Home Loan Securitization Fraud: The Critical Facts Every Borrower Should Understand

The modern mortgage industry is built on complex financial systems that most borrowers rarely see or fully understand. When individuals apply for a mortgage, they typically believe they are entering into a straightforward agreement with a lender who will hold and manage the loan over time. However, in reality, many home loans are bundled together and sold to investors through a process known as securitization. While securitization itself is a legitimate financial practice used globally to increase liquidity in the lending market, serious concerns arise when the process is carried out improperly or without full transparency. This is where the issue of home loan securitization fraud becomes critically important for borrowers, homeowners, and legal professionals to understand.

At its core, home loan securitization fraud refers to situations where mortgage loans are improperly transferred, misrepresented, or documented during the securitization process. Instead of following strict legal and financial procedures, certain entities may manipulate documentation, conceal ownership of loans, or misrepresent the status of the mortgage within securitized investment structures. When these irregularities occur, the true ownership of a loan can become unclear, creating serious legal and financial consequences for borrowers who are simply trying to repay their mortgage or protect their property.

The securitization process typically involves several financial players, including loan originators, mortgage servicers, investment banks, trustees, and institutional investors. Loans are often bundled into mortgage-backed securities and sold in large financial markets. However, if any step in the transfer of loan ownership is handled incorrectly, it may create gaps in the chain of title or documentation. In some cases, missing assignments, improperly endorsed promissory notes, or questionable transfers into trust structures have raised allegations of home loan securitization fraud in courts and financial investigations.

For borrowers, the implications can be significant. Many homeowners have discovered that the entity attempting to enforce or foreclose on their mortgage may not clearly demonstrate legal ownership of the loan. This situation has led to disputes over standing, documentation authenticity, and compliance with securitization trust agreements. Because of these complexities, the issue of home loan securitization fraud has become a growing area of legal research, forensic auditing, and financial investigation.

Another concern is transparency. Borrowers are rarely informed when their loans are securitized, even though the ownership of their mortgage may change multiple times after the loan is originated. While these transfers are often legal, problems arise when documentation is incomplete, inaccurate, or intentionally altered. In such circumstances, the borrower may face enforcement actions from entities whose authority to collect or foreclose may be questionable. Understanding the potential risks associated with home loan securitization fraud can help borrowers recognize warning signs and seek professional assistance when necessary.

Over the past decade, increased scrutiny from regulators, courts, and consumer advocates has shed light on the complexities surrounding mortgage securitization. Investigations have revealed cases where loan documentation was processed in bulk, signatures were automated, or transfers into securitization trusts occurred outside the legally required timelines. These findings have fueled ongoing discussions about accountability, borrower protection, and financial transparency.

For homeowners, attorneys, and financial analysts, gaining a deeper understanding of home loan securitization fraud is essential. By learning how securitization works, how loans are transferred, and where documentation errors may occur, borrowers can better protect their rights and navigate the complicated financial structures that exist behind modern mortgage lending.

The Financial Architecture Behind Mortgage Securitization

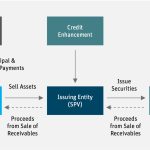

To understand home loan securitization fraud, it is first necessary to understand how the mortgage securitization system works. Mortgage securitization is a financial process in which banks and financial institutions bundle hundreds or thousands of individual home loans together and convert them into investment products known as mortgage-backed securities. These securities are then sold to institutional investors such as pension funds, insurance companies, and investment firms. The investors receive returns based on the payments made by borrowers on their mortgages.

The process typically begins with a loan originator, which could be a bank or mortgage company that provides the initial home loan to the borrower. Shortly after the loan is issued, the lender may sell it to another financial institution. That institution then transfers the loan into a securitization structure, usually a trust created specifically for the purpose of holding mortgage assets. The trust pools multiple loans together and issues securities that investors can purchase.

While this structure helps lenders free up capital and expand lending, it also creates layers of complexity. Multiple transfers occur between entities, including originators, aggregators, investment banks, trustees, and servicers. If these transfers are not documented properly, gaps in ownership records can arise. These documentation issues often form the foundation of claims involving home loan securitization fraud.

The Role of Documentation in Mortgage Ownership

Documentation is the backbone of any mortgage transaction. Two key documents typically define a mortgage loan: the promissory note and the mortgage or deed of trust. The promissory note represents the borrower’s promise to repay the loan, while the mortgage secures the loan against the property.

When loans are securitized, these documents must be transferred properly through each stage of the securitization chain. Each transfer requires endorsements, assignments, and proper recordkeeping to ensure the legal ownership of the loan remains clear. If the required transfers do not occur correctly or are completed after the required deadlines, legal disputes may arise.

Allegations of home loan securitization fraud often center on these documentation issues. Courts in several jurisdictions have examined cases where mortgage assignments appeared years after a foreclosure began, or where documentation was executed by parties who lacked legal authority. Such irregularities raise questions about whether the entity attempting to enforce the mortgage truly holds the legal rights to the loan.

Why Borrowers Rarely Know Their Loan Was Securitized

Most homeowners never realize that their mortgage may have been sold or securitized shortly after closing. Borrowers usually continue sending payments to the same mortgage servicer, even though the ownership of the loan may have changed multiple times behind the scenes.

Mortgage servicing companies act as intermediaries between borrowers and investors. They collect payments, manage escrow accounts, and handle customer service issues. However, servicers do not necessarily own the loans they manage. This separation between loan ownership and servicing is another factor that complicates disputes related to home loan securitization fraud.

Because borrowers rarely receive detailed information about securitization transfers, they may struggle to determine who actually owns their mortgage. When foreclosure proceedings occur, this lack of transparency can become a critical issue. Borrowers and their legal representatives may request documentation proving the chain of ownership, especially if concerns about home loan securitization fraud arise.

The Importance of the Chain of Title

The chain of title refers to the documented sequence of ownership transfers for a loan or property. In mortgage lending, maintaining a clear chain of title is essential to demonstrate who has the legal authority to enforce a loan agreement.

When securitization occurs, the loan should move through a defined path: from the original lender to an aggregator, then to a depositor, and finally into a securitization trust. Each step must be documented through legally valid assignments or endorsements.

If any step is missing, incomplete, or executed improperly, the chain of title may be broken. Broken chains of title are one of the most frequently discussed elements in investigations of home loan securitization fraud. Without proper documentation, it can become difficult to determine who legally owns the loan or has the right to initiate foreclosure.

These issues have appeared in numerous legal cases where courts required lenders to provide detailed evidence of loan ownership. In some situations, missing documentation has delayed foreclosure proceedings or forced lenders to reestablish the chain of ownership before continuing legal action.

Common Red Flags Associated With Mortgage Securitization Issues

Borrowers and legal professionals often examine several indicators when investigating potential home loan securitization fraud. One common red flag is the appearance of mortgage assignments created long after the loan was supposedly transferred into a securitization trust. Trust agreements typically require that loans be transferred within specific timelines, and transfers occurring years later may raise questions about compliance.

Another concern involves documentation signed by individuals who appear to execute large volumes of mortgage assignments on behalf of multiple institutions. In past investigations, some documents were allegedly signed without proper verification of the underlying transactions. Such practices have raised concerns about the accuracy and legitimacy of certain loan records.

Electronic mortgage registration systems have also drawn scrutiny in discussions surrounding home loan securitization fraud. While these systems were designed to streamline mortgage transfers, critics argue that they may obscure the true ownership of loans and complicate the verification of the chain of title.

Legal Challenges and Courtroom Disputes

The complexity of securitized mortgages has led to numerous legal disputes in courts around the world. Borrowers facing foreclosure sometimes challenge the authority of lenders by requesting proof that the entity initiating the foreclosure actually owns the loan.

In cases involving alleged home loan securitization fraud, courts may examine several factors, including the timing of mortgage assignments, the authenticity of signatures, and the compliance of transfers with trust agreements. Legal arguments often focus on whether the proper documentation exists to demonstrate the lender’s standing to enforce the loan.

Some court decisions have emphasized the importance of accurate documentation and transparency in mortgage transactions. These rulings highlight the need for financial institutions to maintain detailed records of loan transfers and ownership changes throughout the securitization process.

The Growing Role of Forensic Loan Audits

As awareness of home loan securitization fraud has increased, forensic loan audits have become a specialized area of financial investigation. These audits involve detailed examinations of mortgage documentation, securitization records, and loan transfer histories.

Forensic analysts may review loan origination documents, assignment records, trust agreements, and servicing data to determine whether the loan was transferred according to required procedures. In some cases, these investigations uncover inconsistencies in documentation or gaps in the chain of title.

Legal professionals sometimes rely on forensic loan audits to support litigation or settlement negotiations. While not every mortgage contains irregularities, these audits can provide valuable insights into the structure and history of securitized loans.

Why Understanding Securitization Matters for Borrowers

For many homeowners, the concept of securitization may seem distant from their everyday experience of paying a mortgage. However, understanding the basics of the securitization system can help borrowers make informed decisions when questions about loan ownership arise.

Knowledge of home loan securitization fraud allows borrowers to recognize the importance of documentation, transparency, and proper loan transfers. When disputes occur, having a clear understanding of how mortgages move through financial markets can help homeowners work effectively with attorneys, auditors, and financial experts.

As the mortgage industry continues to evolve, transparency and accountability remain essential priorities. By learning how securitization works and where irregularities may occur, borrowers can better navigate the complex financial structures that shape modern home lending.

Conclusion

Understanding the complexities behind modern mortgage lending is essential for every homeowner, especially in an era where financial structures have become increasingly layered and opaque. The issue of home loan securitization fraud highlights how critical transparency, proper documentation, and lawful loan transfers are within the mortgage industry. While securitization itself is a legitimate financial practice designed to improve liquidity and expand lending opportunities, problems arise when the process is not executed in accordance with established legal and financial standards.

For borrowers, awareness of home loan securitization fraud can play an important role in protecting their rights. Many homeowners are unaware that their mortgage may have been transferred multiple times after the loan was originated. When documentation errors, delayed assignments, or unclear ownership records appear, they may create legal complications that affect enforcement actions, loan servicing, or foreclosure proceedings.

Recognizing the warning signs of home loan securitization fraud can help borrowers, attorneys, and financial investigators identify potential irregularities within mortgage documentation and securitization structures. Careful examination of loan records, ownership transfers, and compliance with trust agreements can provide valuable insights into whether the mortgage has been handled properly.

Ultimately, increased awareness and due diligence remain the strongest safeguards against home loan securitization fraud, helping ensure accountability, transparency, and fairness within the mortgage system while empowering borrowers to better understand the financial structures behind their home loans.

Gain Deeper Insights. Build Stronger Mortgage Cases. Deliver Better Results

In today’s complex mortgage landscape, clarity and precision can make the difference between uncertainty and a well-supported case. When questions arise around loan transfers, securitization structures, or documentation irregularities, having the right analytical support becomes essential. That’s where Mortgage Audits Online steps in.

For more than four years, our team has supported professionals by providing detailed securitization analysis and forensic mortgage audits designed to uncover critical information within loan documentation. Our services are developed specifically for business-to-business partners, including attorneys, investigators, consultants, and financial professionals who require accurate insights to strengthen their case strategies.

Through careful examination of mortgage records, assignment histories, and securitization pathways, our audits help reveal key details that may otherwise remain hidden. Our goal is simple: deliver dependable analysis that allows our associates to present clearer arguments, make informed decisions, and pursue stronger outcomes for their clients.

At Mortgage Audits Online, we combine analytical precision with industry experience to provide reports that emphasize accuracy, dependability, and meaningful insight. Each audit is designed to support professionals who require reliable documentation reviews and comprehensive mortgage research.

If your organization is looking for trusted support in securitization and forensic mortgage auditing, we invite you to connect with our team.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: Mortgage Audits Online Official Website

Accuracy. Dependability. Insight. Strategic Advantage

Disclaimer Note: This article is for educational & entertainment purposes”

{kind=link}