Inside the Mortgage Market: The Truth about Home Loan Securitization Fraud

The modern mortgage industry operates through complex financial systems that many borrowers never see or fully understand. Behind the simple act of signing a home loan agreement lies an intricate network of financial transactions, investment vehicles, and institutional relationships. Over the past few decades, mortgage lending has evolved from a straightforward lender-borrower arrangement into a sophisticated marketplace where loans are frequently bundled, sold, and traded among investors. While this process, known as securitization, can improve liquidity in the financial system, it has also opened the door to serious irregularities. One of the most controversial issues within this framework is home loan securitization fraud, a topic that has gained increasing attention among legal experts, financial analysts, and consumer advocates.

At its core, home loan securitization fraud refers to deceptive or improper practices that occur when mortgage loans are pooled together and converted into securities for sale to investors. In a typical securitization process, a bank or mortgage lender originates loans and then transfers them into a trust, where they are packaged into mortgage-backed securities and sold on the secondary market. Investors purchase these securities expecting reliable returns generated from borrowers’ monthly mortgage payments. However, when documentation errors, misrepresentations, or improper transfers occur during this process, serious legal and financial complications can arise. These complications often form the foundation of allegations involving home loan securitization fraud.

One of the most troubling aspects of home loan securitization fraud is the lack of transparency that borrowers often face. Many homeowners assume that the bank they originally borrowed from continues to hold and service the loan. In reality, the loan may have been sold multiple times and transferred through various financial institutions or trusts. During these transfers, documentation such as promissory notes, mortgage assignments, and ownership records may be mishandled or inaccurately recorded. When these records become inconsistent or incomplete, questions about the lawful ownership of the loan can emerge—an issue frequently cited in investigations related to home loan securitization fraud.

The issue gained widespread attention following the 2008 financial crisis, when millions of homeowners faced foreclosure and courts began examining the paperwork behind mortgage ownership. Investigations uncovered cases where loan documents were improperly transferred, signed without verification, or even created after the fact to support foreclosure actions. Such irregularities sparked debates about whether lenders and servicers had the legal authority to enforce certain mortgages. These controversies further fueled scrutiny of home loan securitization fraud, prompting legal challenges and regulatory discussions in several jurisdictions.

Another significant concern surrounding home loan securitization fraud involves the role of mortgage servicers and intermediaries. Mortgage servicers are responsible for collecting payments, managing escrow accounts, and handling borrower communications. However, when servicing rights are separated from actual loan ownership—a common occurrence in securitized mortgages—borrowers may encounter conflicting information about who truly controls their loan. In some cases, servicing companies may pursue foreclosure actions on behalf of investors or trusts without clear documentation establishing proper authority. Situations like these often become central issues in cases alleging home loan securitization fraud.

Financial experts also highlight how the complexity of securitized mortgage structures can make it difficult for borrowers to trace the ownership of their loans. Securitization trusts may involve multiple parties, including originators, sponsors, depositors, trustees, and investors. Each entity plays a role in transferring and managing mortgage assets. When these transfers fail to follow strict legal and contractual requirements, the entire chain of ownership may be called into question. Such breakdowns in documentation and compliance are frequently cited as indicators of home loan securitization fraud, particularly in legal disputes over foreclosure rights.

Understanding home loan securitization fraud is essential for homeowners, legal professionals, and financial researchers seeking greater transparency in the mortgage industry. By examining how mortgage loans move through financial markets and identifying potential irregularities in documentation and ownership transfers, investigators and auditors can uncover critical information that may influence legal outcomes. As awareness grows, discussions around home loan securitization fraud continue to shape debates about consumer protection, financial accountability, and the integrity of mortgage-backed securities within the global financial system.

The Evolution of Mortgage Securitization in Modern Finance

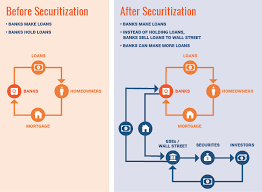

To understand the concerns surrounding home loan securitization fraud, it is essential to first explore how mortgage securitization became a dominant feature of the global financial system. Mortgage securitization emerged as a financial innovation designed to increase liquidity in lending markets. Traditionally, banks would issue a mortgage loan and hold it on their balance sheet until the borrower fully repaid it. This approach limited the number of loans a lender could offer because their capital remained tied to long-term mortgage obligations.

Securitization transformed this model by allowing lenders to convert mortgages into investment products. Instead of holding loans for decades, financial institutions began bundling thousands of mortgages into large pools and selling them as securities to investors. These mortgage-backed securities provided investors with income streams generated from borrowers’ monthly payments.

While securitization improved capital flow and expanded homeownership opportunities, it also introduced layers of complexity. Each mortgage loan could pass through multiple entities, including originators, sponsors, trustees, servicers, and investors. When these transfers occur without strict compliance with legal documentation and financial regulations, the system becomes vulnerable to errors and manipulation. This environment creates the conditions where home loan securitization fraud may occur.

The expansion of mortgage securitization during the late 1990s and early 2000s significantly increased the volume of loans moving through secondary markets. As competition among lenders intensified, the emphasis on speed and profit sometimes overshadowed the importance of accurate documentation and compliance. These weaknesses in the system later became central concerns in discussions about home loan securitization fraud, particularly during the financial crisis when millions of mortgages came under legal scrutiny.

Documentation Irregularities and Mortgage Ownership Conflicts

One of the most common issues associated with home loan securitization fraud involves documentation irregularities. Mortgage loans rely on a chain of legal documents that prove ownership and enforceability. These documents typically include the promissory note, mortgage or deed of trust, assignments, endorsements, and transfer records.

In a properly executed securitization process, these documents must be transferred in a precise order to ensure that the securitization trust legally owns the loan. However, investigations following the housing crisis revealed that many transfers did not follow the required procedures. In some cases, documents were signed without proper authorization or created retroactively to fill gaps in the ownership chain.

Such irregularities create significant legal challenges. When a financial institution attempts to enforce a mortgage or initiate foreclosure proceedings, it must demonstrate that it holds the legal right to do so. If documentation is incomplete or inconsistent, borrowers may challenge the legitimacy of the claim. These disputes often form the basis of allegations involving home loan securitization fraud, as they highlight potential misconduct in the transfer and management of mortgage assets.

Another problem arises when mortgages are transferred multiple times without clear records. The complexity of securitized mortgage structures means that a single loan may move through several entities before reaching a final investment trust. If even one step in the transfer process is mishandled, the chain of ownership may become legally questionable. These documentation failures continue to be a major focus in investigations related to home loan securitization fraud.

The Role of Mortgage Servicers and Financial Intermediaries

Mortgage servicers play a central role in the day-to-day administration of home loans. They collect monthly payments, manage escrow accounts, and communicate with borrowers about loan status. In securitized mortgage structures, servicers often operate on behalf of investors who own the mortgage-backed securities.

However, the separation between loan ownership and loan servicing can create confusion. Borrowers may interact only with the servicer while the actual loan ownership remains with a distant investment trust. This separation sometimes leads to situations where borrowers receive conflicting information about their loan status.

Concerns about home loan securitization fraud often arise when servicers pursue legal actions without clearly demonstrating their authority to act on behalf of the loan owner. In some documented cases, servicers initiated foreclosure proceedings while documentation regarding the loan’s transfer into a securitization trust remained incomplete or questionable.

Financial intermediaries involved in securitization transactions also contribute to the complexity of mortgage ownership. Sponsors, depositors, and trustees each perform specific roles in transferring and managing mortgage assets. If these parties fail to follow the contractual requirements outlined in securitization agreements, the legal standing of the mortgage trust may become uncertain. These complications highlight why investigations into home loan securitization fraud frequently focus on the relationships between servicers, trustees, and investors.

Legal and Financial Implications for Borrowers

The presence of home loan securitization fraud allegations has significant implications for borrowers. When the ownership of a mortgage becomes unclear, homeowners may face uncertainty regarding who has the authority to collect payments or enforce loan terms. This uncertainty can create confusion during loan modifications, refinancing negotiations, or foreclosure disputes.

In legal proceedings, borrowers sometimes challenge foreclosure actions by questioning whether the institution pursuing the claim possesses valid documentation proving ownership of the loan. Courts in several jurisdictions have examined these challenges closely, particularly in cases where documentation appeared inconsistent or incomplete.

Legal experts often rely on forensic mortgage audits to examine loan histories, transfer records, and securitization documents. These audits analyze whether mortgage loans were transferred according to the contractual requirements of the securitization trust. When irregularities are discovered, they may provide evidence supporting claims related to home loan securitization fraud.

Beyond individual foreclosure cases, the broader implications of these issues extend to financial markets as well. Mortgage-backed securities rely on accurate documentation and lawful ownership of underlying loans. If these elements are compromised, investor confidence may decline. For this reason, transparency and compliance are essential in maintaining trust within the mortgage securitization system.

The Growing Demand for Transparency and Financial Accountability

As awareness of home loan securitization fraud continues to grow, financial professionals and policymakers increasingly emphasize transparency and accountability in mortgage transactions. Regulatory reforms following the financial crisis aimed to strengthen oversight of mortgage origination and securitization practices.

New compliance requirements encourage lenders and financial institutions to maintain accurate records, follow strict transfer procedures, and disclose important information to borrowers and investors. These measures are designed to reduce the risk of documentation errors and prevent the types of irregularities associated with home loan securitization fraud.

At the same time, advances in financial auditing and digital recordkeeping have improved the ability to track mortgage ownership. Sophisticated forensic audits now allow investigators to analyze loan transfers across complex financial structures, revealing discrepancies that might otherwise remain hidden.

Legal professionals, financial analysts, and consumer advocates continue to explore ways to enhance transparency in mortgage markets. Their efforts focus on ensuring that mortgage ownership remains clearly documented and that borrowers receive accurate information about their loans.

Ultimately, the discussion surrounding home loan securitization fraud reflects broader concerns about financial accountability in modern lending systems. By examining how mortgages are transferred, managed, and enforced, industry experts aim to strengthen protections for borrowers while preserving the stability of the securitized mortgage market.

Conclusion

Understanding home loan securitization fraud is essential in today’s complex mortgage environment, where loans are frequently transferred, bundled, and sold across financial markets. What appears to borrowers as a simple lending agreement often becomes part of a much larger financial structure involving multiple institutions, investment trusts, and servicing entities. When documentation errors, improper transfers, or questionable practices occur during these transactions, concerns about home loan securitization fraud begin to emerge.

The growing scrutiny around home loan securitization fraud highlights the importance of transparency, proper documentation, and strict compliance with legal requirements throughout the securitization process. Borrowers, legal professionals, and financial analysts increasingly recognize the need to carefully examine mortgage ownership records and transfer histories. Such examinations help determine whether the entities enforcing a mortgage truly possess the legal authority to do so.

As financial markets continue to evolve, awareness of home loan securitization fraud plays a critical role in promoting accountability within the mortgage industry. Greater transparency, improved regulatory oversight, and detailed forensic mortgage audits can help identify irregularities and protect both homeowners and investors. By understanding the risks associated with home loan securitization fraud, stakeholders can work toward a more responsible, transparent, and trustworthy mortgage lending system that safeguards financial stability and consumer rights.

Please write a promotional CTA Motivational and professional in style With the information and also give an enticing Heading Unlock Clarity. Strengthen Your Case. Transform Your Client Outcomes We have been helping our associates build strong cases for over 4 years with our securitization and forensic audits. We are exclusively a business-to-business provider. Mortgage Audits Online 100 Rialto Place, Suite 700 Melbourne, FL 32901 📱 877-399-2995 📠 Fax: 877-398-5288 🌐 Visit: https://www.mortgageauditsonline.com/ Accuracy. Dependability. Insight. Advantage Please change the language a little bit and also the CTA title

Gain the Evidence Advantage for Every Mortgage Case

Strong cases begin with clear financial insight. When legal professionals and industry experts need reliable documentation and forensic mortgage analysis, the right audit can make all the difference. For more than four years, Mortgage Audits Online has supported professionals with detailed securitization and forensic mortgage audits designed to uncover critical information and strengthen case preparation.

Working exclusively as a business-to-business service provider, we partner with attorneys, consultants, investigators, and financial professionals who require dependable, well-documented audit reports. Our mission is simple: deliver precise, actionable analysis that helps our associates build stronger arguments, identify discrepancies, and move forward with confidence.

Our specialized audits examine loan documentation, securitization structures, transfers of ownership, and potential compliance issues within mortgage transactions. These insights can provide valuable leverage in negotiations, litigation, and investigative reviews. When accuracy and credibility matter, having a professional forensic audit can become a powerful strategic tool.

At Mortgage Audits Online, we combine experience, attention to detail, and deep industry knowledge to ensure that every report meets the highest standards of clarity and reliability. Our team understands the complexities of mortgage securitization and the importance of presenting findings in a way that professionals can confidently use in their case strategies.

If you are ready to elevate the strength of your mortgage cases, our team is prepared to assist.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Explore our services: Mortgage Audits Online Official Website

Precision. Reliability. Insight. Your Professional Edge.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}