The Shocking Reality of Home Loan Securitization Fraud in the Mortgage Industry

In the modern financial world, the mortgage industry plays a crucial role in helping millions of individuals achieve the dream of homeownership. However, beneath the surface of this essential financial system lies a complex and often misunderstood mechanism that has raised serious concerns among borrowers, legal experts, and financial analysts alike. One of the most alarming issues that has emerged over the past few decades is home loan securitization fraud, a practice that has significantly impacted homeowners, investors, and the integrity of financial markets.

At its core, home loan securitization fraud refers to deceptive or improper practices involved in the securitization of residential mortgages. Securitization itself is not inherently illegal. In fact, it is a legitimate financial process where banks and financial institutions bundle thousands of mortgage loans together and sell them as securities to investors. These securities, often known as mortgage-backed securities, are traded in global financial markets and provide liquidity to lenders so they can continue issuing new home loans. However, when transparency and compliance are ignored, the securitization process can become a breeding ground for fraud.

The roots of home loan securitization fraud can be traced back to the rapid expansion of mortgage lending and the financial engineering that dominated the housing market in the early 2000s. During this period, lenders, investment banks, and mortgage servicers aggressively pushed mortgage products into the market. Many of these loans were quickly transferred into securitized trusts without strict adherence to the legal procedures required to transfer ownership of the mortgage notes and deeds. As a result, documentation errors, missing assignments, and improper transfers became widespread.

One of the most troubling aspects of home loan securitization fraud involves the breakdown of the chain of title. In a properly executed mortgage transaction, the ownership of the loan must be clearly documented as it moves from the originator to subsequent entities and eventually into a securitized trust. Unfortunately, in many cases, this chain of ownership became fragmented or incomplete. Loans were sold multiple times, documents were fabricated after the fact, and signatures were often produced through questionable practices such as robo-signing.

For homeowners facing foreclosure, home loan securitization fraud has become a critical issue. Borrowers frequently discover that the entity attempting to foreclose on their property cannot produce the original loan documents or demonstrate a clear legal right to enforce the mortgage. This lack of documentation has led to numerous legal disputes and has raised serious questions about whether certain foreclosure actions were conducted lawfully. Courts in several jurisdictions have examined cases where the legitimacy of the loan transfer process was challenged due to inconsistencies in securitization records.

The impact of home loan securitization fraud extends beyond individual homeowners. Investors who purchased mortgage-backed securities also suffered substantial losses when underlying loans were improperly documented or misrepresented. In many cases, securities were marketed as high-quality investments backed by properly secured mortgages. However, when defaults increased and the true condition of the loan portfolios became apparent, the financial consequences were severe. This systemic failure contributed to the broader financial instability witnessed during the global housing crisis.

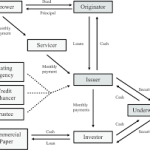

Another factor contributing to the fraud is the complexity of the securitization structure itself. The process often involves multiple parties, including mortgage originators, aggregators, investment banks, trustees, and servicing companies. Each of these participants plays a role in transferring, managing, or enforcing the loans within a securitized pool. When oversight is weak or compliance procedures are ignored, opportunities for misrepresentation and documentation irregularities increase dramatically.

In recent years, increased scrutiny from regulators, consumer advocates, and legal professionals has brought greater attention to home loan securitization fraud. Investigations, lawsuits, and financial settlements have revealed patterns of misconduct that were once hidden behind layers of financial transactions. These developments have sparked ongoing debates about accountability, transparency, and the need for stronger regulatory frameworks within the mortgage industry.

Understanding home loan securitization fraud is essential for borrowers, legal practitioners, and financial professionals who seek to navigate the complexities of mortgage finance. As more information continues to emerge, the conversation surrounding securitization practices is evolving, shedding light on the structural weaknesses that allowed fraudulent activities to flourish. By examining these issues carefully, stakeholders can better understand the risks involved and work toward a more transparent and accountable mortgage system.

Understanding the Foundations of Home Loan Securitization

To fully grasp the depth of home loan securitization fraud, it is essential to understand how mortgage securitization was originally designed to function. Securitization emerged as a financial innovation intended to increase liquidity in the housing market. Instead of holding mortgage loans for decades, lenders could sell them into large financial pools that were then converted into mortgage-backed securities and sold to investors. This process allowed banks to recover their capital quickly and issue new loans to additional borrowers.

In theory, securitization benefits both lenders and homeowners. Financial institutions gain access to continuous funding, while borrowers gain easier access to credit and home financing. However, the rapid expansion of mortgage lending created a system where speed often replaced accuracy. As the demand for mortgage-backed securities grew, many institutions began prioritizing volume over proper documentation and compliance. This environment created fertile ground for home loan securitization fraud to develop.

Mortgage loans were frequently transferred multiple times between lenders, aggregators, and investment banks before being placed into securitized trusts. Each transfer required precise documentation and legal assignments to ensure the loan’s ownership remained clear. When these steps were rushed or skipped entirely, inconsistencies in ownership records began to appear. These documentation gaps later became central issues in legal challenges involving home loan securitization fraud.

The Breakdown of Mortgage Documentation and Chain of Title

One of the most critical elements of any mortgage loan is the chain of title. This refers to the documented history of ownership transfers associated with a mortgage note and its related security instrument. When the chain of title is intact, it clearly shows which entity currently owns the loan and has the legal right to enforce it.

However, widespread evidence has shown that in many securitized loans, the chain of title became severely compromised. Documents were sometimes missing, improperly dated, or created long after the loan had already been transferred. These irregularities became a defining characteristic of home loan securitization fraud.

The issue often surfaced during foreclosure proceedings. Homeowners and their attorneys began requesting proof that the foreclosing entity actually owned the loan. In numerous cases, lenders struggled to produce the original promissory note or valid assignments demonstrating ownership. This lack of documentation raised significant legal concerns and revealed systemic flaws in the securitization process.

Another controversial practice tied to home loan securitization fraud involved the use of mass document signing. Employees at servicing companies reportedly signed thousands of foreclosure documents without verifying their accuracy. These practices, commonly referred to as robo-signing, further undermined the reliability of mortgage records and intensified scrutiny from courts and regulators.

Financial Incentives That Encouraged Home Loan Securitization Fraud

The mortgage boom created enormous financial incentives for lenders and investment institutions to originate and securitize as many loans as possible. Mortgage originators earned fees when loans were created, while investment banks generated profits by packaging and selling mortgage-backed securities to investors. Because the loans were quickly sold into securitized pools, the institutions originating them often bore little long-term risk.

This structure created a dangerous misalignment of incentives. Instead of focusing on loan quality and borrower affordability, many lenders prioritized rapid loan origination. As a result, underwriting standards declined dramatically. Borrowers were sometimes approved for loans they could not realistically repay, and documentation requirements were frequently relaxed.

The aggressive push to generate new mortgages intensified the conditions that allowed home loan securitization fraud to spread throughout the mortgage industry. Loans were often transferred into securitized trusts without proper verification of documentation, and investors were sometimes given misleading information about the quality of the underlying assets.

These practices ultimately destabilized the mortgage market. When borrowers began defaulting on their loans, the weaknesses within securitized mortgage pools became impossible to ignore. Investors realized that some of the loans backing their securities lacked proper documentation or failed to meet the underwriting standards originally promised.

Legal Challenges and Courtroom Battles

Over the past decade, courts have played a significant role in exposing issues connected to home loan securitization fraud. Many homeowners facing foreclosure challenged lenders by demanding proof of ownership and compliance with securitization rules. These legal disputes revealed numerous inconsistencies in mortgage documentation.

In some cases, courts ruled that lenders could not proceed with foreclosure because they failed to demonstrate proper ownership of the loan. Judges questioned the validity of assignments that were executed years after the loan had supposedly been transferred into securitized trusts. These rulings forced financial institutions to review their foreclosure procedures and improve their documentation practices.

Legal scholars have also examined the role of trust agreements governing mortgage-backed securities. These agreements often require loans to be transferred into the trust within strict timelines and with specific documentation. When loans were transferred improperly or after these deadlines, it raised additional questions about whether the trust legally owned the mortgage. Such irregularities became another key indicator of potential home loan securitization fraud.

While many cases have been settled or dismissed for procedural reasons, the broader legal debates continue. Courts across different jurisdictions have issued varying interpretations of securitization rules, which has contributed to ongoing uncertainty in mortgage litigation.

The Impact on Borrowers and Investors

The consequences of home loan securitization fraud have affected multiple groups within the financial ecosystem. For homeowners, the issue often surfaces during foreclosure disputes, where borrowers question whether the entity attempting to seize their property actually holds the legal authority to do so.

Many homeowners have discovered that their mortgage loans were transferred multiple times without their knowledge. These transfers sometimes occurred through complex financial structures involving investment banks, servicing companies, and securitized trusts. When documentation problems arise, borrowers may face prolonged legal battles while attempting to protect their homes.

Investors have also suffered significant consequences. Pension funds, insurance companies, and other institutional investors purchased mortgage-backed securities believing they were backed by properly documented loans. When documentation flaws and loan quality issues emerged, many investors experienced substantial financial losses.

The exposure of home loan securitization fraud also damaged public trust in the mortgage industry. Many consumers began questioning whether the financial institutions managing their loans were operating with sufficient transparency and accountability. These concerns led to increased calls for stronger regulatory oversight and improved consumer protections.

Regulatory Scrutiny and the Path Toward Greater Transparency

In response to widespread concerns about home loan securitization fraud, regulators and policymakers have taken steps to strengthen oversight of mortgage practices. Financial institutions now face stricter documentation requirements, improved auditing procedures, and greater regulatory scrutiny regarding mortgage transfers and securitization activities.

Government agencies and financial regulators have introduced rules designed to increase transparency in mortgage-backed securities markets. These reforms aim to ensure that investors receive accurate information about the loans underlying securitized products. In addition, servicing standards have been updated to improve accountability among companies responsible for managing mortgage loans.

Despite these reforms, experts continue to debate whether current safeguards are sufficient to prevent future instances of home loan securitization fraud. The complexity of modern financial systems means that transparency and accountability remain ongoing challenges.

However, increased awareness of securitization practices has empowered borrowers, attorneys, and financial professionals to examine mortgage documentation more closely. As the mortgage industry evolves, continued vigilance will be essential to ensuring that securitization operates in a lawful and transparent manner.

Conclusion

The growing awareness surrounding home loan securitization fraud has fundamentally changed how borrowers, legal professionals, and financial experts view the mortgage industry. What was once considered a highly technical and obscure financial process has now become a critical topic of investigation and debate. As more cases and financial records have been examined, the complex layers behind mortgage securitization have revealed serious concerns about documentation practices, loan ownership, and the legal rights of institutions attempting to enforce mortgages.

Understanding home loan securitization fraud is essential for homeowners who want to protect their financial interests and ensure that any entity claiming authority over their loan can legally prove its ownership. When proper procedures are not followed during the securitization process, gaps in documentation and irregularities in loan transfers may arise, potentially affecting foreclosure actions and legal proceedings.

At the same time, the broader financial system has learned important lessons from the exposure of home loan securitization fraud. Investors, regulators, and policymakers have recognized the need for stronger transparency, stricter documentation standards, and improved accountability within mortgage markets. Increased scrutiny has already led to reforms aimed at strengthening oversight and protecting both borrowers and investors.

Elevate Your Case Strategy with Expert Mortgage Intelligence

Success in complex mortgage and securitization cases often depends on the strength of the evidence and the clarity of the financial analysis behind it. Legal professionals, consultants, and industry associates frequently face complicated loan structures, incomplete documentation, and intricate securitization trails. In these situations, having reliable forensic insight can provide the clarity needed to build stronger, more persuasive cases.

For more than four years, Mortgage Audits Online has supported professional associates by delivering comprehensive securitization and forensic mortgage audits designed to uncover critical details within loan files. Our mission is simple—help our partners develop well-supported case strategies through detailed research, structured analysis, and dependable reporting.

Working exclusively as a business-to-business provider, our services are tailored for attorneys, legal researchers, consultants, and industry professionals who require in-depth mortgage analysis. Our experienced audit specialists carefully review loan documentation, securitization pathways, and financial records to identify potential inconsistencies, documentation gaps, and key evidentiary elements that may strengthen your case preparation.

Every audit is conducted with precision and professionalism to ensure that our associates receive clear, well-organized insights they can rely on when preparing litigation strategies or reviewing complex mortgage transactions. Our commitment to accuracy, dependability, and analytical clarity helps professionals move forward with greater confidence and strategic advantage.

If your team is navigating complicated mortgage documentation or securitization questions, partnering with a trusted forensic audit provider can make a meaningful difference.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

Take the next step toward clearer analysis, stronger documentation, and better-informed case strategies by connecting with our professional audit team today.

“Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}