Home Loan Securitization Fraud Revealed: The Hidden System Behind Mortgage Lending

The global mortgage market has evolved dramatically over the past few decades, introducing complex financial mechanisms designed to expand credit availability and increase liquidity within the housing sector. Among these mechanisms, securitization has played a major role in transforming traditional mortgage lending. However, alongside legitimate financial innovation, serious concerns have emerged regarding transparency, documentation, and investor accountability. These concerns have led many analysts, attorneys, and homeowners to closely examine what is increasingly described as home loan securitization fraud. Understanding this issue requires looking beyond the surface of mortgage agreements and exploring the intricate financial structures operating behind the scenes of modern lending.

At its core, securitization is the process of pooling numerous home loans together and converting them into mortgage-backed securities that are sold to investors in financial markets. Banks and lenders use this system to move mortgages off their balance sheets, allowing them to issue more loans while transferring risk to investors. In theory, this process creates efficiency and expands access to credit. However, critics argue that the rapid growth of securitization created opportunities for misrepresentation, improper documentation, and systemic irregularities that have contributed to what many describe as home loan securitization fraud.

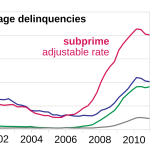

The issue gained widespread attention during the global financial crisis of 2007–2008, when millions of homeowners faced foreclosure and investigators began uncovering inconsistencies in loan ownership records and mortgage transfers. In numerous cases, mortgage notes appeared to be transferred multiple times without proper documentation, raising questions about who legally owned the debt and who had the authority to enforce foreclosure. These revelations fueled legal challenges across the United States and sparked debates about whether some lending practices constituted home loan securitization fraud rather than legitimate financial structuring.

One of the most controversial aspects of the system involves the separation of the mortgage note from the deed of trust during the securitization process. When loans are bundled and sold into investment trusts, the legal chain of ownership must be carefully documented through a series of assignments and endorsements. Critics argue that in many cases these steps were skipped, fabricated, or completed long after the fact. As a result, some homeowners and legal analysts claim that the lack of clear documentation has become a central indicator of home loan securitization fraud, particularly when lenders attempt to enforce foreclosure without demonstrating proper standing.

Another factor contributing to the debate is the role of mortgage servicing companies and electronic registry systems used to track loan transfers. While these systems were designed to streamline transactions, they have also been criticized for reducing transparency and weakening the traditional public recording process. When ownership records are incomplete or inconsistent, borrowers may find it difficult to determine who actually holds their mortgage, further intensifying concerns about home loan securitization fraud and its implications for both homeowners and investors.

Beyond the legal complexities, the broader impact of these issues extends into the financial system itself. Investors who purchased mortgage-backed securities rely on accurate loan documentation and proper underwriting standards. If the underlying loans were improperly transferred or documented, the integrity of the securities could be compromised. For this reason, regulators, attorneys, and financial analysts continue to investigate whether systemic weaknesses in mortgage documentation contributed to widespread home loan securitization fraud within the broader mortgage market.

As scrutiny of mortgage practices continues, awareness of home loan securitization fraud has become increasingly important for borrowers, legal professionals, and financial investigators alike. By examining loan origination records, securitization structures, and mortgage transfer documentation, experts seek to determine whether lenders followed proper procedures or whether irregularities occurred within the complex web of modern mortgage finance. Understanding these mechanisms is essential for anyone attempting to navigate the modern housing finance system and evaluate the legitimacy of mortgage claims in an increasingly securitized financial landscape.

The Evolution of Mortgage Lending and the Rise of Securitization

The modern mortgage industry did not develop overnight. It evolved over decades as financial institutions searched for ways to increase liquidity, distribute risk, and expand the availability of housing credit. Traditional lending models were once straightforward: a bank issued a home loan and kept the loan on its balance sheet until the borrower finished paying the mortgage. The bank collected monthly payments and assumed the full risk if the borrower defaulted.

However, as housing demand increased and financial markets expanded, lenders began looking for ways to free up capital so they could originate more loans. This search for efficiency led to the creation of mortgage securitization, a process that allowed lenders to bundle multiple loans together and sell them to investors as securities. While this system helped increase credit availability and stimulate the housing market, critics argue that it also laid the groundwork for what many now describe as home loan securitization fraud.

Through securitization, thousands of individual mortgages could be combined into investment pools known as mortgage-backed securities. Investors would purchase shares in these securities and receive income generated from homeowners’ monthly payments. In theory, the system created a mutually beneficial relationship between lenders, investors, and borrowers. Banks could issue more loans, investors could access new financial products, and borrowers could obtain mortgages more easily.

Yet as the securitization market grew rapidly, oversight and documentation practices did not always keep pace. Complex financial structures began replacing the simpler lender-borrower relationships that once defined the mortgage industry. In many cases, the original lender no longer owned the loan shortly after issuing it. Instead, the mortgage might pass through several intermediaries before being placed into a trust designed to hold thousands of mortgages for investors.

This complicated chain of ownership is one of the reasons investigators and legal professionals began examining potential home loan securitization fraud. When loans are transferred multiple times between institutions, strict documentation procedures must be followed to maintain a clear legal chain of ownership. If any step in that chain is incomplete or inaccurate, questions can arise about who truly holds the rights to the mortgage.

The increasing complexity of the mortgage market also meant that borrowers often had little knowledge of what happened to their loan after closing. Many homeowners assumed their lender continued to own the mortgage, when in reality the loan may have been sold to several entities within months. This disconnect between borrowers and the financial system surrounding their loans has fueled ongoing discussions about transparency and the potential presence of home loan securitization fraud within certain mortgage transactions.

Documentation Breakdowns and Legal Challenges in Mortgage Ownership

One of the most significant areas of concern surrounding home loan securitization fraud involves documentation. In a properly structured securitization, every mortgage must be transferred through a clearly recorded chain of assignments. Each transfer typically includes endorsements of the promissory note and recorded assignments of the mortgage or deed of trust.

During the housing boom that preceded the financial crisis, however, the mortgage industry processed loans at an unprecedented pace. Lenders, servicers, and financial institutions handled millions of mortgages each year, often relying on automated systems and third-party document processors. As a result, critics argue that documentation standards sometimes deteriorated under the pressure of high-volume loan production.

When the housing market collapsed and foreclosure cases began appearing in courts across the country, attorneys and investigators started examining loan files more closely. In some cases, they discovered missing assignments, improperly executed documents, or transfers that occurred years after the securitization trust was supposedly established. These irregularities prompted claims that certain foreclosures were initiated without clear evidence of ownership.

Such findings fueled allegations of home loan securitization fraud, particularly when lenders attempted to enforce mortgage rights without presenting a complete and verifiable chain of title. Courts in various jurisdictions began scrutinizing foreclosure documentation more carefully, leading to high-profile legal disputes and significant settlements within the banking industry.

Another issue frequently discussed in connection with home loan securitization fraud is the use of document-signing practices sometimes referred to as “robo-signing.” In these situations, employees or contractors signed large volumes of mortgage documents without verifying the underlying information. Critics argued that this practice undermined the reliability of legal filings and contributed to the documentation problems uncovered during foreclosure proceedings.

These legal challenges highlighted the importance of accurate mortgage records and reinforced the idea that transparency is essential in a financial system built on complex securitized assets. For borrowers facing foreclosure, documentation disputes often became the central issue in determining whether a lender had the legal authority to enforce a mortgage.

Financial Incentives and Structural Weaknesses in the Securitization System

Beyond documentation concerns, analysts examining home loan securitization fraud often focus on the financial incentives that shaped mortgage lending during the securitization boom. When lenders could quickly sell mortgages into securitized pools, their long-term exposure to loan performance decreased significantly. Instead of holding loans for decades, lenders could transfer the risk to investors shortly after origination.

This shift changed the traditional incentive structure of mortgage lending. In the past, lenders had strong motivation to ensure borrowers could repay their loans because the lender carried the financial risk. Under the securitization model, however, some institutions prioritized loan volume over long-term credit quality because the loans would soon be sold into investment trusts.

Critics argue that this environment contributed to questionable lending practices, including insufficient income verification, inflated property appraisals, and complex adjustable-rate mortgages that borrowers struggled to understand. While not every problematic loan represented home loan securitization fraud, the combination of weak oversight and aggressive lending practices created conditions where irregularities could occur.

Investment banks and financial institutions that structured mortgage-backed securities also faced pressure to produce large volumes of securities for investors seeking higher yields. As demand for these financial products grew, the pace of mortgage origination accelerated, sometimes outpacing regulatory supervision.

Within this environment, concerns about home loan securitization fraud expanded beyond individual loan files to broader questions about systemic risk and financial accountability. Analysts began examining whether certain securitization structures accurately represented the underlying mortgages to investors and whether loan documentation truly met the legal standards required for enforceable securities.

These questions became especially important when the financial crisis exposed the vulnerability of mortgage-backed securities tied to risky or poorly documented loans. As defaults increased, the value of many securities collapsed, leading to significant financial losses across the global banking system.

The Ongoing Importance of Transparency and Mortgage Audits

Today, the debate surrounding home loan securitization fraud continues to influence legal strategies, financial investigations, and regulatory discussions. Attorneys representing homeowners, investors, and financial institutions frequently examine mortgage files to verify whether securitization procedures were properly followed.

Mortgage audits have emerged as one of the primary tools used to analyze loan documentation and securitization structures. These audits involve reviewing the chain of assignments, examining trust agreements, and verifying whether mortgage transfers complied with applicable laws and contractual requirements.

For borrowers and legal professionals, identifying documentation inconsistencies can provide valuable insights into the history of a mortgage loan. While not every irregularity proves the existence of home loan securitization fraud, thorough analysis can reveal important details about how a loan was originated, transferred, and ultimately enforced.

Transparency remains the central principle guiding these investigations. Clear documentation, accurate records, and proper legal procedures are essential for maintaining confidence in the mortgage system. Without these safeguards, both homeowners and investors face uncertainty regarding the legitimacy of mortgage transactions.

As financial markets continue to evolve, the lessons learned from past controversies surrounding home loan securitization fraud highlight the need for stronger oversight, improved record-keeping, and greater accountability within the lending industry. By understanding the structural complexities of securitized mortgages, borrowers and professionals alike can better navigate the modern mortgage landscape and ensure that financial practices align with legal and ethical standards.

Conclusion

The growing awareness surrounding home loan securitization fraud has significantly reshaped how borrowers, legal professionals, and financial analysts view the modern mortgage system. What once appeared to be a straightforward lending process is now understood as part of a complex financial structure involving multiple institutions, investment trusts, and servicing entities. As securitization expanded, it introduced efficiency and liquidity into the housing market, but it also created layers of complexity that sometimes obscured transparency and accountability. These challenges are precisely why the issue of home loan securitization fraud continues to receive attention from courts, regulators, and financial investigators.

Examining mortgage documentation, loan transfers, and securitization structures has become essential in determining whether proper legal procedures were followed. When gaps in the chain of title, improper assignments, or questionable documentation practices are discovered, they raise legitimate concerns about the integrity of mortgage ownership and enforcement. These situations often become the focal point of investigations into potential home loan securitization fraud.

Ultimately, the discussion surrounding home loan securitization fraud highlights the importance of transparency, accurate recordkeeping, and accountability within the lending industry. A well-documented mortgage system protects both borrowers and investors by ensuring that financial rights and obligations are clearly established. As scrutiny of mortgage securitization continues, awareness and careful analysis remain crucial tools for identifying irregularities and maintaining trust in the housing finance system.

Gain Deeper Insight. Build Stronger Cases. Deliver Better Results

When complex mortgage documentation and securitization structures stand between you and a successful case outcome, having the right analytical support makes all the difference. That’s where our expertise comes in. For more than four years, we have been supporting professionals with detailed securitization reviews and forensic mortgage audits designed to uncover critical documentation issues and strengthen legal strategies.

Working exclusively as a business-to-business service provider, our focus is on empowering attorneys, investigators, consultants, and industry professionals with reliable, court-ready analysis. Our reports are carefully structured to highlight inconsistencies in loan transfers, chain-of-title issues, securitization pathways, and potential compliance violations—key insights that can elevate your case preparation and negotiation strategy.

Our team combines industry knowledge with analytical precision to deliver audit reports that are clear, structured, and actionable. Whether your goal is litigation support, pre-litigation case evaluation, or strategic negotiation leverage, our securitization and forensic audits provide the clarity needed to move forward with confidence.

Professionals across the mortgage and legal sectors rely on these audits to transform complex loan data into meaningful evidence. By identifying documentation gaps, assignment irregularities, and securitization inconsistencies, our work helps uncover the facts that matter most in high-stakes mortgage disputes.

If you are ready to strengthen your case analysis and offer greater value to your clients, connect with our team today. We are committed to delivering the precision, reliability, and insight that professionals depend on.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 877-399-2995

📠 Fax: 877-398-5288

🌐 Explore our services: Mortgage Audits Online official website

Partner with a team dedicated to helping professionals uncover the details that can shape stronger legal arguments and more successful outcomes

Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}