitization works and recognizing potential red flags, borrowers may be better equipped to challenge questionable foreclosure actions and seek legal assistance when necessary.

Ultimately, the growing discussion around home loan securitization fraud highlights the need for greater transparency within the mortgage industry. Legal experts continue to examine how financial institutions manage loan transfers, maintain documentation, and enforce foreclosure proceedings. As courts, regulators, and consumer advocates work to address these challenges, the goal remains clear: protecting homeowners while maintaining the stability and credibility of the housing finance system.

Next part in 1000 words following the introduction with headings , no subheadings Use KW meaningfully.

Understanding the Foundations of Home Loan Securitization

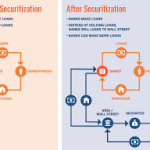

To fully understand the legal debates surrounding home loan securitization fraud, it is important to first examine how mortgage securitization works. Securitization is a financial process through which lenders bundle large numbers of home loans together and convert them into investment products known as mortgage-backed securities. These securities are then sold to investors such as pension funds, insurance companies, and institutional investors seeking steady returns.

In theory, securitization offers several benefits. It allows lenders to free up capital so they can issue new loans, helps spread financial risk among investors, and creates liquidity within the housing market. However, legal experts point out that the complexity of this system can sometimes lead to serious documentation errors or questionable loan transfers. When proper procedures are not followed, the system that was designed to increase efficiency can instead become vulnerable to home loan securitization fraud.

Mortgage loans often pass through several entities during securitization. These may include originators, aggregators, trustees, servicers, and investors. Each step requires accurate documentation that proves ownership and maintains the legal chain of title. If any part of this process is mishandled, it can create confusion about who actually owns the loan. Legal professionals argue that such confusion is often at the heart of many disputes related to home loan securitization fraud.

Another critical issue involves the trust structures used in securitization. Mortgage loans are typically transferred into special investment trusts that issue mortgage-backed securities. These trusts operate under strict guidelines and deadlines for accepting loans. If a loan is transferred improperly or after the closing date of the trust, it may raise legal concerns about whether the transfer is valid. Such irregularities are frequently cited in cases involving home loan securitization fraud, where the legitimacy of the loan ownership becomes a key legal question.

Understanding this structure is essential for homeowners and legal professionals alike. Without a clear chain of documentation, it becomes difficult to determine whether the party seeking to enforce the loan has the legal authority to do so. This is why the conversation about home loan securitization fraud often centers on transparency, accountability, and the need for stronger oversight within the mortgage industry.

Legal Concerns Raised by Mortgage Documentation Irregularities

One of the most significant issues discussed by legal experts involves the documentation used during mortgage transfers. Every time a loan changes ownership, a record must be created to show the transfer from one party to another. This chain of documentation ensures that the current holder of the mortgage note has the legal right to enforce the loan.

In cases involving home loan securitization fraud, legal professionals often discover missing or incomplete documents. Mortgage assignments may appear years after the original transfer supposedly occurred, raising questions about whether the transaction was properly recorded at the time. In some instances, documents appear to have been signed by individuals who lacked proper authorization or whose identities cannot be verified.

Courts have increasingly scrutinized such irregularities because accurate documentation is essential for protecting the rights of homeowners. When foreclosure proceedings begin, the lender or servicing company must prove that it has the legal authority to enforce the mortgage. If documentation is inconsistent or incomplete, homeowners may challenge the foreclosure on the basis that the party seeking enforcement does not have proper ownership of the loan.

Legal analysts frequently emphasize that home loan securitization fraud does not necessarily involve intentional deception in every case. Sometimes the problem arises from large-scale administrative errors, poor record keeping, or the use of automated systems that generate documents without proper verification. However, regardless of whether the errors were intentional or accidental, the legal consequences can still be significant.

Another major concern involves the practice commonly referred to as “robo-signing.” This occurs when individuals sign large volumes of mortgage documents without reviewing them carefully or verifying the information contained within them. Courts and regulatory agencies have criticized this practice because it undermines the reliability of mortgage records. In several high-profile cases, robo-signing has been linked to disputes involving home loan securitization fraud, where questionable documentation played a role in foreclosure proceedings.

These documentation issues highlight the importance of maintaining a clear and verifiable chain of ownership. Without it, the legal foundation of the mortgage system becomes unstable. Legal experts argue that stronger documentation standards and improved record-keeping practices are necessary to reduce the risk of disputes related to home loan securitization fraud.

The Impact of Home Loan Securitization Fraud on Homeowners

For homeowners, the consequences of home loan securitization fraud can be both financial and emotional. Many borrowers enter into mortgage agreements with the expectation that their lender will manage the loan responsibly and transparently. However, when loans are securitized and transferred between multiple institutions, borrowers may lose visibility into who actually owns their mortgage.

This lack of clarity can become particularly problematic when homeowners face financial difficulties and attempt to negotiate loan modifications or repayment plans. In cases involving home loan securitization fraud, borrowers sometimes encounter multiple companies claiming authority over the loan, each providing different instructions or documentation requirements. Such confusion can delay assistance and increase the risk of foreclosure.

Legal experts also note that homeowners may face challenges when attempting to verify the accuracy of their mortgage records. Because securitized loans often pass through several financial institutions, tracking the full history of the loan can be difficult. When discrepancies arise, homeowners may need legal assistance to investigate whether the loan was transferred properly.

Another major impact involves foreclosure proceedings. When a lender initiates foreclosure, it must demonstrate that it has the legal right to enforce the mortgage. In some cases involving home loan securitization fraud, courts have discovered that the party seeking foreclosure could not produce the original promissory note or prove a complete chain of ownership. Such cases have led to legal battles that delay foreclosure actions and raise questions about the reliability of mortgage documentation.

Beyond the courtroom, the broader psychological impact on homeowners should not be underestimated. Facing foreclosure is already a stressful experience, and the added uncertainty created by potential home loan securitization fraud can make the situation even more overwhelming. Borrowers may feel trapped in a complex financial system where identifying the responsible party becomes extremely difficult.

Legal professionals often advise homeowners to review mortgage records carefully and seek professional guidance if irregularities appear. By understanding how securitization works and recognizing possible warning signs, borrowers may be better prepared to protect their rights. As discussions about home loan securitization fraud continue within legal and financial circles, the primary goal remains ensuring that homeowners receive fair treatment within the mortgage system.

The ongoing examination of these issues reflects a broader effort to improve transparency and accountability in mortgage finance. As courts, regulators, and legal experts continue to address cases involving home loan securitization fraud, their decisions will likely influence how mortgage documentation, loan transfers, and foreclosure proceedings are handled in the future.

Conclusion

The growing legal discussion surrounding home loan securitization fraud highlights the importance of transparency, accountability, and proper documentation within the modern mortgage system. As mortgage loans move through complex securitization structures, the accuracy of records and the integrity of loan transfers become critical factors that affect both financial institutions and homeowners. When these processes are handled correctly, securitization can support a stable and efficient housing finance market. However, when documentation errors, questionable assignments, or unclear ownership chains emerge, serious legal concerns can arise.

Legal experts continue to emphasize that home loan securitization fraud often centers on the failure to maintain a clear and verifiable chain of title for mortgage loans. Without reliable records, disputes may arise over who has the authority to enforce a loan or initiate foreclosure proceedings. These issues can create uncertainty for borrowers and complicate the work of courts, regulators, and financial professionals.

For homeowners and legal practitioners alike, understanding the mechanics of securitization is becoming increasingly important. Greater awareness, stronger regulatory oversight, and improved documentation standards can help reduce the risks associated with home loan securitization fraud. As the legal system continues to examine these cases, the focus remains on protecting homeowner rights while preserving the stability and credibility of the broader mortgage industry.

Top of Form

Bottom of Form

Gain the Insight You Need. Build Stronger Cases. Deliver Powerful Results

In today’s complex mortgage and foreclosure landscape, having clear, accurate financial analysis can make all the difference in how effectively a case is prepared and presented. Legal professionals, foreclosure defense specialists, and industry consultants often face intricate documentation and securitization structures that require expert evaluation. That is where professional audit support becomes an essential advantage.

For more than four years, our team has partnered with professionals to help uncover critical details within mortgage documentation through advanced securitization and forensic auditing services. Our work is designed exclusively for business professionals, helping attorneys, legal researchers, and industry specialists strengthen their strategies with reliable, data-driven insights.

At Mortgage Audits Online, we understand how important precision and credibility are when preparing legal arguments or evaluating mortgage documentation. Our forensic and securitization audits are developed to identify inconsistencies, documentation gaps, and structural irregularities that may influence the strength of a case. By providing thorough analysis and carefully prepared reports, we help our associates build more compelling and well-supported case files.

Our approach focuses on clarity, efficiency, and professional collaboration. Each audit is conducted with attention to detail, ensuring that the information delivered to our associates is both actionable and easy to understand. Whether you are reviewing complex mortgage transfers or examining securitization structures, our team works to provide insights that can support deeper investigation and informed decision-making.

We are proud to operate as a dedicated business-to-business provider, supporting professionals who require dependable research and audit services. Over the years, our associates have relied on our expertise to enhance their case preparation and strengthen their ability to advocate effectively for their clients.

If you are looking to add a layer of professional insight to your mortgage or foreclosure analysis, our team is ready to support your work with dependable forensic auditing and securitization reviews.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Learn more:

Precision. Reliability. Insight. Your Strategic Advantage.

The modern mortgage system is built on complex financial structures that most homeowners rarely see or fully understand. While borrowers typically focus on interest rates, repayment schedules, and monthly installments, the financial journey of their mortgage often extends far beyond the original lender. In today’s global financial markets, many home loans are bundled together and sold as investment products in a process known as securitization. Although securitization can help banks maintain liquidity and expand lending opportunities, it has also created an environment where transparency is sometimes lost. This lack of clarity has opened the door to serious legal concerns, particularly those related to home loan securitization fraud.

Legal experts across the financial and consumer protection sectors have increasingly raised concerns about how home loan securitization fraud affects homeowners, borrowers, and even the broader housing market. In simple terms, securitization involves converting mortgage loans into tradable securities that investors can purchase. While this financial practice is legal and widely used, problems arise when documentation errors, ownership misrepresentation, or improper loan transfers occur during the process. When these issues are not handled properly, they may lead to disputes about who truly owns the mortgage note and who has the legal authority to enforce foreclosure.

For homeowners, the consequences of home loan securitization fraud can be profound and sometimes devastating. Many borrowers assume their mortgage remains with the lender that issued the loan. However, once a loan enters the securitization pipeline, it may be sold, transferred, or assigned multiple times to different entities, including investment trusts and servicing companies. Legal professionals have observed that in some cases, these transfers are not documented correctly, which can create serious legal gaps. When foreclosure proceedings begin, homeowners may discover that the entity attempting to enforce the mortgage cannot properly demonstrate ownership of the loan.

Attorneys specializing in foreclosure defense frequently highlight that home loan securitization fraud often revolves around incomplete or questionable paperwork. Mortgage assignments may be backdated, signatures may be questionable, or key documents may be missing entirely. In certain cases, the original promissory note—the document that proves the borrower’s obligation—cannot be located. These documentation issues can significantly complicate foreclosure cases and raise legal questions about the validity of the claims made against homeowners.

Another major concern raised by legal experts involves the role of mortgage servicers in cases involving home loan securitization fraud. Mortgage servicers are responsible for collecting payments, managing escrow accounts, and communicating with borrowers. However, they often do not actually own the loan itself. This separation between loan ownership and loan servicing can create confusion for homeowners trying to resolve disputes or negotiate loan modifications. When documentation is unclear or inaccurate, borrowers may find themselves trapped in a system where accountability becomes difficult to establish.

The legal implications of home loan securitization fraud extend beyond individual homeowners and can influence the integrity of the financial system itself. Courts across multiple jurisdictions have seen cases where securitized loans were transferred into trusts after legal deadlines had passed or where the chain of ownership was incomplete. Such irregularities can undermine investor confidence and create legal vulnerabilities for financial institutions. As a result, many legal professionals argue that stronger regulatory oversight and stricter documentation standards are necessary to ensure transparency within the securitization process.

Consumer advocates and legal analysts also emphasize the importance of education and awareness when addressing home loan securitization fraud. Many homeowners are unaware that their mortgage may have been securitized or that irregularities in the securitization process could impact their legal rights. By understanding how securitization works and recognizing potential red flags, borrowers may be better equipped to challenge questionable foreclosure actions and seek legal assistance when necessary.

Ultimately, the growing discussion around home loan securitization fraud highlights the need for greater transparency within the mortgage industry. Legal experts continue to examine how financial institutions manage loan transfers, maintain documentation, and enforce foreclosure proceedings. As courts, regulators, and consumer advocates work to address these challenges, the goal remains clear: protecting homeowners while maintaining the stability and credibility of the housing finance system.

Next part in 1000 words following the introduction with headings , no subheadings Use KW meaningfully.

Understanding the Foundations of Home Loan Securitization

To fully understand the legal debates surrounding home loan securitization fraud, it is important to first examine how mortgage securitization works. Securitization is a financial process through which lenders bundle large numbers of home loans together and convert them into investment products known as mortgage-backed securities. These securities are then sold to investors such as pension funds, insurance companies, and institutional investors seeking steady returns.

In theory, securitization offers several benefits. It allows lenders to free up capital so they can issue new loans, helps spread financial risk among investors, and creates liquidity within the housing market. However, legal experts point out that the complexity of this system can sometimes lead to serious documentation errors or questionable loan transfers. When proper procedures are not followed, the system that was designed to increase efficiency can instead become vulnerable to home loan securitization fraud.

Mortgage loans often pass through several entities during securitization. These may include originators, aggregators, trustees, servicers, and investors. Each step requires accurate documentation that proves ownership and maintains the legal chain of title. If any part of this process is mishandled, it can create confusion about who actually owns the loan. Legal professionals argue that such confusion is often at the heart of many disputes related to home loan securitization fraud.

Another critical issue involves the trust structures used in securitization. Mortgage loans are typically transferred into special investment trusts that issue mortgage-backed securities. These trusts operate under strict guidelines and deadlines for accepting loans. If a loan is transferred improperly or after the closing date of the trust, it may raise legal concerns about whether the transfer is valid. Such irregularities are frequently cited in cases involving home loan securitization fraud, where the legitimacy of the loan ownership becomes a key legal question.

Understanding this structure is essential for homeowners and legal professionals alike. Without a clear chain of documentation, it becomes difficult to determine whether the party seeking to enforce the loan has the legal authority to do so. This is why the conversation about home loan securitization fraud often centers on transparency, accountability, and the need for stronger oversight within the mortgage industry.

Legal Concerns Raised by Mortgage Documentation Irregularities

One of the most significant issues discussed by legal experts involves the documentation used during mortgage transfers. Every time a loan changes ownership, a record must be created to show the transfer from one party to another. This chain of documentation ensures that the current holder of the mortgage note has the legal right to enforce the loan.

In cases involving home loan securitization fraud, legal professionals often discover missing or incomplete documents. Mortgage assignments may appear years after the original transfer supposedly occurred, raising questions about whether the transaction was properly recorded at the time. In some instances, documents appear to have been signed by individuals who lacked proper authorization or whose identities cannot be verified.

Courts have increasingly scrutinized such irregularities because accurate documentation is essential for protecting the rights of homeowners. When foreclosure proceedings begin, the lender or servicing company must prove that it has the legal authority to enforce the mortgage. If documentation is inconsistent or incomplete, homeowners may challenge the foreclosure on the basis that the party seeking enforcement does not have proper ownership of the loan.

Legal analysts frequently emphasize that home loan securitization fraud does not necessarily involve intentional deception in every case. Sometimes the problem arises from large-scale administrative errors, poor record keeping, or the use of automated systems that generate documents without proper verification. However, regardless of whether the errors were intentional or accidental, the legal consequences can still be significant.

Another major concern involves the practice commonly referred to as “robo-signing.” This occurs when individuals sign large volumes of mortgage documents without reviewing them carefully or verifying the information contained within them. Courts and regulatory agencies have criticized this practice because it undermines the reliability of mortgage records. In several high-profile cases, robo-signing has been linked to disputes involving home loan securitization fraud, where questionable documentation played a role in foreclosure proceedings.

These documentation issues highlight the importance of maintaining a clear and verifiable chain of ownership. Without it, the legal foundation of the mortgage system becomes unstable. Legal experts argue that stronger documentation standards and improved record-keeping practices are necessary to reduce the risk of disputes related to home loan securitization fraud.

The Impact of Home Loan Securitization Fraud on Homeowners

For homeowners, the consequences of home loan securitization fraud can be both financial and emotional. Many borrowers enter into mortgage agreements with the expectation that their lender will manage the loan responsibly and transparently. However, when loans are securitized and transferred between multiple institutions, borrowers may lose visibility into who actually owns their mortgage.

This lack of clarity can become particularly problematic when homeowners face financial difficulties and attempt to negotiate loan modifications or repayment plans. In cases involving home loan securitization fraud, borrowers sometimes encounter multiple companies claiming authority over the loan, each providing different instructions or documentation requirements. Such confusion can delay assistance and increase the risk of foreclosure.

Legal experts also note that homeowners may face challenges when attempting to verify the accuracy of their mortgage records. Because securitized loans often pass through several financial institutions, tracking the full history of the loan can be difficult. When discrepancies arise, homeowners may need legal assistance to investigate whether the loan was transferred properly.

Another major impact involves foreclosure proceedings. When a lender initiates foreclosure, it must demonstrate that it has the legal right to enforce the mortgage. In some cases involving home loan securitization fraud, courts have discovered that the party seeking foreclosure could not produce the original promissory note or prove a complete chain of ownership. Such cases have led to legal battles that delay foreclosure actions and raise questions about the reliability of mortgage documentation.

Beyond the courtroom, the broader psychological impact on homeowners should not be underestimated. Facing foreclosure is already a stressful experience, and the added uncertainty created by potential home loan securitization fraud can make the situation even more overwhelming. Borrowers may feel trapped in a complex financial system where identifying the responsible party becomes extremely difficult.

Legal professionals often advise homeowners to review mortgage records carefully and seek professional guidance if irregularities appear. By understanding how securitization works and recognizing possible warning signs, borrowers may be better prepared to protect their rights. As discussions about home loan securitization fraud continue within legal and financial circles, the primary goal remains ensuring that homeowners receive fair treatment within the mortgage system.

The ongoing examination of these issues reflects a broader effort to improve transparency and accountability in mortgage finance. As courts, regulators, and legal experts continue to address cases involving home loan securitization fraud, their decisions will likely influence how mortgage documentation, loan transfers, and foreclosure proceedings are handled in the future.

Conclusion

The growing legal discussion surrounding home loan securitization fraud highlights the importance of transparency, accountability, and proper documentation within the modern mortgage system. As mortgage loans move through complex securitization structures, the accuracy of records and the integrity of loan transfers become critical factors that affect both financial institutions and homeowners. When these processes are handled correctly, securitization can support a stable and efficient housing finance market. However, when documentation errors, questionable assignments, or unclear ownership chains emerge, serious legal concerns can arise.

Legal experts continue to emphasize that home loan securitization fraud often centers on the failure to maintain a clear and verifiable chain of title for mortgage loans. Without reliable records, disputes may arise over who has the authority to enforce a loan or initiate foreclosure proceedings. These issues can create uncertainty for borrowers and complicate the work of courts, regulators, and financial professionals.

For homeowners and legal practitioners alike, understanding the mechanics of securitization is becoming increasingly important. Greater awareness, stronger regulatory oversight, and improved documentation standards can help reduce the risks associated with home loan securitization fraud. As the legal system continues to examine these cases, the focus remains on protecting homeowner rights while preserving the stability and credibility of the broader mortgage industry.

Top of Form

Bottom of Form

Gain the Insight You Need. Build Stronger Cases. Deliver Powerful Results

In today’s complex mortgage and foreclosure landscape, having clear, accurate financial analysis can make all the difference in how effectively a case is prepared and presented. Legal professionals, foreclosure defense specialists, and industry consultants often face intricate documentation and securitization structures that require expert evaluation. That is where professional audit support becomes an essential advantage.

For more than four years, our team has partnered with professionals to help uncover critical details within mortgage documentation through advanced securitization and forensic auditing services. Our work is designed exclusively for business professionals, helping attorneys, legal researchers, and industry specialists strengthen their strategies with reliable, data-driven insights.

At Mortgage Audits Online, we understand how important precision and credibility are when preparing legal arguments or evaluating mortgage documentation. Our forensic and securitization audits are developed to identify inconsistencies, documentation gaps, and structural irregularities that may influence the strength of a case. By providing thorough analysis and carefully prepared reports, we help our associates build more compelling and well-supported case files.

Our approach focuses on clarity, efficiency, and professional collaboration. Each audit is conducted with attention to detail, ensuring that the information delivered to our associates is both actionable and easy to understand. Whether you are reviewing complex mortgage transfers or examining securitization structures, our team works to provide insights that can support deeper investigation and informed decision-making.

We are proud to operate as a dedicated business-to-business provider, supporting professionals who require dependable research and audit services. Over the years, our associates have relied on our expertise to enhance their case preparation and strengthen their ability to advocate effectively for their clients.

If you are looking to add a layer of professional insight to your mortgage or foreclosure analysis, our team is ready to support your work with dependable forensic auditing and securitization reviews.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Learn more:

Precision. Reliability. Insight. Your Strategic Advantage.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}