Borrower Protection and the Rising Concerns Over Home Loan Securitization Fraud

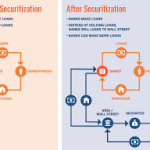

The modern housing finance system is built on complex financial structures that most borrowers never see or fully understand. While obtaining a home loan is often viewed as a straightforward process between a borrower and a lender, the reality behind the scenes can be far more intricate. In many cases, mortgages are bundled, sold, and traded in secondary markets through a process known as securitization. This system helps banks generate liquidity and continue lending, but it has also created opportunities for irregularities, misrepresentations, and documentation issues. These concerns have given rise to increasing scrutiny around home loan securitization fraud, a topic that has gained significant attention among financial analysts, legal professionals, and borrower advocacy groups.

At its core, securitization involves pooling thousands of individual mortgages and converting them into investment products that can be sold to investors. Financial institutions package these loans into mortgage-backed securities and distribute them across global financial markets. The intention behind securitization is to spread risk and increase capital flow within the financial system. However, when transparency is lacking or documentation becomes inconsistent, the process can lead to serious legal and ethical questions. Many borrowers and legal experts now argue that home loan securitization fraud may occur when loans are transferred improperly, recorded inaccurately, or when the true ownership of a mortgage becomes unclear.

For homeowners, the implications can be significant. Borrowers often assume their loan remains with the original lender, but in reality it may change ownership multiple times without their direct knowledge. When a mortgage is transferred through multiple entities—such as servicers, trustees, and investment trusts—the chain of title must remain accurate and verifiable. If documentation gaps appear, disputes may arise regarding who actually holds the legal right to enforce the mortgage. These concerns are central to many investigations and legal claims involving home loan securitization fraud, particularly in cases where foreclosure actions are challenged due to incomplete or questionable paperwork.

The global financial crisis of 2007–2008 highlighted how vulnerabilities in the securitization process could impact both financial institutions and everyday homeowners. During that period, rapid loan origination, weak underwriting standards, and large-scale securitization created an environment where documentation errors and financial misrepresentations became widespread. In the aftermath of the crisis, regulators, courts, and consumer advocates began paying closer attention to the structure of mortgage-backed securities and the legal validity of loan transfers. These developments intensified public awareness about home loan securitization fraud and the potential risks borrowers may face when mortgage ownership is unclear or improperly recorded.

Borrower protection has therefore become a growing priority in discussions about mortgage transparency and accountability. Homeowners facing foreclosure or loan disputes increasingly rely on forensic loan audits and securitization research to determine whether their mortgage was properly transferred and documented. Legal professionals often examine loan pooling agreements, trust closing dates, and mortgage assignment records to identify irregularities. When inconsistencies are discovered, they may indicate possible home loan securitization fraud, prompting further investigation into the chain of ownership and compliance with financial regulations.

Another important concern involves the role of mortgage servicers, which are companies responsible for collecting payments and managing borrower accounts. Servicers may change over time as loans are sold or transferred between financial entities. While borrowers continue making payments as instructed, they may not always receive clear explanations regarding who ultimately owns their mortgage note. In complex securitization structures, this lack of transparency can create confusion and make it difficult for borrowers to challenge errors or verify the legitimacy of foreclosure proceedings. Such situations are frequently cited in discussions about home loan securitization fraud, where the true holder of the loan may be difficult to identify.

The growing awareness of securitization-related issues has encouraged borrowers, attorneys, and financial experts to take a closer look at the documentation supporting mortgage transactions. By examining securitization reports, trust records, and loan assignment histories, investigators attempt to determine whether financial institutions followed the proper procedures required by law and contract. When discrepancies appear—such as assignments executed years after a trust’s closing date or missing endorsements on promissory notes—they may raise red flags connected to home loan securitization fraud.

As housing markets continue to evolve and financial products become increasingly sophisticated, the conversation surrounding borrower protection remains more relevant than ever. Transparency, accountability, and accurate documentation are essential to maintaining trust within the mortgage system. By understanding how securitization works and recognizing the warning signs associated with home loan securitization fraud, borrowers and professionals alike can better navigate the complexities of modern home lending and advocate for a more transparent financial environment.

Understanding the Mechanics Behind Home Loan Securitization

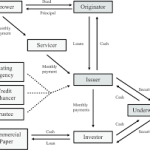

To fully grasp the risks associated with home loan securitization fraud, it is important to understand how the securitization process works in the modern financial system. When a borrower takes out a mortgage, the lender may not intend to keep that loan for the entire repayment period. Instead, many lenders sell mortgages to larger financial institutions or aggregators shortly after origination. These entities then bundle thousands of individual mortgages together into a pool. The pooled loans are transferred into special investment structures known as trusts, which issue mortgage-backed securities to investors.

The investors who purchase these securities receive payments generated from the mortgage borrowers’ monthly installments. In theory, the process creates a steady stream of income for investors while providing lenders with fresh capital to issue new loans. However, because mortgages can be transferred multiple times before reaching the final trust, the chain of ownership must be documented accurately at every stage. Any break in this chain may create legal uncertainty.

This is where concerns about home loan securitization fraud begin to emerge. If mortgage assignments are improperly executed, recorded after the fact, or missing altogether, it can create questions about whether the loan was legally transferred into the trust. When documentation does not follow the strict requirements set by pooling and servicing agreements, the legitimacy of the securitization structure may be challenged.

For borrowers, the complexity of these financial transactions often remains hidden. Most homeowners continue making their mortgage payments without realizing that their loan may have changed hands several times. When disputes arise, however, the securitization structure becomes highly relevant, especially if the entity enforcing the loan cannot clearly demonstrate ownership.

Documentation Breakdowns and Chain of Title Issues

One of the most frequently discussed issues surrounding home loan securitization fraud involves documentation errors within the chain of title. Every mortgage has two key documents: the promissory note, which represents the borrower’s promise to repay the loan, and the mortgage or deed of trust, which secures the loan with the property.

When a mortgage is sold or transferred, these documents must follow a specific legal process. The promissory note should be properly endorsed to the new owner, and the mortgage assignment should be recorded in public land records. These steps ensure that the legal ownership of the loan remains transparent and traceable.

During the rapid expansion of mortgage securitization in the early 2000s, however, many institutions processed loans at extremely high volumes. This fast-paced environment sometimes resulted in incomplete transfers, missing endorsements, or delayed assignments. In some cases, documents were created or signed years after the original transfer was supposed to occur.

These irregularities have become central to investigations into home loan securitization fraud. When documents are executed retroactively or when assignments appear inconsistent with the timeline of the securitization trust, legal professionals may question whether the loan was ever properly transferred. Such discrepancies can play a crucial role in foreclosure litigation and financial disputes.

Borrower Challenges During Foreclosure Proceedings

For many homeowners, the issue of home loan securitization fraud becomes most visible during foreclosure proceedings. When a borrower falls behind on payments, the entity seeking to foreclose must demonstrate that it has the legal authority to enforce the mortgage. This typically requires proof that the foreclosing party owns the promissory note or has the right to act on behalf of the owner.

If the chain of mortgage transfers is incomplete or inconsistent, borrowers may challenge the foreclosure by requesting documentation that proves ownership of the loan. In some cases, courts have examined whether the mortgage assignments were valid or whether the trust attempting to enforce the loan actually received the mortgage within the required time frame.

Legal disputes involving home loan securitization fraud often focus on whether financial institutions complied with the rules governing mortgage-backed securities trusts. These trusts usually have strict deadlines and procedures for transferring loans into the pool. If those procedures were not followed, questions may arise regarding the trust’s authority to enforce the mortgage.

Borrowers who uncover irregularities sometimes use securitization analysis as part of their legal defense. While not every documentation error invalidates a mortgage, courts may take such issues seriously if they reveal broader problems within the loan transfer process.

The Role of Mortgage Servicers and Loan Transfers

Another important dimension of home loan securitization fraud involves mortgage servicing companies. Servicers are responsible for collecting payments, managing escrow accounts, and communicating with borrowers on behalf of the loan owner. However, the servicer is not necessarily the actual owner of the mortgage.

As loans move through the securitization pipeline, servicing rights may also change hands. Borrowers may receive notices informing them that their loan servicing has been transferred to a different company. While these changes are common in the mortgage industry, they can create confusion when borrowers attempt to identify who ultimately owns their loan.

In situations where servicing transfers are poorly documented or where communication is unclear, borrowers may struggle to verify the legitimacy of payment instructions or foreclosure notices. These uncertainties can contribute to concerns about home loan securitization fraud, especially when the servicing company cannot clearly demonstrate its authority to act on behalf of the loan holder.

Transparency in servicing relationships is therefore essential. Borrowers must receive accurate information regarding the ownership and management of their mortgage. Without this transparency, the complex structure of securitized loans can create misunderstandings and legal conflicts.

Financial Market Pressures and the Growth of Securitization

The expansion of mortgage securitization was largely driven by the financial markets’ demand for investment products that generate steady income. Mortgage-backed securities became attractive to institutional investors such as pension funds, insurance companies, and investment firms seeking predictable returns.

However, the intense demand for securitized assets sometimes encouraged lenders to originate large volumes of mortgages quickly. In certain cases, underwriting standards weakened and documentation procedures became less rigorous. These conditions contributed to the broader financial instability that eventually surfaced during the global housing crisis.

Within this environment, allegations of home loan securitization fraud began to surface more frequently. Investigations revealed instances where mortgage documentation was incomplete, improperly transferred, or recreated to support foreclosure actions. These discoveries sparked significant debate among regulators, consumer advocates, and financial institutions.

The lessons from that period continue to influence modern discussions about financial transparency. Today, policymakers and legal experts emphasize the importance of maintaining accurate loan records and ensuring that securitization processes follow established legal guidelines.

The Importance of Transparency and Borrower Awareness

As the mortgage industry continues to evolve, borrower awareness plays an increasingly important role in preventing disputes related to home loan securitization fraud. Homeowners who understand the basic structure of mortgage transfers are better equipped to ask questions and request documentation when necessary.

For example, borrowers can request information about their loan owner, review public land records for mortgage assignments, and examine servicing notices carefully. Legal professionals may also conduct forensic loan audits to identify potential irregularities within the securitization process.

While most mortgages function within legitimate financial frameworks, transparency remains essential to maintaining trust in the system. Clear documentation, consistent recordkeeping, and open communication between lenders, servicers, and borrowers help reduce the risk of misunderstandings and legal disputes.

Ultimately, the growing conversation about home loan securitization fraud reflects a broader effort to ensure accountability within the housing finance system. By promoting transparency and strengthening borrower protections, financial institutions and regulators can help restore confidence in the processes that support homeownership and mortgage lending.

Conclusion

The growing attention surrounding home loan securitization fraud highlights the importance of transparency, accountability, and proper documentation within the modern mortgage system. As home loans move through complex financial channels involving lenders, investors, trusts, and servicing companies, the need for accurate records becomes critical. When mortgage transfers are not properly documented or when ownership of a loan becomes unclear, serious legal and financial concerns can arise for both borrowers and financial institutions.

Understanding the risks associated with home loan securitization fraud allows borrowers to become more informed about how their mortgages may be handled within the broader financial marketplace. While securitization itself is a legitimate financial process designed to improve liquidity and expand lending opportunities, the lack of clear documentation or oversight can create opportunities for irregularities. These issues may surface during loan disputes, foreclosure proceedings, or forensic mortgage investigations.

Ultimately, greater borrower awareness, improved regulatory oversight, and stronger industry practices can help reduce the likelihood of home loan securitization fraud. By emphasizing transparency and ensuring that every mortgage transfer follows proper legal procedures, the housing finance system can better protect homeowners while maintaining confidence in the mortgage lending process.

Gain Deeper Financial Insight. Strengthen Legal Strategies. Deliver Stronger Results

When complex mortgage structures raise questions, having the right analytical support can make all the difference. Our specialized securitization and forensic mortgage audits are designed to help professionals uncover critical financial details, clarify loan histories, and strengthen the foundation of their cases.

For more than four years, we have worked alongside industry associates, providing reliable audit reports and detailed securitization research that help identify documentation inconsistencies and hidden financial structures. Our services are designed exclusively for business professionals—attorneys, investigators, consultants, and other industry partners—who require dependable, evidence-based mortgage analysis.

Our experienced team focuses on accuracy, clarity, and actionable insights. By examining loan transfers, securitization records, and financial documentation, we provide the information professionals need to evaluate mortgage transactions with confidence. Each report is carefully prepared to support strategic decision-making and case development.

If you are seeking dependable securitization analysis and forensic audit support, our team is ready to assist you.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit:

Precision. Reliability. Insight. Your Professional Advantage.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}