Home Loan Securitization Fraud: What Lies Beneath the Surface of Mortgage Securitization

The modern mortgage industry operates on complex financial mechanisms designed to increase liquidity and distribute risk, but these same systems can also conceal serious irregularities. One of the most concerning issues facing borrowers, attorneys, and financial investigators today is home loan securitizaztion fraud. This term refers to deceptive or unlawful practices that occur when mortgage loans are bundled, transferred, and sold to investors through securitization without proper documentation, authority, or transparency. While securitization itself is a legal and widely used financial process, problems arise when lenders, servicers, or financial institutions fail to follow required legal procedures during the transfer and assignment of mortgage loans.

In many cases, borrowers remain unaware that their loan has been sold multiple times, often without proper notification or valid legal assignments. This lack of transparency creates opportunities for errors, misrepresentations, and even fraudulent foreclosure actions. Home loan securitizaztion fraud may involve missing endorsements, fabricated assignments, broken chains of title, or improper loan transfers into trusts after critical deadlines. These issues can significantly impact the enforceability of the mortgage and the legal standing of the party attempting to collect payments or initiate foreclosure.

Understanding home loan securitizaztion fraud is essential for identifying potential violations, protecting borrower rights, and ensuring that financial institutions are held accountable for maintaining lawful and accurate mortgage records.

Understanding the Securitization Process and Where It Can Go Wrong

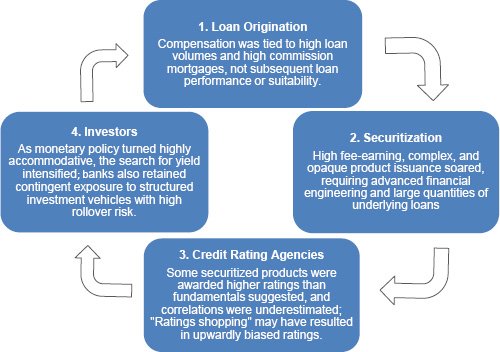

Mortgage securitization is a structured financial process where lenders bundle multiple home loans into mortgage-backed securities and sell them to investors. This process increases liquidity and allows lenders to issue more loans. However, the complexity of this system creates opportunities for documentation errors, misrepresentation, and unlawful transfers. Home loan securitizaztion fraud often arises when the original lender transfers the loan without properly endorsing the promissory note or recording the assignment in official land records. These failures create gaps in the chain of title, which may call into question who truly owns the loan and who has the legal authority to enforce it.

When mortgage loans are transferred into securitization trusts, strict timelines and legal requirements must be followed. If the loan is transferred after the trust’s closing date or without proper endorsements, the transfer may be invalid. In such cases, the entity attempting to collect payments or initiate foreclosure may lack legal standing. This is one of the most significant red flags associated with home loan securitizaztion fraud, as it directly affects the legitimacy of loan enforcement.

Chain of Title Breaks and Documentation Irregularities

One of the most critical aspects of mortgage legality is maintaining a clear and uninterrupted chain of title. This chain documents every transfer of ownership from the original lender to the current holder. In cases involving home loan securitizaztion fraud, this chain is often incomplete, inaccurate, or fabricated. Missing assignments, robo-signed documents, and backdated transfers are common indicators of serious documentation problems.

These irregularities can create legal uncertainty about who actually owns the mortgage. Without proper documentation, financial institutions may struggle to prove their right to enforce the loan. This is especially important in foreclosure proceedings, where the foreclosing party must demonstrate legal ownership of both the mortgage and the promissory note. When documentation is flawed or manipulated, it raises serious questions about the validity of the entire enforcement process.

The Role of Mortgage Servicers and Third Parties

Mortgage servicers play a central role in collecting payments and managing loans, but they are not always the true owners of the mortgage. In many securitized loans, servicers act on behalf of investors or trusts. However, home loan securitizaztion fraud can occur when servicers attempt to enforce loans without proper authority or when they rely on incomplete or inaccurate documentation.

Servicers may initiate foreclosure actions even when the loan was never properly transferred to the trust they represent. This creates legal disputes over standing and authority. In some cases, servicers produce assignments or endorsements only after foreclosure proceedings have begun, raising concerns about the authenticity and timing of those documents. These actions undermine the legal integrity of the mortgage system and can expose borrowers to wrongful foreclosure risks.

Legal and Financial Consequences for Borrowers and Institutions

The consequences of home loan securitizaztion fraud can be severe for both borrowers and financial institutions. Borrowers may face foreclosure actions from entities that cannot legally prove ownership of the loan. This can lead to prolonged legal battles, financial hardship, and emotional stress. At the same time, financial institutions may face regulatory penalties, lawsuits, and reputational damage if fraudulent or improper securitization practices are discovered.

Forensic loan audits and securitization analysis have become essential tools for uncovering these issues. By reviewing loan documents, assignment records, and securitization trust filings, investigators can identify irregularities and determine whether the loan was transferred properly. Detecting home loan securitizaztion fraud early can help borrowers and legal professionals challenge unlawful enforcement actions and protect their legal rights.

Conclusion: Exposing the Truth and Protecting Mortgage Integrity

The hidden complexities of mortgage securitization have created an environment where errors, misrepresentations, and unlawful practices can occur without immediate detection. Home loan securitizaztion fraud is not merely a technical issue—it represents a serious breakdown in transparency, accountability, and legal compliance within the mortgage industry. When loans are transferred without proper endorsements, recorded assignments, or adherence to trust requirements, the legal foundation of the mortgage itself can be compromised. This raises critical concerns about who truly owns the loan and whether enforcement actions, including foreclosure, are legally valid.

For borrowers, attorneys, and financial professionals, identifying home loan securitizaztion fraud is essential to ensuring fairness and protecting legal rights. Missing documents, broken chains of title, and questionable loan transfers are warning signs that demand careful investigation. These irregularities may provide grounds to challenge improper loan enforcement and hold responsible parties accountable.

Ultimately, awareness and thorough analysis are the strongest defenses against home loan securitizaztion fraud. By uncovering the truth behind loan transfers and securitization practices, stakeholders can safeguard financial integrity, promote lawful enforcement, and ensure that the mortgage system operates with the transparency and accountability it was designed to uphold.

Reveal the Evidence. Empower Your Strategy. Deliver Powerful Results for Your Clients

In today’s complex mortgage landscape, success depends on access to accurate information, detailed analysis, and reliable forensic insight. When questions arise around securitization, loan ownership, or documentation integrity, having the right partner can make all the difference. Mortgage Audits Online is committed to equipping legal professionals, auditors, and industry associates with comprehensive securitization and forensic audit reports that expose critical facts and strengthen case foundations.

For over four years, we have supported our business-to-business partners by delivering precise, court-ready findings designed to uncover hidden irregularities, identify documentation gaps, and clarify the true status of mortgage loans. Our expert-driven approach helps you build stronger arguments, enhance credibility, and confidently advocate for your clients. Whether you are preparing for litigation, conducting due diligence, or evaluating loan validity, our services provide the clarity and professional support you need to move forward with certainty.

Partner with a trusted provider dedicated exclusively to empowering professionals like you. Gain deeper insight, strengthen your legal strategy, and elevate your client outcomes with dependable forensic and securitization audits.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📞 Phone: 877-399-2995

📠 Fax: (877) 398-5288

🌐 Visit: https://www.mortgageauditsonline.com/

{kind=link}