Understanding Home Loan Selling & Securitization: How Banks Transfer Mortgage Risk

The modern banking system relies heavily on liquidity, risk management, and efficient capital utilization to sustain lending activities. One of the key mechanisms that enables banks to continue issuing new loans without exhausting their capital reserves is the process of home loan selling & securitization. This financial practice allows banks and lending institutions to transfer the ownership and risk of mortgage loans to other financial entities, investors, or securitization trusts. Instead of holding a home loan for its entire duration, banks bundle multiple mortgages together and sell them as mortgage-backed securities (MBS), creating opportunities to free up funds and reduce exposure to long-term credit risk.

Through home loan selling & securitization, lenders convert illiquid assets, such as long-term housing loans, into liquid financial instruments that can be traded in the capital markets. This not only strengthens the bank’s balance sheet but also enhances its capacity to provide fresh loans to new borrowers. For investors, securitized mortgage products offer an opportunity to earn returns based on the repayment streams of borrowers. However, this process also introduces complexities related to loan ownership, servicing rights, and borrower awareness. Understanding how this system works is essential for homeowners, financial professionals, and legal experts, as it directly influences loan servicing, foreclosure rights, and overall mortgage transparency.

The Core Concept Behind Home Loan Selling & Securitization

At its foundation, home loan selling & securitization is a structured financial process that allows banks and lenders to transfer mortgage loans from their own balance sheets to external investors. When a borrower takes a home loan, the bank initially owns the loan and receives monthly payments consisting of principal and interest. However, instead of holding that loan for 15 to 30 years, the bank often sells it to a larger financial entity such as a securitization trust, government-sponsored enterprise, or private investment institution.

This transfer does not usually affect the borrower’s repayment terms, interest rate, or loan tenure. The borrower continues to make payments as agreed, but the ownership of the loan—and therefore the right to receive those payments—has been transferred. The primary objective of home loan selling & securitization is to help banks recycle their capital efficiently so they can issue more loans to other customers. This continuous cycle supports the growth of the housing sector and ensures liquidity in the financial system.

How Banks Package and Transfer Mortgage Loans

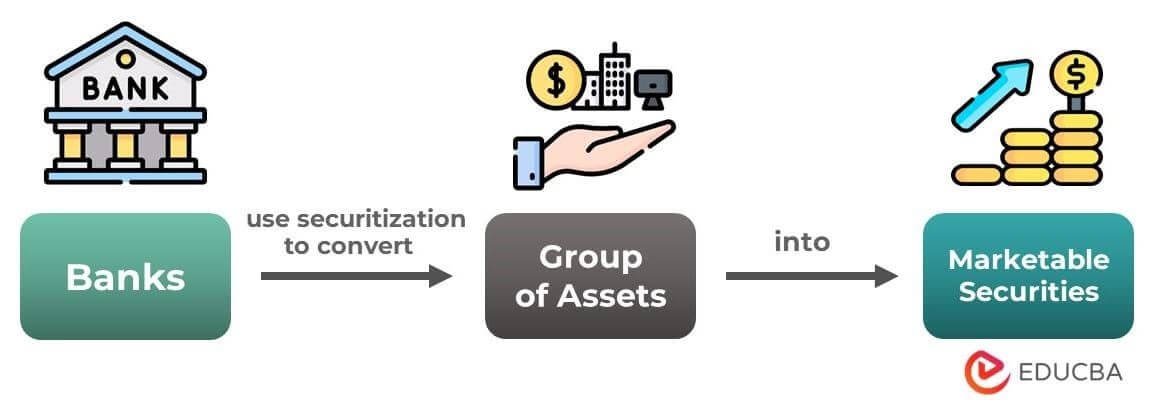

The process of home loan selling & securitization involves pooling multiple home loans with similar characteristics into a single financial package. These pooled loans are then transferred into a special legal entity called a Special Purpose Vehicle (SPV) or trust. The SPV becomes the legal owner of the loans and is responsible for issuing securities backed by these mortgages.

Investors purchase these securities because they generate income from the borrowers’ monthly payments. This creates a flow of funds from borrowers to investors through the SPV structure. Banks benefit immediately by receiving a lump sum payment from the sale, which improves their liquidity and reduces long-term exposure to borrower default risk. In this way, home loan selling & securitization transforms individual home loans into marketable financial instruments that can be bought and sold.

The Role of Loan Servicers After Securitization

Even after home loan selling & securitization, borrowers typically continue interacting with the same bank or servicing company. This is because the original lender often retains the servicing rights, meaning it continues to collect monthly payments, manage customer service, and handle administrative tasks. The servicer acts as an intermediary between the borrower and the actual loan owner.

This arrangement ensures continuity and convenience for borrowers, who may not even realize that their loan ownership has changed. However, legally, the financial rights belong to the investor or trust that purchased the loan. The servicing institution earns a servicing fee for managing the loan on behalf of the new owner.

Why Banks Rely on Home Loan Selling & Securitization

Banks depend on home loan selling & securitization to maintain financial stability and sustain lending operations. Holding too many long-term loans can limit a bank’s ability to provide new credit, as capital becomes tied up for extended periods. By selling loans, banks convert future payment streams into immediate funds, which can then be used to issue new mortgages, business loans, or personal loans.

This process also distributes risk across multiple investors rather than concentrating it within a single bank. As a result, the banking system becomes more resilient and capable of supporting economic growth. For borrowers, while the loan ownership may change behind the scenes, their repayment obligation remains the same, ensuring continuity in their homeownership journey.

Conclusion:

The Financial Impact and Borrower Implications of Home Loan Selling & Securitization

In conclusion, home loan selling & securitization plays a vital role in maintaining the strength, flexibility, and sustainability of the modern mortgage and banking system. By transferring mortgage ownership from lenders to investors through structured financial instruments, banks are able to free up capital, improve liquidity, and continue offering new loans to homebuyers. This process ensures that the housing finance ecosystem remains active and capable of supporting growing demand without placing excessive long-term risk on individual financial institutions.

For borrowers, home loan selling & securitization generally does not change the loan terms, interest rate, or repayment obligations. However, it does shift the legal ownership of the loan, which can affect who ultimately holds the financial rights associated with the mortgage. Despite this transfer, loan servicing typically remains consistent, allowing borrowers to continue making payments without disruption.

Understanding home loan selling & securitization empowers homeowners to become more informed about how their mortgage functions beyond the surface level. It also highlights the interconnected relationship between lenders, investors, and financial markets. Ultimately, this system supports broader economic growth while enabling banks to manage risk efficiently and maintain continuous lending capacity.

Unlock the Hidden Truth Behind Every Mortgage File

When it comes to mortgage securitization and loan ownership, clarity is not just valuable—it is essential. At Mortgage Audits Online, we empower legal professionals, forensic analysts, and industry associates with precise, reliable, and court-ready securitization and forensic audit reports. With over four years of dedicated experience serving business-to-business clients, our expertise helps uncover critical details that can strengthen case strategies, validate claims, and reveal securitization gaps that may otherwise go unnoticed.

Our professional audit solutions are designed to provide deep insight into mortgage transfers, chain of title, securitization status, and compliance issues. Whether you are preparing for litigation, supporting a client defense, or conducting due diligence, our detailed forensic reports give you the confidence and documentation needed to move forward with authority.

Partner with a trusted industry specialist committed to accuracy, confidentiality, and measurable results. Take the next step toward building stronger cases and delivering exceptional outcomes for your clients.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📞 Phone: 877-399-2995

📠 Fax: (877) 398-5288

{kind=link}